Introduction

The dynamic digital work environment coupled with continual technological advancements have emphasised the need for accounting graduates to exhibit competence in digital skills. In particular, competence in Microsoft Excel (hereafter referred to as Excel) has been identified as an essential skill for accounting graduates by both employers and academics (Daff, 2021; Rackliffe & Ragland, 2016; Spraakman et al., 2015; Tysiac, 2019). Accounting educators worldwide have called for integration of technology and Excel use across accounting curricula to increase graduate employability (Al-Htaybat et al., 2018; Kotb et al., 2019; Lafond et al., 2016; Rackliffe & Ragland, 2016). However, this has been impeded by a lack of professional body accreditation for information technology- (IT) related content, crowded syllabi and issues relating to faculty competence in the use of Excel (Kotb et al., 2019).

Traditionally, the teaching of software packages such as Excel takes place as stand-alone modules on accounting programmes. This approach was questioned by Rackliffe and Ragland (2016, p. 161) who recommended “incorporating Excel in a comprehensive, integrative, and pedagogically consistent manner in the accounting curriculum to improve students’ proficiency in Excel technology” while preparing students for their future careers. Reflecting this, Sangster et al. (2020, p. 447) have called for studies to provide “evidence-based good practice guides and practice exemplars” for technology use within accounting education. Prior research in this area is limited. Dania et al. (2019) demonstrated that accounting and finance students expressed a preference for the use of Excel within the classroom as a teaching aid for presentation of learning material during lectures. Additionally, Willis (2016) investigated the teaching of Excel to accounting undergraduates within an IT module, suggesting a project-type exercise for improving students’ Excel skills. Despite some evidence in this area, there is an absence of research on how Excel is delivered simultaneously with accounting in an integrative manner as recommended by Rackliffe and Ragland (2016).

This study addresses this gap by integrating the teaching of Excel within undergraduate financial accounting modules and investigating the experiences of students taught financial accounting using the technology-integrated approach. Harel and Papert (1990, p. 29) proposed the ‘integrated learning’ principle which states that “learning more can be easier than learning less”. They observed that students learning mathematics and software design in an integrated way learned more than had the learning content been taught separately. The objective of this study therefore is to investigate if, and how, integrated learning may be designed within a financial accounting class to develop the accounting-related IT skills that students require when entering the workplace, while also enhancing their financial accounting learning experience.

Educational research has been heavily criticised for its lack of practical impact in classrooms, as the scientific knowledge it generates is often an insufficient representation of the phenomena it alleges to address (Brown, 1992; Sandoval & Bell, 2004). This is due to a focus on isolating single variables to establish causal effects using experiments that are conducted in controlled laboratories, removed from real educational settings (Gravemeijer & Cobb, 2013; McKenney, 2017; Plomp, 2013). However, experimental control is difficult to achieve in classrooms where there are multiple dependent variables at play in producing learning outcomes, such as learners’ prior experiences and skill levels (Entwistle et al., 2010). In contrast, this study applies a design-based research (DBR) methodology that is newly emerging within the accounting education field. DBR addresses the complexity of educational environments by designing elements of a ‘learning ecology’ and studying how they work together to aid learning (Cobb et al., 2003). DBR seeks analytical generalisation in the form of obtaining a greater understanding of learning ecologies with a view to supporting others in using design products to obtain learning benefits in other settings, rather than focusing on isolated variables to achieve a statistical generalisation (Gravemeijer & Cobb, 2013; Herrington et al., 2007; Plomp, 2013).

DBR supports a broad inclusive perspective of learning, with participants co-creating a blended learning pedagogical approach through iterative cycles of design, implementation and evaluation. This paper depicts how one element of the blended learning intervention, the integrated learning of MS Excel within financial accounting modules, was designed, implemented and refined with first-year accounting undergraduate students over three design iterations spanning academic years from 2017 to 2020. Educational research has also been criticised for its narrow focus on “learning of content and skills as the only measure of worth” when evaluating interventions (Collins et al., 2004, p. 18). This study goes beyond narrow measures of learning by focusing on learners’ perceptions of their integrated learning experience rather than aiming to test students’ skill levels.

This study extends prior research by providing an exemplar of effective learning design and implementation where Excel is taught in an integrated way in accounting modules. It thus makes a meaningful contribution to learning theory in the area of accounting education. In addition, the research demonstrates that students’ perceived Excel skill levels can be enhanced through the integrated learning of Excel and financial accounting. The study’s findings and narrative account of the integrated learning design provide guidance to accounting educators who wish to design learning environments to equip students with digital skillsets in preparation for the workplace.

The remainder of the paper is organised as follows. Firstly, the literature review considers the pedagogical considerations for teaching with technology, based on constructivist learning principles. Secondly, details of the study context and participants are presented. Thirdly, a section on the research methodology outlines the DBR methodology used. The fourth section reports on the implementation and findings pertaining to the integrated learning approach. The process used to integrate the learning and teaching of financial accounting and Excel across the three design cycles is elaborated upon, presenting the findings from each cycle and their impact on subsequent cycles. Finally, a discussion and conclusions section considers the findings and their implications for accounting educators.

Literature Review

A review of the literature identifies important pedagogical considerations when integrating technology with learning and teaching. In particular, constructivist learning environments are relevant, emphasising the need to address active learning, authentic tasks and scaffold learners.

Constructivist theory posits that learners participate actively in the learning process rather than receiving knowledge passively, building their own knowledge and forming their own understanding in relation to the world around them (Fosnot, 2005). Constructivist learning environments are designed to include elements of ‘real-world’ settings, where learners are allowed to actively construct their own meaning as they work collaboratively using conversation involving planning, negotiating and problem-solving (Jonassen et al., 1995; Kirschner, 2001). Herrington and Oliver (2000) suggested that students’ self-learning and self-regulation skills can be fostered within authentic learning environments using activities that have real-world relevance rather than decontextualised classroom tasks. Use of authentic tasks gives students an opportunity to build knowledge, while linking with past experiences and identifying the real-life relevance of that knowledge (Woo & Reeves, 2007), resulting in knowledge gained being more effectively applied when solving future real-life problems (Herrington & Oliver, 2000). In addition, projects that have an authentic focus lead to higher levels of satisfaction for students when compared with working on artificial problems (Kearsley & Shneiderman, 1998).

Soloway et al. (1994, 1996) proposed use of active constructive learning where the learning environment also contains elements of socioculturalism. Learning, according to socioculturalism, is enculturation that involves learners engaged in collaborative meaning-making using the practices and tools of the professional discipline being studied. Enculturation is achieved through use of authentic activities from the work domain with learning supported through use of ‘scaffolding’.

“… when learning is divorced from doing a meaningful task – as are many arbitrary, decontextualized activities in the classroom – then learning becomes just another chore, low on the priority stack” (Soloway et al., 1994, p. 40)

‘Scaffolding’ refers to the support provided to students by teachers or others to assist students in the mastery of tasks. The term ‘scaffolding’ was applied originally by Luria (Luria & Vygotsky, 1930) and Bernstein (1947) in relation to the use of motor skills in developing movement. It was later transferred by Wood et al. (1976) to the teaching and learning process. Scaffolding may be achieved by initially ‘controlling’ the task elements that are beyond the learner’s competency, allowing them to concentrate on the elements that are within their ability level, eventually facilitating successful completion of the task. The scaffolding is gradually faded until the learner can perform the task completely independently of others. The teacher plays a key role in scaffolding, as the nature of the task and learner characteristics must be considered when planning the learning activities. Under constructivism, scaffolding can take place through: relating new information to previously acquired information; use of relevant and meaningful tasks; encouraging reflection and metacognitive awareness; and expressing the task as a series of steps to reduce its complexity, thereby reducing cognitive overload (Soloway et al., 1996). Cognitive overload occurs when working memory becomes overwhelmed dealing with large amounts of complex information (Sweller, 1988).

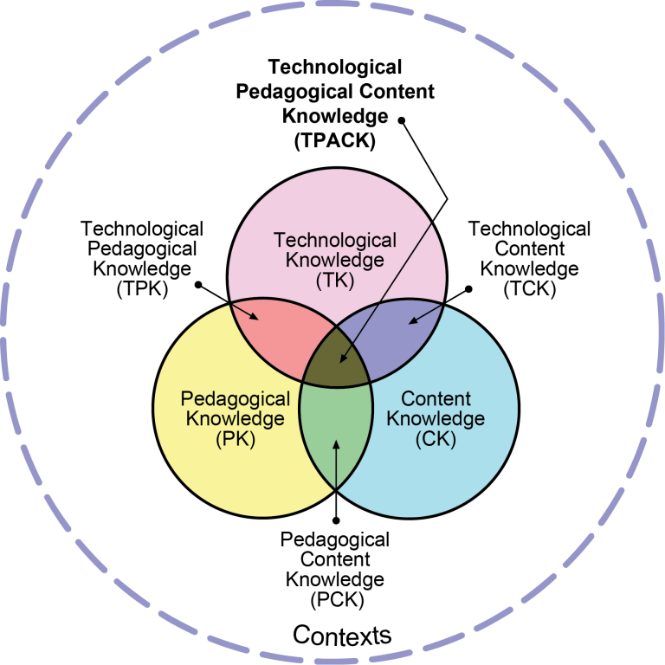

Mishra and Koehler (2006, p. 1045) advocated for “learning environments that allow students and teachers to explore technologies in relationship to subject matter in authentic contexts”. They developed the TPACK framework, utilising a design experiments research methodology, for use by teachers when designing learning environments that integrate technology and pedagogy. The framework builds on the seminal work of Shulman (1986, 1987) on pedagogical content knowledge (PCK), which refers to the way in which subject matter is changed by teachers into a form that is easily understandable by learners. The TPACK model, as illustrated in Figure 1, recognises that knowledge of a technology does not necessarily produce good teaching with the technology, as “merely knowing how to use technology is not the same as knowing how to teach with it” (Mishra & Koehler, 2006, p. 2033). Teachers must consider how to combine technology with subject matter and pedagogy to create an effective learning environment. Technology use can place constraints on content delivery and affect pedagogical decisions. For example, software is typically designed for business rather than education; it may not always be suitable for use in an educational context. This view is echoed by Sangster et al. (2020) who recognised the need to focus on pedagogcial matters when teaching with technology in an accounting education context.

Elements of the TPACK model as shown in Figure 1 are outlined in Table 1.

When integrating technology into the classroom, there is no single approach that works for every teacher or programme, rather technology integration should take place through the teacher’s creative ability to positively exploit the complex interactions between content, pedagogy and technology (Figure 1), and are specific to the learning and teaching context (Koehler & Mishra, 2009). However, the knowledge components (content, pedagogy and technology) cannot be viewed in isolation, as there is a dynamic relationship between them. Introduction of a new technology affects the equilibrium between the three elements of the TPACK model and forces the teacher to re-calibrate by looking at content, pedagogy and change the teaching and learning approach (Koehler & Mishra, 2009; Mishra & Koehler, 2006).

The next section introduces the research context and provides a profile of the study participants.

Study Context and Participants

This study was carried out in an Irish higher education institution. Participants in the research were enrolled in year 1 of Bachelor of Arts in Accounting and Bachelor of Arts in Accounting and Law programmes. Participants were engaging in introductory financial accounting modules across two semesters with the researcher (and first author) as instructor. The study took place over three design cycles, with a total of 68 student participants. (Note: a different set of first-year students participated in each design cycle.) The profile of participants is given in Table 2.

The majority of study participants were school leavers, aged under 23 years. Over the course of the three design cycles there was a relatively even proportion of males and females. International students comprised 22% of the total participants across the three cycles. Prior to engaging with the intervention, study participants had not encountered Excel as part of their undergraduate programme. However, some students had previous experience of Excel, further detail of which is provided in the implementation and findings section of this paper.

Research Methodology

Design research can be considered as a common label assigned to “a family of related research” (Van den Akker et al., 2006, p. 4), examples of which include design experiments (Brown, 1992; Collins, 1992), design-based research (The Design-Based Research Collective, 2003) and design studies (Shavelson et al., 2003). The DBR methodology applied in this study was chosen due to its ability to address the complexity of educational practice (Sandoval, 2014). With DBR, the classroom becomes a “living laboratory” where educational interventions are implemented and researched in a local context (Brown, 1992). The DBR methodology was considered most suited for the current study as it facilitated the design of the learning intervention while also providing a theoretical understanding (McKenney & Reeves, 2013) applicable in this context to the accounting education field.

“Design-based research is premised on the notion that we can learn important things about the nature and conditions of learning by attempting to engineer and sustain educational innovation in everyday settings.” (Bell, 2004, p. 243)

Throughout the study, the researcher progressively tested and refined a pedagogical approach involving the simultaneous teaching of financial accounting and Excel through a series of successive implementations. Using the DBR methodology, iterative cycles of the integrated learning approach were enacted, with design changes implemented in collaboration with key stakeholders (Hogan et al., 2017). After each implementation cycle, evaluation took place and changes were made to further improve the intervention and its ability to enhance the learning experience of students (Kelly, 2020; Kelly et al., 2022).

While DBR is an established and effective methodology for contemporary and novel learning environments (The Design-Based Research Collective, 2003), it has been acknowledged that difficulties can arise due to the multivariate nature of real-world situations, along with the large amounts of data typically generated during a DBR study (Collins et al., 2004). To address this, a mixed-methods approach was employed, involving the collection of quantitative and qualitative data from various sources, including surveys, student learning logs, group interviews and instructor field notes. Pre- and post-implementation surveys were administered at the commencement and end of each design cycle respectively. Quantitative survey data were analysed using SPSS, while qualitative survey data were integrated with qualitative data from student learning logs and group interviews. Additionally, students were encouraged to externalise their thoughts, feelings, opinions, and perceptions using learning logs available on the financial accounting Moodle page. The logs, available throughout each design cycle, were set up in open-ended journal format on Moodle as learning diaries in which students could write from a personal and reflective perspective. Completion of learning logs also allowed students to reflect on their learning, offering an opportunity for greater metacognitive awareness among students and contributing to the scaffolding of learners, as posited by Soloway et al. (1996).

At the conclusion of each cycle, a one-hour group interview was conducted by the researcher with a small number of participants to probe complex issues and gain a thorough understanding of participants’ views on their experiences of the learning intervention. Interviews followed a semi-structured format using an interview guide with an evolving set of questions that offered flexibility to allow interviewees to elaborate on points of interest. Each interview was audio-recorded with the prior consent of interviewees. Transcription was conducted by the researcher, offering the benefit of bringing her closer to the data. Finally, the researcher collected primary data on the design implementation throughout the study by recording descriptive and reflective notes on interactions in the learning environment.

Qualitative data was input to Excel and coded using concept mapping, posited by Metcalfe (2007, p. 149) as a “rational method for emerging appropriate concepts from discussions with stakeholders”. This involved coding student statements with statements that were similar or identical in meaning. The coding data were then entered into an interaction matrix (Metcalfe, 2007) and imported into UCINET6 social network analysis software (Borgatti et al., 2002), which produced clusters of data items, each representing a pragmatic concept. Concept mapping allowed the research to produce a graphical output showing the connections between idea clusters, which helped to identify relationships between the underlying concepts/themes (Trochim, 1989). The researcher used the ‘following a thread’ model advanced by Moran-Ellis et al. (2006) to integrate the multiple datasets.

Ethical approval was obtained from the relevant institutional research ethics committees in advance of the study. The researcher was also guided by the Ethical Guidelines for Educational Research (British Educational Research Association, 2018). Informed consent was obtained from all participants. Communication with students indicated that participation was voluntary and that they may withdraw from the research at any time without explanation or fear of adverse consequences. Due to the researcher’s dual role of lecturer and researcher within the study, she was aware of the need to be reflexive to ensure the research was conducted ethically. To establish credibility, regular conversations took place with a ‘critical friend’ employed within the same institution but outside of the faculty where the study was located, to probe issues relating to methodology, researcher bias and emerging conclusions (Foulger, 2010).

Integrated Learning: Implementation and Findings

This section describes the process used to integrate the learning and teaching of financial accounting and Excel across the three design iterations, with the objective of developing students’ accounting-related IT skills while also enhancing their learning experience within financial accounting. The findings from each iteration are presented and how they informed design changes for each subsequent design cycle are discussed. Finally, a summary of the study findings pertaining to the research objective is presented.

Design Cycle 1

In this study, the integrated learning principle was applied by integrating the teaching of the Excel spreadsheet application with financial accounting (Harel & Papert, 1990). As Excel is a digital workplace tool used commonly by accountants in practice and industry, its use within the classroom constitutes incorporation of an authentic activity from the work domain within the learning environment, in line with constructivist learning theory (Soloway et al., 1994, 1996). This was facilitated by timetabling some of the face-to-face class hours in introductory financial accounting modules in a computer laboratory rather than a traditional classroom.

During these classes, the lecturer used her PCK (see Figure 1) to identify suitable pedagogical practices for teaching the specific accounting subject matter. Topic material was first illustrated using the PC and projector located at the top of the room. Examples were illustrated in a step-like fashion to reduce complexity and the cognitive load. New material was introduced on a gradual basis through worked examples of increasing complexity so that learners could relate it to previously acquired information. In this way students were ‘scaffolded’ through the learning process (Soloway et al., 1996). As students became more familiar with learning material, they were encouraged to work on solutions to problems in their question manual using Excel, while the lecturer was available to provide assistance where necessary. In this way, the scaffolding was faded to allow the learners to independently complete problem solutions.

During Cycle 1, the researcher observed a slower pace of learning in the computer laboratory due to varying levels of skills in using Excel. This was confirmed by one student during the group interview: “I feel less is done in the computer class” (2017–18, Student 26, group interview). The researcher also recorded in her field notes that certain question types, particularly those that relied heavily on preparation of ledger accounts, proved difficult for students to work on in Excel. Bearing in mind that “not every topic can be shoehorned into any technology and, correspondingly, any given technology is not necessarily appropriate for every topic” (Mishra & Koehler, 2006, p. 1040), the lecturer needed to use her TCK (Figure 1) when considering carefully the suitability of each accounting topic for delivery using Excel.

Unlike a traditional lecture where all students sit facing the top of the room, the computer laboratory seating arrangement resulted in some students facing towards the sides and back of the room. This caused difficulties when the lecturer needed to address the whole class. Furthermore, the space between computers caused a ‘separateness’ among students, which inhibited group exercises, with the researcher also observing an absence of double-checking of answers among peers in the computer laboratory setting. As one student noted, the end-of-semester exam consisted of a written paper rather than an exam conducted through Excel:

“It’s different when you’re typing and then you go into the exam and you’re writing.” (2017–18, Student 15, group interview)

This reinforced the reflections of the researcher and emphasised the need to focus on pedagogical matters (Sangster et al., 2020), as it was essential that improvements in technological skills were not acquired at the expense of impeding learning in accounting.

Mishra and Koehler (2006) have noted that technology use within the classroom can place constraints on content delivery and affect pedagogical decisions. Within this study, scheduling face-to-face classes within a computer laboratory setting with the concomitant use of Excel as a learning tool required the researcher to employ TPACK in reviewing her teaching content and adapting her pedagogical approach to suit the technology use. As Excel was not designed for educational use, it was incumbent on the lecturer as researcher to employ her TPK (Figure 1) to re-purpose the software to serve a pedagogical purpose. Using Excel when learning about financial accounting could potentially lead to cognitive overload for students if pedagogical adaptations are not made. This was evident from this student’s comment:

“Trying to keep up with the typing and look at what you are doing at the same time wouldn’t be my strong point … You’re trying to balance the book, you’re trying to type, you’re trying to look. It’s too much!” (2017–18, Student 2, group interview)

Using her TPK, the researcher adapted her pedagogical approach to scaffold students in the use of the technology by preparing Excel templates for use during class to accommodate diverse levels of student Excel competency. Students typed their answers into the Excel template. Each Excel template comprised a proforma solution that was pre-populated with headings, text and borders. This allowed students to input their answers speedily without being constrained by slow typing speeds.

Despite their cognisance of the limitations imposed by classes in the computer laboratory setting, students in the group interviews accepted the benefits offered and the opportunity to improve their Excel skill levels. One student suggested reverting to a traditional classroom setting for course material that was less suitable for delivery in the computer laboratory:

“I think it should be brought in for the blended learning but I don’t think every week. I think we’re losing a bit if we’re having it every week.” (2017–18, Student 26, group interview)

Design Cycle 2

In Cycle 2, the researcher utilised her TPACK to choose pedagogical practices that used the technology to support student learning of the subject matter (Mishra & Koehler, 2006). She adapted her pedagogical approach by using LanSchool classroom management software for demonstrating questions and solutions during class and provided templates using Excel to accelerate data entry where appropriate. Excel templates facilitated students in completing the solution using technology without having to struggle too much if they were less experienced in using the software, thus acting as a supporting scaffold for them. Students input their own formulae, where required, while completing the solution. Moreover, when providing solution templates in Excel during this cycle, the lecturer also provided a copy of the question in Excel format. This allowed parts of the question to be illustrated to students using LanSchool and enabled them to click back and forth between the question and solution as they worked. In addition, LanSchool allowed the lecturer to take control of the students’ screens when demonstrating topic material, which helped to overcome the constraints of the computer laboratory seating layout. These design changes aimed to achieve an enhanced learning experience during classes scheduled in the computer laboratory.

The introduction of LanSchool for demonstrating solutions to problems in computer laboratory classes was noted by the researcher as a successful change, as reflected in this student’s comment:

“I particularly like when the screen is taken over as I can look at what you are showing us and taking in what is being said at the same time.” (2018–19, Student 19, survey response)

Scaffolding provided by the Excel templates during computer laboratory classes (Soloway et al., 1996) was also commended by the students; for example:

“I had never used Excel before, but it is not difficult as the template is already there. Once you get used to Excel it is very easy and practical to use.” (2018–19, Student 17, semester 1, student log)

However, a number of group interview participants indicated a preference for writing out the full solution layout when working on problems, rather than working from an Excel template:

“You’d prefer to be writing out the layouts of them because you’re going to need to for your exam.” (2018–19, Student 18, group interview)

Contrasting views were presented by others who valued the authenticity offered by using a digital tool employed in the workplace:

“I think it’s helpful doing it on Excel though, because if you think about it like when you go on to be an accountant everything is done on computers really. You’re not going to be writing it out.” (2018–19, Student 12, group interview)

“I liked the fact that after completing the question we brought it one step further and used the computer because it made it more relatable to the work we will be doing in the future.” (2018–19, Student 22, semester 1, student log)

Another student recommended further scaffolding through use of a tutorial class on Excel at the commencement of the programme:

“I also feel I have a greater knowledge of the Excel program from this activity, but I think having one tutorial on all aspects of Excel at the start of the year would be highly beneficial for many students.” (2018–19, Student 8, semester 1, student log)

The lecturer was conscious of the fact that the final exam would be in pen-and-paper format, so was eager to ensure that students were also capable of completing problem solutions without the use of an Excel template. This point was also stressed by Cycle 1 participants; hence the lecturer used her TCK (Figure 1) to identify learning content that was unsuited to computer laboratory delivery, returning to the traditional classroom setting for delivery of such content and as the end-of-semester exam approached.

Another change during Design Cycle 2, motivated by constructivist learning theories, required students to complete a financial accounting assignment, which involved them completing a bank reconciliation question in groups of four. The task involved a real-life bank reconciliation exercise rather than the type of decontextualised bank reconciliation question that typically appears in accounting textbooks. The bank reconciliation task included ‘authentic’ bank statements together with cashbook details for the previous month. These details would be available to an accounts department employee but are not typically made available to college students when attempting a bank reconciliation. In line with constructivist learning theory, this allowed students to work collaboratively on an authentic task with real-world relevance, adding authenticity to the learning environment (Herrington & Oliver, 2000; Kearsley & Shneiderman, 1998; Soloway et al., 1996; Woo & Reeves, 2007). Students were subsequently required to submit their answer individually in electronic form using Excel via Moodle outside of class time. Students were not provided with an Excel template for this task and were free to use whatever format or formulae they wished. Incorporation of Excel as part of the assignment was designed to match a real-world accounting task in order to engage and motivate learners (Kearsley & Shneiderman, 1998).

Students valued the use of authentic questions, particularly the bank reconciliation topic, which involved an authentic bank statement and a more comprehensive cashbook providing historical detail:

“I found questions that were based around real-life scenarios aided me in understanding what it is I’m actually doing. This will help in exam situations as I will understand what I’m meant to do, I won’t just be following a learned formula.” (2018–19, Student 8, semester 1, student log)

“Real-life question was easier as we could see the previous month and easily find which numbers are part of the opening reconciliation.” (2018–19, Student 24, semester 1, student log)

The researcher observed a large number of students in the group using Excel formulae when submitting the financial accounting assignment in Excel format during semester 1, despite the fact that use of Excel formulae was not a requirement of the task, which is evidence that students’ knowledge of Excel had been enhanced.

Design Cycle 3

The design elements and changes from Cycle 2 were retained in Cycle 3. In addition, the lecturer held a tutorial class in the use of Excel at the commencement of the programme to familiarise students with use of simple Excel formulae. The tutorial was introduced in response to student feedback from Design Cycle 2, where some students expressed a preference for using pen and paper rather than Excel. Use of Excel software while teaching accounting increases the authenticity of education but can pose challenges for some students who lack IT experience. The tutorial was designed to scaffold students so that they would not struggle later in the semester when trying to use Excel while also encountering new financial accounting material. This involved the tutor scaffolding learners by considering the nature of the task and the learners’ characteristics when designing the learning environment (Wood et al., 1976). Students were provided with a handout illustrating the various formulae and worked on exercises that focused on use of the formulae and formatting within Excel. Despite most of the students indicating that they had not used Excel formulae prior to this, they worked confidently on the tasks assigned during this class.

Similar to Design Cycle 2, early in semester 1 students were required to upload a financial accounting assignment solution to Moodle using Excel. In general, students reported no problems in the use of Excel, despite a number of students indicating in their semester 1 logs that they had low levels of expertise:

“Typing my answer in Excel was OK but I need more practice using Excel, so hopefully next time I’ll be a lot better using it.” (2019–20, Student 11, semester 1, student log)

Many of the students indicated in their student logs that they had used Excel previously. However, this would not necessarily have taken place in an accounting context:

“I felt that putting the answers in Excel was a good option as it made it clearer when writing the answers and it was also a back-up to the calculations as it can be easy to make a mistake. I have used Excel before through work but mainly for tables and not calculations.” (2019–20, Student 2, semester 1, student log)

Nonetheless, one student who considered themself skilled in using Excel, still expressed a preference for writing on paper:

“Typing in Excel was no problem at all as I have used it before. … This assessment was good as Excel is easier for spotting mistakes before we upload the assignment to Moodle. I preferred doing the bank reconciliation questions in class because I would find it slightly easier to do these exercises on paper rather than on the computer.” (2019–20, Student 13, semester 1, student log)

In line with Design Cycle 2 findings, survey responses showed that participants valued the opportunity to apply their accounting knowledge when using Excel, appreciative of the authentic real-world knowledge that they were gaining:

“Excel is probably used quite often among some accountants. It is important that we learn how to use these kinds of programs in college as it prepares us for when we start working.” (2019–20, Student 13, survey response)

Group interview participants expressed a view that “textbook questions” may not be representative of tasks that they might be required to perform in the workplace, as it is a “different situation”. They were aware of the importance of being able to apply knowledge learned in college when they arrive in the workplace:

“You don’t want to land in on your first day at work and they hand you a bank rec sheet and you’re like, what’s this?” (2019–20, Student 5, group interview)

They appreciated the opportunity to work on tasks that resembled “real-life examples”, stating that it made the subject more “realistic” for them:

“You can apply it to your own life, like when your own bank statement comes in you’re like ‘oh, this is like what we did in class!’” (2019–20, Student 14, group interview)

One student described how they felt like they were doing “actual work”, while another student drew connections between the authentic bank reconciliation statement questions and the use of Excel throughout the module, indicating that both acted as preparation for the world of work.

There was no evidence of difficulties in using Excel within the various datasets collected during Cycle 3. The Excel tutorial introduced in Cycle 3 at the commencement of the programme, informed by student feedback and designed based on the lecturer’s TPK, is likely to have provided scaffolding to students, enabling them to progress quickly onto independent tasks using Excel, leading to positive student perceptions in relation to use of Excel as a learning tool during accounting classes. The lecturer observed an air of confidence among students in Cycle 3 at an early stage of semester 1. Furthermore, as the year progressed, students worked competently, inputting their own formulae where required. All group interview participants affirmed an increased confidence in the use of Excel following the financial accounting modules:

“It just made you feel more comfortable using Excel. You’d be typing in 3,000 + 4,000 + 7,000 whereas you can just go click + click + click = and you have it done!” (2019–20, Student 7, group interview)

The use of Excel templates provided by the lecturer to assist them during class was also commended. Students also provided positive feedback in relation to their experience of LanSchool in the computer laboratory, some commenting on how it allowed them to see the lecturer’s workings clearly. One student affirmed:

“I think it is pretty effective, especially when the lecturer takes over our screens and gives us demonstrations on how to complete questions.” (2019–20, Student 15, survey response)

This provides evidence of how TPACK impacted positively on the design of the integrated learning intervention. However, during the group interview a few students with high levels of prior accounting experience expressed frustration about their screens being taken over to demonstrate material with which they were already familiar:

“You just could be doing something and then the screen would be taken and then you’d lose focus and you’d just start drifting out, zoning out … it annoys me that … let’s say some people might not understand but you understand it perfectly.” (2019–20, Student 7, group interview)

Students indicated that offering LanSchool as an option that students could avail of would be preferable. While this shows evidence of the challenge posed when teaching students with mixed prior levels of knowledge, it also reveals a desire among students to work independently at their own pace and become more self-directed in their learning. This underlines the importance of considering issues relating to the learning context, such as learner characteristics, when designing novel learning interventions as depicted in the TPACK model (Mishra & Koehler, 2006).

Summary of Findings

Students rated their perceived skills levels in using Excel within a pre-implementation survey at the commencement of each cycle of the blended learning experience. As part of the post-implementation survey, students were asked to rate their perceived skills levels again. The post-implementation survey took place at the end of each design cycle, prior to the group interview and end-of-semester examination. In general, while students expressed low confidence levels in relation to their Excel skills at the commencement of the programme, survey results showed higher perceived levels of improvement at the end of their integrated learning experience across all three design cycles. For example, in Design Cycle 1, 63% of students indicated they had a small or no degree of skill at the commencement of the programme. This percentage decreased to 25% by the end of the course, with 75% stating moderate to extremely high levels of perceived skill. Results for all three design cycles are displayed in Table 3. The results overall indicate that engagement in the integrated learning experience increased perceptions of Excel skill levels among students.

When surveyed on their perceived improvement in level of skill when using Excel, 71% of students in Cycle 1 stated that they had achieved moderate to very high levels of improvement. When a comparison is made of perceived improvement in Excel skill across the three design iterations, it is evident that the majority of respondents indicated moderate to very high levels of perceived skill improvement across all three cycles. In addition, levels of perceived improvement increased as the study progressed, as displayed in Table 3. In Design Cycle 3, 93% of respondents indicated moderate to very high levels of perceived skill improvement. Only one student in Design Cycle 3 indicated a small improvement in Excel skill, attributing this to having a high standard of Excel knowledge prior to commencing the course.

In the post-implementation survey at the end of each design cycle, students were asked two questions relating to their self-efficacy in using Excel. These questions were based on an instrument developed and validated by Torkzadeh and van Dyke (2001) and adapted for use in this study. Question responses were based on a Likert-type scale, from ‘Strongly Disagree’ to ‘Strongly Agree’ and scored from 1 to 5 accordingly. Mean response scores for each question item are displayed in Table 4. Mean scores relating to students’ confidence levels in using Excel improved in Cycle 2, with Cycle 3 findings remaining largely in line with those in Cycle 2, indicating that design changes implemented from Cycle 2 onwards are likely to have had positive effects on learner confidence.

These findings were corroborated by qualitative survey responses, which indicated that students benefited from classes in the computer lab. Respondents said that the integrated learning intervention augmented their IT skills, increased their familiarity with Moodle and introduced them to Excel, which will be of benefit in their future careers. Students were affirmative in relation to improvements in their Excel skill levels:

“I didn’t know how to use Excel before I came to college and now I feel really comfortable using it.” (2018–19, Student 8, group interview)

When surveyed on their experiences of learning financial accounting using the blended learning design, levels of agreement on question items showed a general improvement by the third iteration, as displayed in Table 5.

Significant improvements took place in Design Cycle 2 in particular when the main changes influencing the design were implemented. Thus, there was evidence that learning activities provided within the design facilitated greater understanding, yielded increased confidence, and nurtured a greater interest in the financial accounting subject, thus enhancing the student learning experience. It is likely that the levels of scaffolding provided within the computer laboratory setting acted to reduce cognitive overload, contributing to an enhanced learning experience. It is acknowledged that the survey questions pertained to the students’ overall experience of the blended learning design, not specifically to their experiences in relation to the integrated learning of financial accounting with Excel. Nonetheless, these findings demonstrate that the integrated learning of Excel and financial accounting, with its authentic learning and perceptions of Excel skill improvement, is likely to have positively affected students’ overall learning experience within the financial accounting modules, while also augmenting their accounting-related IT skills.

Discussion and Conclusions

This study contributes to theory-building in designing future-focused accounting education through the novel use of a participatory DBR methodology, whereby the integrated learning of Excel and financial accounting took place based on constructivist learning principles, with the aim of providing first-year students with key accounting-related IT skills while learning financial accounting. Flanagan and Stewart (1991), when investigating the use of computers to enhance the learning process in accounting education, ascertained that teaching and learning are inextricably connected, but not the same. In developing the DBR model for this study and ultimately the teaching approach, consideration was given to how students learn, and to the contribution that the integrated learning of Excel and financial accounting can make to enhancing learning of accounting concepts along with Excel skills. This learning approach was designed based on learning theories, inspired by the work of Bromson et al. (1994) who emphasised the contribution that scholarship in learning theory research can make to the effective teaching and learning of accounting. This research advances our understanding of how we can implement concepts of learning in accounting education through DBR, illustrating how financial accounting can be enhanced through the integration of technology, to equip students with digital workplace skills. The learning intervention was implemented and evaluated across three design cycles and student perceptions of learning Excel during financial accounting classes using the integrated approach were examined. Improvements were enacted across each subsequent cycle, informed by student feedback and educational theories. Other accounting educators and researchers might consider taking the innovative DBR concepts and methods deployed in the current research and adapting them to develop engaging and impactful pedagogical interventions in their respective educational and teaching contexts.

This study also illustrates the benefits that accrue from exposing students to authentic activities from the work domain using a constructivist learning style. Learning financial accounting while using Excel, a digital workplace tool, introduced a real-world element into the learning environment, to engage and motivate learners (Kearsley & Shneiderman, 1998). Use of a collaborative financial accounting assignment with an authentic focus, informed by Herrington and Oliver (2000), allowed learners the opportunity to engage in a task that was relevant and meaningful. Students were ‘scaffolded’ by undertaking tasks in a series of steps (Soloway et al., 1996). Scaffolding was gradually reduced until students could complete a problem solution independently. The design elements implemented were all informed by constructivist learning theories.

The results indicated that learners perceived their Excel skill levels improved, having been exposed to the integrated learning approach. Confidence levels in relation to Excel use among questionnaire respondents were generally high at the end of each design iteration, following a learning experience that integrated financial accounting and Excel in a computer laboratory setting. These outcomes suggest that, in support of Harel and Papert’s (1990) integrated learning principle, financial accounting classes held in a computer laboratory setting can support the acquisition of Excel skills as students learn financial accounting. In addition, it was shown that the inclusion of tasks with real-world relevance added to learner satisfaction, in line with the arguments of Kearsley and Shneiderman (1998).

However, the integrated learning and teaching of Excel and financial accounting requires careful pedagogical planning, and the instructor to adapt their teaching approach and deploy TPACK to facilitate learning in the computer laboratory setting (Mishra & Koehler, 2006). As the study progressed, the pedagogical approach evolved in response to the dynamic interconnections between content, pedagogy and technology in the learning environment. These pedagogical amendments appeared to contribute to increased satisfaction levels among students as the design cycles progressed and changes were implemented based on student feedback. In this study, increasing levels of perceived skill improvements corresponded with the introduction of LanSchool classroom management software and increased use of Excel templates from Design Cycle 2 onwards, informed by the TPACK model (Mishra & Koehler, 2006). Furthermore, the addition of an Excel tutorial at the commencement of the academic year in Design Cycle 3 further acted to scaffold students (Bernstein, 1947; Luria & Vygotsky, 1930; Wood et al., 1976).

This study is distinguished by the participatory nature of the design process, whereby learners were listened to, and feedback used to positively influence the design as the iterations progressed. The study illustrates the potential offered by the DBR methodology in the design of learning environments in accounting education. A minority of students expressed a preference for traditional pen-and-paper methods, cognisant of their final exam being in this format. However, results show that in general students valued the authenticity offered by using a digital workplace tool during financial accounting classes, appreciating the real-world knowledge they were gaining. Students could identify the real-life relevance of that knowledge within a constructivist learning environment (Woo & Reeves, 2007). Thus, integrated learning of financial accounting and Excel can add value by exposing students to software that will be used ubiquitously in their future careers, while also enhancing their learning experience of accounting (Herrington & Oliver, 2000).

In terms of limitations, while small group sizes during each design cycle were easily facilitated in a computer laboratory setting, this study may be difficult to replicate with larger group sizes. The researcher was cognisant that scheduling classes in a computer laboratory is governed by timetabling constraints within the local institutional context and may not be as achievable in all educational settings. Future research could address integrated learning of accounting and Excel, whereby students use their own technological devices in an accounting classroom rather than a computer laboratory setting. A similar study in a financial accounting module, where the final exam is in a computer-based format, would also add greater insights into the potential of the integrated learning approach. In addition, instructor confidence in the use of Excel is acknowledged as a factor contributing to successful implementation. However, the detailed design and implementation process in this study should give direction to practitioners when integrating the teaching of technology with accounting in their own learning context. Thus, this study makes a valuable contribution in providing guidance to accounting educators wishing to equip their students with the necessary skillset in preparation for entering the digital workplace.