1. Introduction

Although much research has been undertaken on management accounting and control within different contexts, timeframes and locations, most has focused on larger organisations (Scapens & Bromwich, 2010). Consequently, research examining the role of management accounting in small and medium-sized enterprises (SMEs) is lacking (Lavia López & Hiebl, 2015; Mitchell & Reid, 2000; Prencipe et al., 2014), despite the prevalence of such firms in the European Union (EU) (Quinn, 2011) and the United States of America (US) (Office of the United States Trade Representative, 2020). Management accounting practices, such as costing, budgeting and performance measurement, are primarily supported by, and linked to, a range of IT tools (Knauer et al., 2020; Pedroso & Gomes, 2020). These fall into several categories (Laudon & Laudon, 2020) and support the main tasks performed by management accountants, such as registering, analysing, and reporting data to different management levels to support different types of decisions (Richins et al., 2017). Nevertheless, few studies have examined the links between IT tools, management accounting practices and SME performance, despite the importance of these areas individually.

This paper has three purposes. First, it examines the perception of chief financial officers (CFOs) in SMEs of the impact of IT tools on three primary areas of management accounting practice: costing, budgeting, and performance management. These three areas are in line with areas of management accounting practice identified in the literature (Lavia López & Hiebl, 2015); therefore, they should be understood in a broad sense here. Secondly, the paper examines the perception of CFOs of the impact of management accounting practices on the performance of their SMEs. Few studies have focused on these broad areas collectively, and there is a lack of research on performance management systems within SMEs (Heinicke, 2018). The impact of management accounting practices on the performance of SMEs is under-researched. While some support for enhanced performance has been found (Duréndez et al., 2016; Hakola, 2010; King et al., 2010; Marriott & Marriott, 2000), no consensus has yet emerged (Lavia López & Hiebl, 2015). However, as all firms are continually seeking a competitive edge over their rivals, the use of management accounting and control information to enable improved overall performance (as perceived by senior financial management) would represent a significant advance for SMEs. In addition, as [small] firm size has repeatedly been cited as a reason for lower usage of certain management accounting practices (Marc et al., 2010; Neubauer et al., 2012) due to, for example, a lack of resources and/or competitive pressures, any positive findings reported here may encourage SMEs to reconsider their future use of such practices.

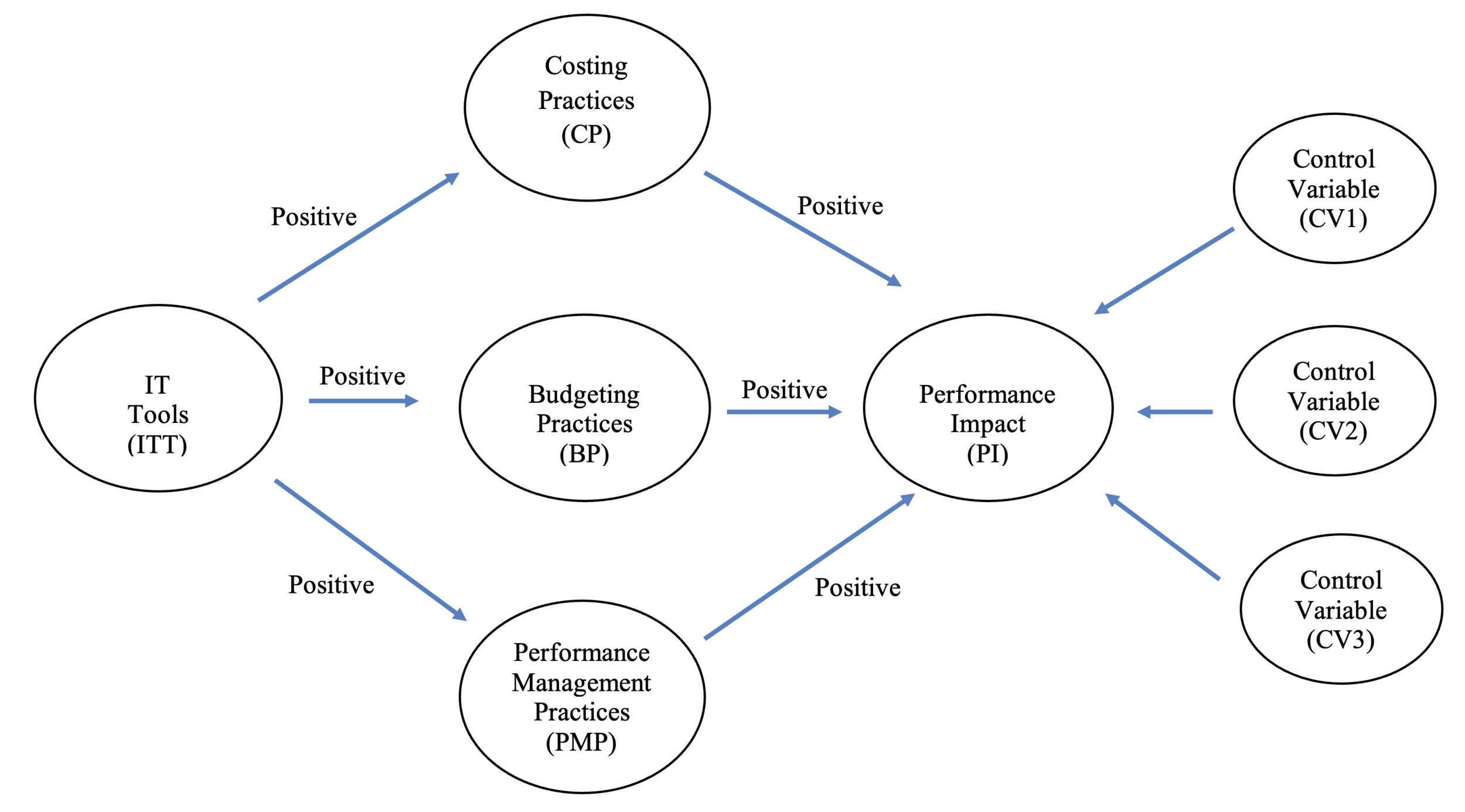

This study is based on empirical evidence collected from a survey distributed to 361 Irish SMEs, as defined by the European Commission (2005). Ireland is a country where SMEs are of critical importance to economic well-being (Central Statistics Office, 2021). Of this sample, 109 completed the survey, giving a response rate of 30%. A conceptual model was developed for this study. It first analyses the perception of CFOs within SMEs of the impact of information technology (IT) on the three primary areas of management accounting practice. Secondly, the model examines CFOs’ perception of the impact of management accounting practices on the performance of their SMEs. The proposed conceptual model was tested using partial least squares (PLS). In doing so, this paper responds to Nitzl’s (2016) call for the increased use of PLS in management accounting-based research. Therefore, this paper’s third purpose is to outline a methodological approach management accounting researchers can consider using in the future.

The following section provides a literature review of the main areas examined in this paper. The methodology is then presented, followed by an outline of the findings, before we provide concluding comments, including suggestions for possible future research.

2. Literature Review

The Impact of IT on the Management Accounting and Control Practices of SMEs

In recent decades, developments in IT have transformed how firms operate (Pavlou & El Sawy, 2010; Poon & Swatman, 1999). Firms now operate in an environment in which quickly and accurately provided data/information/knowledge is a prerequisite for competing. As the business environment changes faster than ever before (Otley, 2016), the requirement for rapid information increases significantly. Recent developments in cloud-based technologies have made accounting and other types of software widely accessible to small firms (Strauss et al., 2014). This has allowed them to benefit from lower IT costs, global data/systems availability, and automatic access to system/software updates (Cleary & Quinn, 2016; Du & Cong, 2010; Robinson, 2011). Although there are different classifications of business-related IT, a common typology is: (1) infrastructure systems, (2) knowledge management systems, (3) transaction registration and processing systems, (4) decision support systems, and (5) management information systems (Laudon & Laudon, 2020). The quality of the data produced by firms and its use largely determines how well they perform multiple tasks, including management accounting ones (Knauer et al., 2020). Consequently, neither management accounting practices nor the role of the management accountant is immune to these rapid technological advancements (Granlund & Malmi, 2002; Güney, 2014; Rikhardsson & Yigitbasioglu, 2018; Suddaby et al., 2015). This study focuses on management accounting practices.

Möller et al. (2020) note that many accounting practitioners believe that digitalisation has the potential to have a significant impact on management accounting practices, with areas such as performance measurement and capital investment techniques likely to require significant change. The website of a professional body such as the Chartered Institute of Management Accountants (CIMA) reveals a need for both technical and practical IT-based competencies as a prerequisite to membership. This importance attached to IT is not new: research conducted by the Institute of Management Accountants (IMA) in 1997 and 2000 reported that over 20% of practitioners identified IT as one of their most critical areas of focus, with over 50% of respondents expecting its importance to increase (Selto & Widener, 2004).

A structured review was undertaken to analyse the relevant literature. General search terms were used to capture any relevant and related literature using the Scopus database for the period between 2000 and 2018. The starting point represents when advances in IT tools, such as enterprise resource planning (ERP) systems and business intelligence, were beginning to be widely adopted. For example, SAP, one of the pioneers of the ERP market, released the first version of its software in 1992 (Bradford & Florin, 2003; Xu et al., 2019). Our search was applied to the paper title, abstract and keywords. We only considered journal articles from the “Business, Management and Accounting” category. An initial search used the broad terms “information technology” and/or “IT” and “management accounting” and returned 14 articles. A manual inspection revealed that most focus on specific systems such as ERP (Spraakman et al., 2018) in the context of larger companies and are therefore not directly comparable to our study of SMEs.

Similar searches and manual inspections of results were repeated, maintaining the IT search criterium, and adding the three broad areas of management accounting practice: costing, budgeting and performance management. For “costing”, 13 journal articles were returned. However, they were not directly relevant to our study as they focus solely on manufacturing firms (Maiga et al., 2014) or on specific approaches to costing (e.g. activity-based costing – Lee et al., 2010). For “budgeting”, 16 journal articles were identified. However, their relevance is limited as their context differs from that of our study. For example, Sofyani (2018) focuses on budgeting in a local government setting, and Kobelsky et al. (2008) involves large organisations in the US. Finally, for “performance management”, 32 journal articles were identified, but none of them are directly relevant as they focus on specific performance management methods and/or are conducted in research settings very different to those of our study (e.g. use of the Balanced Scorecard in Bahrain – Kamhawi, 2011). In general, for the three broad areas of management accounting practice, studies identified in our literature review involved contexts (location, industry, sample) very different to a SME context, which makes a comparison somewhat unreliable.

We also searched for journal articles containing the following search terms, which collectively represent the nexus of this paper: “information technology” and/or “IT”, “management accounting”, and “SME(s)”. No articles were identified. We can conclude from this review, and supported by Knauer et al. (2020), that there is an apparent lack of research on the impact of IT on the three main areas of management accounting practice within SMEs.

Management Accounting and Control Practices in SMEs

According to Lavia López & Hiebl, “research has long ignored the specifics of management accounting in SMEs” (2015, p. 81). In making this determination, they analysed 73 journal articles on management accounting in SMEs between 1985 and 2012. First, the small number of articles analysed within their review period supports the view that research on management accounting in SMEs is limited. Secondly, their review reveals interesting themes: SMEs use less management accounting than larger firms (Marc et al., 2010; Neubauer et al., 2012); within the SME cohort, medium-sized firms generally reported higher usage of sophisticated management accounting methods than smaller firms (Chand & Dahiya, 2010; Hopper et al., 1999) due to, for example, a lack of resources. Finally, SMEs are unlikely to use management accounting innovatively (Mitchell & Reid, 2000). More recently, Pelz (2019) reviewed 67 articles published in 25 journals up to 2017 and found that management accounting among small and new firms is beneficial as it allows management to deal with the challenges that growth invariably brings.

A review of the literature on management control in SMEs suggests that published studies are also relatively small in number. Davila (2005) suggests that the emergence of management control systems in small, growing firms is affected by the size, age, replacement of the founder as CEO and the presence of outside investors. Davila & Foster (2005) note that the time to establish budgeting systems is dependent on factors such as the presence of both venture capital and a financial manager, along with the number of employees. Davila & Foster (2007) find that budgeting systems are the most frequently adopted management control system in the initial stages of start-up companies. Their work also reports that the “number of employees, presence of venture capital, international operations, and time to revenue are positively associated with the rate of adoption” (2007, p. 907). Davila et al. (2015) suggest that management control systems in start-up companies provide management with controls and control information and positively affects firm value. Thus, they argue that more formal control systems in start-ups (which are typically SMEs) have substantial merit. Sandino (2007) provides similar findings from the US retail sector, suggesting that businesses first formalise what she terms “basic” management control systems, which are “used to collect information for planning and establishing the basic operations” (2007, p. 266).

Regarding the potential for management accounting to positively impact performance, Mia & Clarke (1999) and Waldron & Everett (2004) report that as competition intensifies, firms make greater use of the outputs from their management accounting practices to implement plans designed to improve their performance. In contrast, King et al. (2010) have found evidence of a positive relationship between the use of written budgets and performance among a sample of Australian primary healthcare managers. Furthermore, Marriott & Marriott (2000) interviewed owner-managers of small firms and found that if their external accountant provides them with a basic management accounting service that they understand, firm performance will subsequently improve. In contrast, research conducted by Cleary (2015) on indigenous firms (primarily SMEs) operating in the Irish information and communications technology (ICT) sector found a modest but statistically significant relationship between the use of advanced management accounting methods and a perceptual measure of performance. Finally, in the review undertaken by Lavia López & Hiebl (2015), some studies (King et al., 2010; Marriott & Marriott, 2000) claimed a positive relationship between the use of specific management accounting practices and firm performance, though no agreed consensus has yet emerged.

Having reviewed the relevant literature, we can deduce two main points. First, there is a general lack of research on the impact of IT on the primary areas of management accounting practice within SMEs, despite the benefits that technological developments purport to offer (Du & Cong, 2010; Robinson, 2011). Secondly, research on the use of management accounting practices to positively impact aspects of SME performance is scarce (e.g. Duréndez et al., 2016; Hakola, 2010). Therefore, this paper proposes and tests a conceptual model using PLS to determine CFOs’ perceptions of the impact of IT tools on management accounting practices and the perceived impacts of these on SME performance. In doing so, we respond to Ismail et al. (2019), who notes the lack of researchers studying the use of management accounting practices in SMEs, and to Nitzl (2016), who advocates the use of PLS in pursuing management accounting research.

3. Research Methodology

Research Context

The study context is Ireland. SMEs represent 99.8% of active Irish enterprises, employ 67.5% of those employed and generate 46.2% of total turnover (Central Statistics Office, 2021). Furthermore, Ireland scores highly on different indices measuring IT development, indicating advanced application and diffusion of different types of information systems.[1]

Using the Fame[2] database, we adopted the following search criteria to refine our SME choice, which ultimately became our sample population. First, we included private Irish-based firms (i.e. with a trading address in the Republic of Ireland) with an annual turnover of more than €5 million. In addition, we used the SME definition from the European Commission (2005), whereby a “small” firm has an annual turnover of more than €2 million but less than €10 million. While this inevitably excludes many firms, it was a deliberate choice to disregard the smallest SMEs as, due to their size, it was assumed they would be unlikely to have formal accounting functions or have implemented the IT tools we focus on (Hiebl et al., 2015; Mitchell & Reid, 2000). Secondly, we chose SMEs with more than 50% of their shareholding reported as Irish-owned to exclude firms that are non-national (not majority Irish owned, i.e. foreign owned), thereby ensuring that those firms that did participate were local (i.e. indigenous). Thirdly, we included only family-owned firms. About 70–75% of all businesses in Ireland are family-owned. A family-owned company is defined as one where family members hold more than 50% of shares or have majority control of the board of directors. Finally, we only selected firms with more than 10 full-time permanent employees, as SMEs with less than this number would likely have quite rudimentary accounting systems, if any. Based on these criteria, the Fame database generated an initial dataset of 456 firms. However, to retain our focus on SMEs and the integrity of our selection criteria, we manually filtered out those companies not adhering to these criteria, specifically: holding companies, financial services companies, and dormant companies. The dataset then comprised 426 companies.[3]

Survey Design and Data Collection

The survey instrument[4] was designed and administered using the Qualtrics software application. It was based on work conducted by Rikhardsson et al. (2012), who had conducted a similar survey in Iceland, where most firms (as in Ireland) are SMEs. Elements of this survey instrument were also used by Rikhardsson et al. (2015) and Batt et al. (2021). Academic colleagues and a number of financial executives working in the SME sector tested the survey instrument, and suggestions were incorporated into the final version. We limited the length of the survey to try to increase the response rate; pre-tests showed it took 10–12 minutes to complete. The survey was initially administered via email, followed by three reminders to the CFO or equivalent of each participating SME. This cohort was chosen as they would be expected to have a comprehensive knowledge of both the IT tools and management accounting practices within their respective firms. Reasons for non-response included time pressure, company policies precluding taking part in such surveys and invalid email addresses. The final sample population was 361, and 109 (30%) completed the survey, which compares favourably with survey-based research in management accounting (Hägg, 2003; Hiebl & Richter, 2018). The data collection phase of the study occurred between late 2016 and mid-2017. Within the 109 completed surveys there is a small amount of missing data, which was interpolated based on the average responses received. A t-test was used to ensure there is no difference between respondents and non-respondents and to compare early and late respondents. The results reveal no significant differences between the groups.

The SMEs in our sample were founded between 1900 and 2010 and, on average, are 42 years old. As shown in Table 1, the retail sector provided the highest number with 12 (11%) responses, followed by construction at 11 (10%) and manufacturing at 10 (9%). The ‘other’ category to which 19 (17%) respondents indicated that their firm belonged, included the motor industry, distribution, education and hospitality. The highest proportion of firms in our sample (n = 51; 47%) had a minimum turnover between €21 million and €50 million, while 52 firms (48%) reported having a minimum number of permanent and full-time staff employed in Ireland of between 51 and 250 employees. Collectively, these figures indicate a prevalence of medium-sized firms in our sample.

In terms of gender, 78% (n = 85) of respondents were male and 22% (n = 24) female. When questioned as to their highest level of education attained, 37% (n = 40) indicated an undergraduate degree, 39% (n = 43) a master’s degree and 3% (n = 3) a PhD degree. As shown in Table 2, for nearly 28% (n = 30) of respondents, the average length of time in their current position was between five and 10 years, with 41% (n = 45) for more than 10 years. For over 62% (n = 68) of respondents, their average age was 35–50 years, with 30% (n = 33) in the 50–65 age bracket. Nearly 84% (n = 91) of respondents confirmed that they are professionally qualified accountants, with membership of Chartered Accountants Ireland (n = 39; 43%) the most popular, followed by ACCA (n = 22; 24%), CPA Ireland (n = 13; 14%) and CIMA (n = 10; 11%).

Variable Measurements

Our survey focused on the three main areas of management accounting practice: costing practices (CP), budgeting practices (BP) and performance management practices (PMP). A combination of traditional and advanced management accounting practices is considered within each area, some of which have previously been tested (Cleary, 2015), but not within an SME setting. The practices chosen were corroborated by consulting the leading textbooks recommended for the study of management accounting at Irish universities such as Drury (2018), Horngren et al. (2014) and Seal et al. (2019). Respondents were not provided with definitions for any of the management accounting practices. The variable measurements discussed in the following are inspired by Rikhardsson et al. (2012), many of which have subsequently been used by Rikhardsson et al. (2015) and Batt et al. (2021).

To measure the costing practices used by each SME, CFOs were asked to outline their interest among six different practices listed. The practices were: contribution analysis; activity-based costing; target costing; Kaizen costing; life-cycle costing; and full-cost (absorption) accounting. On a six-point Likert scale respondents could choose: 1 = In use; 2 = Little interest; 3 = Average interest; 4 = No interest; 5 = Tried, but no longer used; or 6 = Unknown method.

To measure the use of different budgeting practices, as in Ekholm & Wallin (2011), CFOs were asked, based on a list of six different budgeting practices, to indicate the level of interest in each within their organisation. The six practices were: beyond budgeting; activity-based budgeting; Kaizen (continuous improvement) budgeting; rolling forecasts; zero-based budgeting; and project budgeting. The same six-point Likert scale, as outlined above, was utilised.

Based on the previously mentioned management accounting literature and textbooks, an additional list was compiled to gather further knowledge on the different operational budgets prepared by the SMEs in our sample. These budgets included sales, inventory, production, labour, capital, materials, balance sheet, income statement and cash flow. A four-point ordinal scale was used to measure whether these budgets were prepared: 1 = Annually; 2 = If needed; 3 = Never; or 4 = Not applicable.

To measure the performance measurement practices used by each SME, CFOs were asked, based on a list of six different practices, to indicate how applicable each is to their firm. The six different practices were: Balanced Scorecard; Lean management; business excellence; strategy maps; policy deployment; and Six Sigma. On a six-point Likert scale, respondents could choose: 1 = In use; 2 = Strong interest in using; 3 = Some interest in using; 4 = No interest in using; 5 = Tried, but no longer used; or 6 = Don’t know. We also asked if the performance indicators used by each SME were financial, non-financial or hybrid. On a five-point Likert scale, respondents could choose: 1 = Only financial; 2 = Mostly financial; 3 = Equal financial/non-financial; 4 = Mostly non-financial; or 5 = Only non-financial.

To measure the use of IT tools implemented and used, CFOs were asked about 12 different tools, which were chosen to exemplify the different categories of business information systems (Laudon & Laudon, 2020). We chose tools that are potentially applicable to most types and sizes of companies (Laudon & Laudon, 2020). These were: portal access for customers (transaction processing); access to IT systems through cloud technologies (knowledge work systems); continuous internal auditing/monitoring (decision support system); data warehouse (infrastructure system); customer relationship management (management information system); content management (knowledge work system); quality control systems (decision support system); online business (knowledge work system); time recording/tracking systems (transaction processing); and social media at work (knowledge work systems). On a six-point Likert scale respondents could choose: 1 = In use; 2 = Strong interest in use; 3 = Some interest in use; 4 = No interest in use; 5 = No longer used; or 6 = Don’t know. The final two tools were ERP systems (transaction processing and decision support) and business intelligence (decision support systems and management information systems), and on a four-point Likert scale, respondents could choose: 1 = No; 2 = Used for the past 1–3 years; 3 = Used for more than 3 years; or 4 = Don’t know. The difference between the scales is explained by the assumption – based on industry reports and studies of IT diffusion – that most companies have already implemented some type of ERP system and some type of business intelligence solution (TecTeam, 2021; Xu et al., 2019). We have not hypothesised any specific impacts of IT tools on specific management accounting practices beforehand. These are the links we are looking for in this exploratory research.

Finally, a series of statements were provided to CFOs to garner their perception of how the collective use of management accounting practices/information within their firm impacts on its performance. This use of perceptual measures to gauge performance impact has been cited as a reasonable alternative to the use of objective measures (Dess & Robinson, 1984; Venkatraman & Ramanujam, 1986). It has also been claimed to be strongly correlated with the use of objective financial performance measures (Hansen & Wernerfelt, 1989). Furthermore, it has been suggested (Van der Stede et al., 2005) that the use of subjective/perceptual measures of performance impact may be superior to other types of measures, as from the perspective of a survey respondent they represent their view of reality. An additional benefit of using perceptual measures of performance impact is that they simultaneously capture different aspects of performance (financial, non-financial, quantitative and qualitative) (Mia & Clarke, 1999).

Respondents were provided with six different statements: Management accounting techniques/information (MA) improves overall business performance; MA assists your organisation to outperform rivals; MA helps retain competitive advantage; MA enhances reputation; MA enhances shareholder/firm value; and MA enhances strategic decision-making. On a five-point Likert scale, respondents could choose: 1 = Strongly agree; 2 = Somewhat agree; 3 = Neither agree nor disagree; 4 = Somewhat disagree; or 5 = Strongly disagree. Respondents were requested to consider these statements in the context of their firm’s entire suite of management accounting practices (i.e. costing, budgeting and performance measurement).

Consistent with other management accounting-related studies (Homburg & Stebel, 2009), we included the following three control variables in our analysis, as each can impact our sample’s performance. First, firm size[5] (CV1), as the scale of a firm’s development, may affect its future performance (Marc et al., 2010; Neubauer et al., 2012). Secondly, industry classification[6] (CV2), as firms’ use of IT tools and/or management accounting practices, and their potential impact on performance, may vary between sectors (Asiaei & Jusoh, 2015). Finally, CFO tenure[7] (CV3), as the longer that CFOs remain in situ, the greater their impact on the performance of their respective firms (Engel et al., 2019).

Table 3 outlines each of the survey items comprising the constructs used in this study, along with the mean and standard deviation (SD) and the applicable scale range for each construct. Finally, Table 4 outlines the mean and standard deviation of each construct, all of which will be described in detail in the next section.

Structural Equation Testing

IBM SPSS software was used to analyse the raw data, with PLS – Graph Version 3.0 adopted for PLS analysis. PLS is a method of structural equation modelling that allows estimating complex cause–effect relationship models with latent variables. PLS does not require multivariate normal data and places minimum requirements on measurement levels (Chin, 1998a). As a result, it works very well on complex models and makes practically no assumptions about underlying data (Hair et al., 1987). The rationales behind our choice of statistical approach are as follows. First, PLS has previously been used in management accounting research (Bergmann et al., 2020; Chang et al., 2013; Cleary, 2015; Hall, 2011). Secondly, PLS is suggested to be a suitable approach for exploratory management accounting-based research (Nitzl, 2016). Thirdly, some academics (Chenhall, 2003; Chin, 1998a; Luft & Shields, 2014; Shields, 1997) have stressed the importance and value of using PLS in management accounting research. The inherent flexibility of PLS facilitates an evaluation of the interplay between theory and data simultaneously, thereby enabling a range of research models to be tested holistically. Finally, PLS is recommended for analysing smaller datasets (Hoyle, 1999). Indeed, the use of PLS requires adherence to a minimum sample-size requirement. The protocol (Barclay et al., 1995; Chin, 1997) for any PLS study containing ‘reflective’ indicators is 10 times the largest number of antecedent constructs leading to an endogenous construct. Based on this study’s proposed conceptual model (Figure 1), the minimum acceptable sample size is 40 (4 antecedent constructs × 10). With 109 responses, the use of PLS is thus appropriate (Barclay et al., 1995).

In assessing any PLS model, the primary objective is to maximise the amount of variance explained. This is achieved with reference to the R2 values of the endogenous constructs and the statistical significance of the relationships among the constructs contained in the model (Barclay et al., 1995). However, before determining this, the validity and reliability of the measurement model must be confirmed. Thus, initially, the reliability of the items within each construct is assessed. For well-established items, the standard protocol is to accept those with loadings of 0.70 or more (Carmines & Zeller, 1979). However, as this study is exploratory, the use of the 0.50 loading threshold was deemed appropriate. This is supported by Chin (1998b) and Hair et al. (1987), who suggest that at the initial stages of scale development (as is the case here), items with a minimum loading of 0.50 are generally acceptable. Hulland (1999, p. 198) also supports this view when he states that; “items with loadings of less than 0.40 […] or 0.50 should be dropped”.

As displayed in Table 5, the following items failed the 0.50 loading threshold level and were removed from further analysis: contribution analysis (CP1); financial/non-financial indicators (PMP7); portal access for customers (ITT1); access to IT systems through cloud technologies (ITT2); continuous internal auditing/monitoring (ITT3); time recording/tracking systems (ITT9); ERP systems (ITT11); and business intelligence (ITT12). The remaining items in each construct were then re-evaluated by examining their corrected item-to-total correlation score, the minimum threshold being 0.35 (Saxe & Weitz, 1982). Following this, one additional item was removed (see Table 5), i.e. rolling forecasts (BP4).

A matrix of loadings and cross-loadings was then produced to test the discriminant validity of the remaining items in each construct. As Table 6 illustrates, all remaining items had higher loadings with their corresponding constructs when compared to their cross-loadings. Therefore, each has adequate discriminant validity. Taking the first item, CP2 (activity-based costing), as an example, it loaded onto the costing practices (CP) construct at a value of 0.646, which is higher than any of the other values at which it loaded onto the remaining constructs. Therefore, it can reasonably be claimed that CP2 is most appropriately positioned as an item in the CP construct.

Attention then shifts from items to constructs. Internal consistency is evaluated using the Fornell & Larcker (1981) measure in addition to Cronbach’s Alpha – both require minimum scores of 0.70. In terms of convergent validity (an additional reliability test), the minimum acceptable result as outlined by Fornell & Larcker (1981) is 0.50. For internal consistency, all five constructs used satisfied the 0.70 threshold required for both tests (see Table 7). For convergent validity, three of the constructs fell slightly short of the required 0.50 level, i.e. costing practices (CP) at 0.4963, budgeting practices (BP) at 0.4356 and IT tools (ITT) at 0.4211. However, the exploratory nature of these constructs, coupled with the fact that they have met and exceeded all other statistical validation requirements, renders these results acceptable.

Finally, discriminant validity examines the level to which a construct shares more variance with its items than with the other constructs in a conceptual model. In conducting this test using a correlation matrix, Fornell & Larcker (1981) recommend using the average variance extracted (AVE) equation. For appropriate levels of discriminant validity, values along the diagonal of the correlation matrix (square root of the AVE for each construct) should be greater than the corresponding values in each row or column (Hulland, 1999). All five constructs used in this study satisfy this requirement (see Table 8), apart from the correlation between the CP construct and BP, which at 0.670 is slightly higher than the figure generated for BP itself at 0.660. However, the exploratory nature of this research, coupled with the robustness of most of the statistical testing undertaken, renders this acceptable.

Having ascertained the statistical validity and reliability of the ‘measurement model’, the proposed conceptual model can now be evaluated. A jack-knife analysis was performed within the PLS – Graph software application using a program developed by Fornell & Barclay (1983). Compared to traditional t-tests, jack-knifing facilitates testing the significance of parameter estimates from data not assumed to be multivariate normal (Barclay et al., 1995).

4. Results and Discussion

Before outlining the proposed conceptual model results, some general comments are worthy of a brief mention. First, the costing practices in use by the respondent SMEs are more traditional (contribution analysis, absorption costing) at 77% (n = 84) of respondents, which is consistent with Cleary (2015), despite the reported advantages of more sophisticated methods such as activity-based costing (Kennedy & Affleck-Graves, 2001). Regarding the use of budgeting practices, rolling forecasts (42%; n = 46) emerged as the most widely used approach, followed by project budgeting (23%; n = 25). Performance management practices are more varied, with 19% (n = 21) using the Balanced Scorecard, followed by lean management and business excellence at 15% (n = 16). Finally, the item PMP7, which considered the composition of performance indicators, revealed that over 64% (n = 70) of SMEs are using only/mostly financial performance indicators.

Collectively, these insights suggest an apparent reluctance among Irish SMEs to implement more sophisticated/advanced costing, budgeting and performance management practices. Despite a prolonged economic downturn in Ireland from 2007/2008 onwards (Donovan & Murphy, 2013), it would have been expected that following the crisis, firms would update their management accounting systems to the levels of sophistication prevalent in other EU countries (Endenich, 2014; Pavlatos & Kostakis, 2015; Rikhardsson et al., 2021). This reluctance to change can be explained by the impact of the financial crisis on these firms. The crisis impacted heavily on the Irish economy, and in the following years new priorities emerged, such as an increase in information flow to outsiders due to increased regulatory demand for mandatory disclosures (Van der Stede, 2011). As a result, the level of resources necessary to change their management accounting practices may not have been available to SMEs. Although the prevalence of professionally qualified accountants in our sample is unsurprising, it does suggest that Irish SMEs may not be subject to the suggestion by Hiebl et al. (2015) and Songini & Gnan (2015) that a lack of professional management (including accountants) is a reason small and/or family-owned firms do not develop formal, or more advanced, management accounting and control practices.

A reason for these results could be the amount of time and resources it can take for substantial and prolonged change to become embedded within firms’ accounting functions. For example, it took 25 years for the net present value (NPV) approach to be used widely (Pritsch, 2000, as cited in Möller et al., 2020), while Schäffer & Matlachowsky’s (2008) study (as cited in Möller et al., 2020) demonstrates that the implementation of projects such the Balanced Scorecard can take years, with no guarantee of success. Nevertheless, our findings are consistent with research conducted among SMEs in Malaysia (Azudin & Mansor, 2018) and the reported lower usage of management control systems among family-controlled firms in Austria and Germany (Speckbacher & Wentges, 2012).

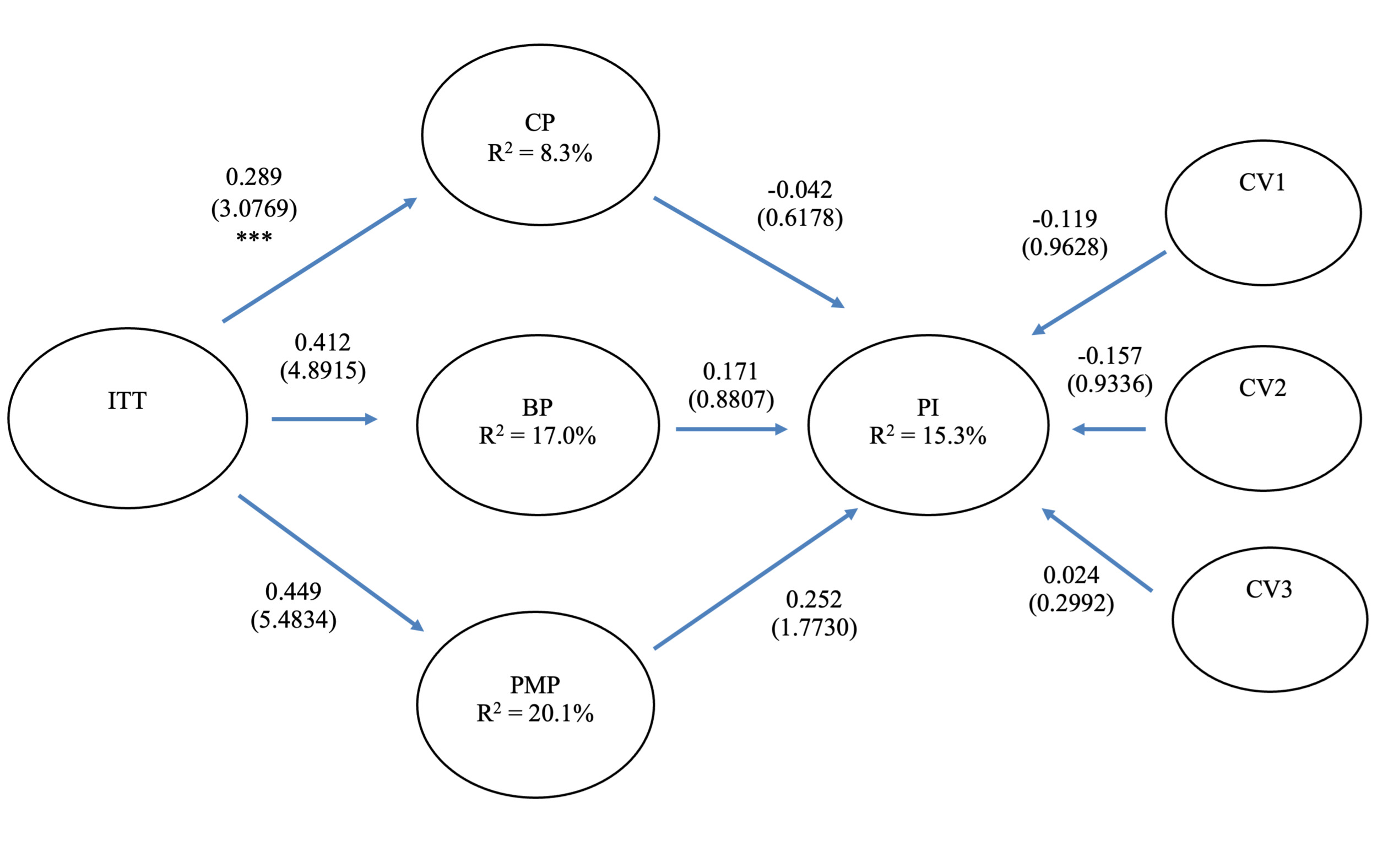

The proposed conceptual model suggests that CFOs (or equivalent) surveyed perceive that IT tools (ITT) positively affect the main management accounting practices of their respective SMEs. CFOs also perceive that these practices positively affect aspects of performance (PI). The results displayed in Figure 2 suggest that ITT use is positively correlated with each of the three main areas of management accounting practice. For CP, the beta path coefficient is positive (0.289) and statistically significant at a p < 0.01 (t = 3.0769); for BP, the beta path coefficient is also positive (0.412) and statistically significant at a p < 0.01 (t = 4.8915); while for PMP, the beta path coefficient connecting this construct with the ITT construct is similarly positive (0.449) and statistically significant at a p < 0.01 (t = 5.4834).

These results support research linking the use of IT and management accounting (Cleary, 2018; Granlund & Malmi, 2002; Suddaby et al., 2015). They also support suggestions that advances in IT have the potential to make a significant difference to how budgeting operates within firms (Taipaleenmäki & Ikäheimo, 2013) or the claim that IT usage is a contributory factor in the increased use of performance management systems in SMEs (Garengo et al., 2005). However, as the use and importance of IT tools continues to evolve rapidly, SMEs must maintain and develop their data infrastructure (including accounting) to facilitate better data management, thereby creating more opportunities to use their data for competitive purposes (Bergmann et al., 2020). The emergence of the digital economy may have multiple implications for SMEs. Due to their increased reliance on digital technologies, the proliferation of ‘big data’ generated by such firms has created opportunities for management accountants and others to derive value/meaning from areas such as data visualisation and performance measurement (Cockcroft & Russell, 2018). Those SMEs that respond proactively to this challenge are likely to reap significant benefits, at the expense of those that fail to do so. Consequently, the positive impact and importance of IT Tools on management accounting within SMEs, as suggested by this paper, is likely to increase in the future.

Regarding CFOs’ perceptions of the impact of each of the three areas of management accounting practice on PI, the statistical results are also outlined in Figure 2. The beta path coefficient connecting CP with PI is negative (-0.042) and statistically insignificant (t = 0.6178). For BP, although the beta path coefficient is positive (0.171), it is statistically insignificant (t = 0.8807). However, for PMP, the beta path coefficient is both positive (0.252) and statistically significant at a p < 0.10 (t = 1.7730). Collectively, these results provide partial and limited support for the suggestion that CFOs perceive management accounting practices as having a positive impact on SME performance (e.g. Cleary, 2015; Duréndez et al., 2016; King et al., 2010; Marriott & Marriott, 2000), although extant research findings are inconclusive.

Our findings are consistent with those from Pedroso et al. (2020), who surveyed the CFOs of SMEs in Portugal but did not find a direct connection between management accounting systems and firm performance. However, our findings are at odds with Sandalgaard & Nielsen (2018), who found that, for example, budgets are positively associated with improved firm performance among SMEs in Denmark. As was the case with our study, both of these papers also evaluated firm performance using perceptual measures.

This divergence of results suggests two things. First, the use and potential impact of management accounting practices within SMEs appears to be contingent on the particular circumstances facing each firm (Ittner & Larcker, 2001). However, there is a growing body of research (e.g. Pelz, 2019) indicating some support for the possibility that particular management accounting practices can positively impact on elements of performance, thus encouraging SMEs to consider using their existing practices in an innovative manner and/or to contemplate using others. As with all firms, any means by which to gain a competitive edge should be taken and the use of management accounting practices may yet play a more prominent role in this regard. Secondly, and linked to the above, more research is needed to enable more definitive pronouncements to be made regarding the use and impact of particular management accounting practices within SMEs (e.g. Ismail et al., 2019; King et al., 2010).

To assess the predictive power of the conceptual model, the R2 value of each endogenous construct contained therein was considered: CP 8.3%, BP 17.0% and PMP 20.1%. Taken together, they suggest that, based on the perceptions of the CFOs who responded to the survey, ITT appears to have the greatest influence on PMP. Further research is needed to determine how, and in what form, this occurs in practice. The R2 value for the PI construct at 15.3%, although modest, indicates some level of support for the proposition that the CFOs who participated in this research perceive that the use of management accounting practices does impact the performance of their respective SMEs. As mentioned above, the fact that most respondents are members of professional accountancy bodies that emphasise financial reporting (i.e. Chartered Accountants Ireland, ACCA, CPA Ireland) rather than management accounting (i.e. CIMA) may partially explain this finding. However, more research is needed to determine if this claim can be supported.

As Figure 2 shows, none of the control variables tested (firm size (CV1),[8] industry classification (CV2),[9] or CFO tenure (CV3)[10]) have any statistically significant influence on the performance impact of the SMEs included in our sample. This outcome increases our trust and confidence in the reported results.

5. Concluding Comments

Over 20 years ago, Mitchell & Reid (2000) stated that research on management accounting and control in SMEs was limited, and since then similar claims are still being made (Heinicke, 2018; Ismail et al., 2019). This is despite the significant contribution of SMEs to wealth creation, employment levels, exchequer returns, etc. In a rapidly changing business environment (Otley, 2016), firms (including SMEs) continually seek innovative ways to gain a competitive edge. The use of management accounting practices, supported by appropriate IT tools, has been cited as one possibility in this regard (Cleary, 2015; Duréndez et al., 2016; King et al., 2010; Marriott & Marriott, 2000).

This paper makes three contributions. First, we examine the perceptions of CFOs on the impact of IT tools on the three main areas of management accounting practice (costing, budgeting, and performance management). The results suggest that CFOs perceive the use of IT tools to be positively significant, associated with each of these areas, which provides support for research suggesting that within the accounting function the use and influence of technology is common (Cleary, 2018; Granlund & Malmi, 2002; Suddaby et al., 2015). Furthermore, when considered with the finding from Knauer et al. (2020) that upgrading IT/IS can increase a firm’s management accounting data quality, thereby leading to better decisions, it may encourage firms (including SMEs) to increase their investment in this area. Indeed, the suggestion that digitalisation will soon have a significant impact on the operation of management accounting practices may accelerate this process (Möller et al., 2020). It has been reported that some businesses have begun using artificial intelligence (AI) to automate some of their more routine accounting processes in an attempt to improve their accuracy and efficiency, as well as reducing their operating costs. CIMA has recognised this increased reliance upon IT in this accounting domain, indicating that to continue to add value in this technological environment, management accountants need to enhance their skills in areas such as digital literacy and advanced technological know-how (Noah, 2019). Those SMEs, and their respective management accountants, that heed this advice should be well-positioned to realise the benefits that can accrue from the use of disruptive technologies such as AI, blockchain, data analytics, and so forth.

Secondly, this study examines the perception of CFOs of the impact of management accounting practices on the performance of their respective SMEs. Partial and limited statistical support was found, despite Hofer et al.‘s (2015) claim that the use of more accurate forecasts could be beneficial to firms operating in volatile trading environments, or by Henri (2006), who reports a similar finding concerning SMEs’ use of performance management systems. An explanation for these findings may be that, owing to limited resources (financial and human), SMEs do not possess the requisite knowledge to maximise their usage of certain management accounting practices by producing bespoke reports to aid more informed decision-making (Halabi et al., 2010). It could also be, as reported by Knauer et al. (2020) in research conducted on German firms, that a significant number are using outdated IT/IS in management accounting, resulting in substantial deficiencies. The findings reported here contribute to the debate as to whether the use of management accounting practices can positively impact aspects of SME performance. To date, the evidence has been both scarce and inconclusive, despite the prevalence and importance of such firms globally (Lavia López & Hiebl, 2015). In doing so, this paper has also proactively responded to Ismail et al. (2019), who remarks on the lack of researchers studying the use of management accounting practices in SMEs

Finally, this study outlines a methodological approach (PLS) for the consideration of those engaging in exploratory management accounting research. One benefit of the PLS approach is that, unlike other methods, it enables a simultaneous evaluation of the interplay between theory and data, which facilitates a range of research models to be tested holistically (Chenhall, 2003; Chin, 1998a; Luft & Shields, 2014; Shields, 1997). By using PLS, this paper also responds to Nitzl’s (2016) call for more management accounting researchers to do so. Although the results from the conceptual model present some interesting findings, they require further testing and analysis before any claims of theory development can be confidently made. However, we hope that the comprehensive PLS approach outlined here will encourage others to use it to engage in further explorative research, which may (eventually) increase understanding of the role that IT tools and management accounting practices can play in SMEs.

There are limitations to this study. First, it is conducted in a single country; it cannot be excluded that national culture has impacted the results obtained. Secondly, this study is exploratory in the sense that some constructs used (although based on Rikhardsson et al., 2012) are novel. Thus, further statistical testing is needed to confirm their validity. Thirdly, as most of the survey questions were Likert scale in nature, their use precludes any follow-up questions in response to, for example, inconsistent answers. Fourthly, as each respondent was requested to answer on behalf of their respective SME, social desirability bias is possible. Respondents may feel compelled to answer questions to present a ‘more favourable’ scenario than exists within their organisation (Konrad & Linnehan, 1995). Concerns about such behaviour in self-administered surveys are inconclusive (Dillman, 1978; Podsakoff & Organ, 1996; Saunders et al., 2002). Finally, this study targets responses from a single source in each SME: the CFO or equivalent. Accumulation of variables from one individual may result in common-method bias (Chong & Chong, 1997). Future research could garner the views of a variety of other organisational actors. This would also address the concerns expressed by Van der Stede et al. (2005), who argue that no one person can reasonably be expected to articulate the views of a whole organisation. However, the fact that the vast majority (84%) of respondents are professionally qualified accountants provides some comfort here.

There are several future research avenues. First, research examining the management accounting and control practices of SMEs is limited. Therefore, developing in-depth case studies in how SMEs use management accounting practices to impact their performance would be extremely interesting and add to our understanding. Secondly, the survey items developed and used in this study could be replicated by focusing on specific industries to ascertain if the results obtained here also apply in particular sectors. Thirdly, this study has focused on a conceptual model of IT tools that affect management accounting practices. Future work could adapt the model and items presented here to study how IT affects the role of the management accountant in SMEs; specifically, the impact of big data and data analytics is an area that warrants future research effort. Finally, Otley (2001) states that it is unusual for researchers to reproduce prior work in management accounting research. However, we would welcome other researchers using our survey instrument in other studies. This is in keeping with the suggestion of Goretzki & Strauss (2018) for more comparative international management accounting studies.

See ITU’s ICT Development Index 2017, on which Ireland is ranked as number 20 out of 176 countries. https://www.itu.int/net4/ITU-D/idi/2017/index.html

Fame is a source of company information in the UK and Ireland and contains company accounts, ratios, activities, ownership, and management for the largest 2.6 million companies.

The anonymous nature of responses did not allow us to test for non-response bias.

A copy of the survey instrument is available on request.

CV1 is the control variable for ‘size’. It is based on the number of full-time permanent employees, with ‘0’ representing ‘small’ firms and ‘1’ representing ‘medium/larger’ enterprises as per the European Commission’s definition of same (https://ec.europa.eu/growth/smes/sme-definition_en).

CV2 is the control variable for ‘industry classification’, with ‘0’ representing ‘manufacturing’ companies and ‘1’ representing ‘service’ companies.

CV3 is the control variable for ‘CFO (or equivalent) tenure in current position’, with ‘0’ representing ‘tenure of up to 5 years’ and ‘1’ representing “tenure beyond 5 years’.

See above, footnote 5.

See above, footnote 6.

See above, footnote 7.