Introduction

With ageing demographics being experienced across western societies, policymakers have become increasingly aware of pension funding problems. As government resources have approached turning points in terms of adequacy, alternatives are being sought to provide for, or at least supplement, retirement income (Jones et al., 2012; Naumanen & Ruonavaara, 2016). In order to ease the burden on the Exchequer, some researchers (Elsinga, 2011; O’Mahony & Overton, 2015) recommend that individuals provide for their own retirement by utilising their accumulated (financial, physical or, occasionally, intellectual) assets. This may be possible through ‘asset-based welfare’ policies (Regan & Paxton, 2001). On the other hand, the behavioural life-cycle (BLC) hypothesis suggests that individuals are reluctant to spend their accumulated assets, especially housing equity, in retirement (Shefrin & Thaler, 1988).

Elsinga and Hoekstra (2005) explain that asset-based welfare policies provide opportunities for households to accumulate assets in a convenient manner which can escalate in value over time. This reduces the reliance on state-managed social transfers to counter the risk of poverty in retirement (Doling & Ronald, 2010). Ireland has experienced high rates of home ownership due to households being provided with fiscal stimuli to encourage home ownership (Norris & Fahey, 2011). The home ownership rate among the elderly (65+ years) Irish stands above 85% in 2018 and consists of two thirds of the elderly’s aggregate gross wealth (CSO, 2018). Thus, housing equity may have the potential to supplement retirement income for existing Irish retirees (Jaiyawala et al., 2018).

At present, Ireland has a well-developed old-age pension system comprising of three pillars: (i) the State Pension; (ii) occupational pensions; and (iii) private pensions, which attract substantial tax expenditures by the Exchequer (Mulligan, 2019). As acknowledged by Holzmann et al. (2008), the World Bank recognises a five-pillar system (pillars 0 to iv) in its conceptual framework in assessing pension systems across the globe. The first two pillars (pillars 0 and i) are similar to pillar i and ii in the Irish context, while pillars ii and iii refer to funded mandatory individual savings accounts and voluntary private savings, respectively. The fifth pillar (pillar iv) is non-financial in nature and includes home ownership and reverse mortgages. Currently, there is little published evidence of withdrawal of housing equity as a retirement income source in Ireland and should it emerge as a material economic phenomenon, it could be categorised as a fourth pillar in Ireland because of its distinct attributes.

Despite having a well-established pension system, the OECD (2019) observes that Ireland has one of the lowest net pension replacement rates (35.9%).[1] If no action is taken, the net replacement rate is likely to decline substantially in the next three decades due to a significant rise in the age dependency ratio (Hennecke et al., 2017). It can be expected that low pension replacement rates will trigger more interest in other retirement funding options, including withdrawal of equity from housing.

The above discussion suggests that housing equity in retirement can play a modest yet worthwhile role in easing the budgetary pressure on the Exchequer with regard to the provision of retirement income (Elsinga, 2011). Further, Hennecke et al. (2017) find Ireland to have modestly favourable conditions for the ERS market. This study seeks to add to the extant literature through its exploration and analysis of new evidence. Thus, it examines aspects of housing equity withdrawal by elderly households through exploring the preferences and mediums of using housing equity in retirement.

The authors use a well-established focus-group technique to provide insights into the perceptions of elderly[2] Irish regarding the withdrawal of housing equity. The findings suggest that these perceptions are evolving. Although there is little evidence of housing equity withdrawal through any medium at present, there is a latent need for such possibilities, primarily to improve the standard of living in retirement. The attitudes towards the bequest motive make such desires to tap into housing equity reserves even more apparent. Following these findings, the State may have opportunities to establish a policy framework for elderly homeowners to facilitate them in utilising housing equity.

The rest of the paper is organised as follows. First, a literature review regarding the theory underpinning the study is presented followed, by the existing research on asset-based welfare, the meaning of home ownership and housing equity withdrawal. This is followed by the research objectives and an outline of the methodology employed for the study. The key findings and analysis of the research are then presented. Finally, the discussion and conclusion are drawn from the findings.

Literature Review

The literature review provides a synthesis of the theoretical background, asset-based welfare in retirement, attitudes towards home ownership, ways of releasing housing equity, and household considerations of withdrawing housing equity.

Life-cycle and Behavioural Life-cycle Theory

This research is underpinned by the influential economic theory, the life-cycle hypothesis (LCH) (Doling & Elsinga, 2013; Naumanen & Ruonavaara, 2016; Toussaint, 2011). This theory holds an underlying assumption that individuals/households attempt to smooth their expenditure throughout their lifetimes in such a way that their investment and expenditure strategy can maximise utility at all life stages (Modigliani & Brumberg, 1954). Individuals are presumed to have lower income and little or no savings/assets in younger life, higher income and some savings/assets in middle age, and little income and higher savings/assets in retirement (Regan & Paxton, 2001).

According to the LCH, individuals are assumed to liquidate their assets (including housing equity) accumulated over their working lives as their incomes contract in retirement. Furthermore, Aalbers (2008) suggests that a home should no longer be considered as just a place to live but also an investment asset that can be deployed as an instrument to accumulate and decumulate equity strategically. It may be natural to postulate that individuals would release housing equity in order to maintain consumption levels (Bonvalet & Ogg, 2008; Chiuri & Jappelli, 2010; Rouwendal, 2009). However, many studies (Elsinga, 2011; Haffner, 2008; Naumanen & Ruonavaara, 2016; Toussaint & Elsinga, 2009) in Europe show contradictory findings which suggest that individuals are reluctant and suspicious of releasing housing equity in retirement for reasons such as aversion to debt, bequest motives, and associated costs.

This seeming contradiction in the behaviour of individuals/households may be explained by the behavioural life-cycle (BLC) hypothesis (Johnson et al., 2015; Kim & Hanna, 2015). This hypothesis was first explained and termed by Shefrin and Thaler (1988):

“Self-control, mental accounting, and framing are incorporated in a behavioural enrichment of the life-cycle theory of saving called the Behavioural Life-Cycle (BLC) hypothesis.”

Since long-term planning is required for retirement savings, self-control is necessary for individuals to supress the temptation of immediate consumption (Shefrin & Thaler, 1988). Mental accounting refers to individuals’ urge to view their wealth as non-fungible since they tend to frame their wealth using some sort of mental accounting to develop a hierarchy of spending based upon the type of wealth (Shefrin & Thaler, 1988). Individuals tend to spend more accessible wealth first (e.g. liquid assets such as cash and savings account), followed by financial assets (stocks, bonds, mutual funds), then housing equity. Hence, such behavioural traits may restrain households from smoothing their consumption in retirement (Thaler, 1990).

Similarly, framing refers to the phenomena that individuals’ decisions can be affected by the way choices are framed. In other words, when options with the same utility are framed differently, individuals will choose the one that is framed favourably. For example, individuals would prefer an option that offers a guaranteed $50 gain over an option that offers an equal probability of winning $150 and losing $50. This is because individuals tend to be more sensitive to losses than gains, as postulated by prospect theory (Kahneman & Tversky, 1979).

According to the BLC hypothesis, the marginal propensity to consume (MPC) – the change in consumption divided by the change in income/asset – is highest for current income, lowest for future income, and somewhere in between for current accumulated assets (Shefrin & Thaler, 1988). In other words, individuals tend to make the highest proportion of consumption from their current income, not so much from their existing accumulated assets, and the lowest proportion of consumption from their future income, perhaps due to constraints on borrowing. This behaviour relates to the system of mental accounting (Shefrin & Thaler, 1988) applied by households, as discussed above.

Also, the lower MPC from accumulated assets may be attributed to factors unique to respective countries. For instance, some countries (e.g. Ireland) may have government policies that promote home ownership without sufficient mechanisms for releasing housing equity at retirement, or may have complex tax systems combined with a lack of trust in financial institutions with regard to equity release mechanisms (Jaiyawala et al., 2018). On the other hand, for historical reasons, some countries (e.g. Germany, Finland) may be more receptive to ERS-type financial products when compared to others (Al-Umaray, 2018; Hennecke et al., 2017). This explains why individuals may be reluctant to use housing equity in retirement. Given the costs of liquidating property assets (legal costs, auctioneering costs, etc.), such a consumption function seems very rational in these circumstances.

Asset-based Welfare

An asset-based welfare premise suggests that individuals in an economy are more likely to prosper if they accumulate and acquire assets (Sherraden, 2003). The concept of asset-based welfare is referred to in the literature, including as an assistance in the eradication of poverty in society and for reducing an intergenerational inequality gap (Castles & Ferrera, 1996). At the beginning of the 21st century, it received attention from researchers in the field of housing who started to consider the role of home ownership with respect to the prospective pension funding challenge in some societies (Doling & Ronald, 2010; Jones et al., 2012).

Norris (2016) notes that the asset-based welfare system has deep roots in Ireland through an agricultural social movement and disputes with respect to ownership of farmland, especially in the 19th and early 20th centuries. Fahey and Maître (2004) argue that this was only the case at the end of the 19th century, as up to then rural and urban households in Ireland predominantly rented their homes. However, the State’s efforts in developing asset-based welfare policies by providing fiscal incentives such as tax relief on mortgage-interest payments helped Ireland to attain one of the highest rates of homeownership in the developed world which serves as a support in old age. Asset-based welfare policies enable individuals to be in control of their lives, develop capabilities and contribute to society and the economy (Sherraden, 2003).

Although asset-based welfare has proved to be a great support for the existing elderly (through mortgage interest relief), it has also resulted in the financialisation of residential property and asset inequality among the elderly and the younger generations (Hearne, 2017). More recently, mortgage interest relief has been abolished. Now the Government has a Help to Buy (HTB) incentive scheme (O’Toole & Slaymaker, 2020) targeted at first-time buyers, which involves a capital advance rather than an interest subsidy. With comparatively low interest rates now applying in a domestic context, a capital subsidy may be viewed as more immediate and visible compared to mortgage-interest relief.

Attitudes toward Home Ownership

Home ownership may have several motives such as personal value, emotional status, control and independence from landlords, stability and reduced fear of eviction, legacy for children, and a possible use in later life (Earley, 2004; Elsinga, 2011; Jones et al., 2012; Watson & Webb, 2009). While an accumulation of financial wealth can provide for consumption in retirement, an owner-occupied dwelling plays a dual role of providing shelter during the entire life along with being a part of a retirement portfolio (Easterlow et al., 2000).

The Central Statistics Office (Central Statistics Office, 2016) notes that housing assets of households in Ireland account for €429 billion out of a net wealth of €626 billion as estimated by the Central Bank of Ireland. Furthermore, the level of home ownership among those over 60 years of age is 85%, which is at a significantly higher level compared to most EU member states (Central Statistics Office, 2016). These data suggest that housing assets are vital for Irish individuals as a store of wealth. Research conducted by Jones et al. (2012) in Germany and the UK finds that many respondents in these jurisdictions considered rent as ‘dead money’ and home ownership is considered important and desirable due to its ease of access as an investment vehicle.

Rowlingson (2006) finds that there is considerable willingness among elderly individuals in the UK to withdraw housing equity for their needs. However, in the research conducted by Jones et al. (2012) in Germany and the UK, it was observed that none of the retired households in the UK or Germany are using any housing equity to support themselves in retirement despite having lower income. Elderly homeowners in both countries consider their homes as a form of a security in case of emergencies, and few can imagine a situation where they would choose to withdraw any equity from the homes. On the other hand, a study conducted by Chiuri and Jappelli (2010) in over 15 OECD countries found that there was a considerable fall in home ownership due to housing equity withdrawal after the age 60.

Housing equity withdrawal may have some consequences for individuals. Toussaint (2011) lists several aspects that are relevant when an owner-occupied home is to be used to supplement retirement income. For example, consumption of housing equity often creates psychological discomfort for older people and, in most cases, they will try to avoid it. Also, if housing equity is consumed, this can lessen the bequest to children, or other family members and relatives, who would otherwise inherit the dwelling (Christie et al., 2008; Overton, 2011). This is particularly important in countries with a weakly-developed welfare state and a strong degree of attachment to family (Jones et al., 2012). Informal concepts such as ‘the bequest motive’ and ‘having a nest egg in case of emergency’ serve to constrain individuals from using housing equity (Elsinga, 2011; O’Mahony & Overton, 2015; Toussaint, 2013), although Elsinga (2011) finds that those residing in liberal and social democratic countries do not consider legacy as important.

Methods of Releasing Housing Equity

Doling and Elsinga (2013) argue that the accumulation of housing equity can be utilised to meet income needs during retirement. In line with this, there has been a rising awareness of ERS in the US and some parts of Europe. Such schemes, if utilised efficiently, can provide a substantial amount to supplement the public pension (Overton, 2011). The other options for releasing equity from housing have been downsizing and sale-and-rent. However, these options are not believed to be attractive due to the strong attachment towards one’s home, especially in Ireland (Fahey & Maître, 2004). Housing equity withdrawal can also help in terms of easing the pension expenditure to GDP ratio for government. This may be achieved by reducing the overall reliance on public and/or the Non-contributory State Pension. This ratio was at 5% in 2015–2016 and is expected to rise to 5.5% by 2025 (OECD, 2019).

ERS allows homeowners to release equity from their homes while continuing to reside there until they have passed away or moved to care (Bielanska, 2016; Reifner et al., 2009). Reverse mortgages and home-reversion schemes are the two most common forms of ERS products (Al-Umaray, 2018; Bielanska, 2016; Reifner et al., 2010). Reverse mortgages (also called lifetime mortgages and loan model) allow homeowners to take out a loan on their property in the form of a lump sum and/or a monthly amount. At the end of a homeowner’s life, their heir has an option to repay the outstanding loan amount along with the accumulated interest either from the proceeds of sale of the home or from their own resources (Al-Umaray, 2018; Bielanska, 2016). A home-reversion scheme (sale model) requires homeowners to sell a whole or part share of their property to a financial institution which will pay the upfront lump sum at a significant discount to the market value of this share (Al-Umaray, 2018; Bielanska, 2016). Therefore, the share in the property that belongs to the financial institution is fixed at the outset and any element of surprise in terms of the repayment amount is eliminated.

The reverse mortgage type of ERS, as compared to the home reversion type, is more prominent across Europe with offerings in the UK, Ireland, Italy, Spain, France, Sweden, Poland and Portugal. Most of these countries saw a reduction in the offering of these products after the 2008 global financial crisis (Al-Umaray, 2018). There have been limited offerings in Ireland from 2018. Home-reversion schemes are more prevalent in Germany, while both types of product are offered in Hungary (Al-Umaray, 2018). Therefore, there is a noticeable variation in the types of product at offer and the extent of their use, depending on the macro-economic environment.

ERS products are complex and expose providers to a large range of risks such as a drop in house prices and a borrower’s longevity. Furthermore, as most providers offer a no-negative-equity guarantee, the risk is reflected in the pricing of these products (Terry & Gibson, 2010). Venti and Wise (2004) argue that, in the US, a reverse mortgage only makes a positive difference for retirees above 85 years of age. They also dismiss the myth that there are older people starving in large homes, providing evidence that retirees with very low disposable income also have a very low housing wealth. Therefore, ERS products only cater to a specific array of retirees. This is also true for Ireland as shown by the CSO’s Household Finance and Consumption Surveys (Central Statistics Office, 2018) over different years. Therefore, they may be suitable only for households with a modest level of retirement income and significant housing equity.

With respect to using ERS products as a medium for releasing housing equity, it is evident that after the 2008 global financial crisis trust in financial markets declined (Gustman et al., 2010; Sapienza & Zingales, 2012) and this is even more so the case in Ireland (Mulligan, 2019). As of 2018, the level of trust in business continues to decline in Ireland and it ranks the lowest among OECD countries in terms of trust in business (Edelman, 2019). Therefore, Irish financial institutions would need to improve their trustworthiness (Overton, 2011) as a prerequisite for providing income solutions relating to housing equity. This might be possible through regulation (Jones et al., 2012) or through increasing involvement of non-profits and/or governmental organisations (Reifner et al., 2009) in developing such products.

Research Objectives and Methodology

The BLC hypothesis suggests that individuals are likely to use their current income ahead of any accumulated assets in retirement. Furthermore, they are unlikely to use illiquid assets such as housing in advance of their liquid assets, such as savings or pensions, since MPC is higher for such liquid assets. This is in contradiction with the concept of asset-based welfare, which in a retirement context may gain more support with the tightening of State resources and likely escalation in the pension expenditure to GDP ratio.

The asset-based welfare concept is consistent with the original LCH (life-cycle hypothesis) which suggests that individuals tend to smooth their consumption with the apt use of accumulated assets in retirement. Thus, there are contradictory theoretical and conceptual positions in the extant literature as to how individuals are expected to behave in retirement. Further empirical research is required to assess the alternative theoretical positions postulated in the literature. With the greater proportion of wealth reposing in residential dwellings for the existing elderly in Ireland, there is an untapped source of retirement income. However, inheritances may be impeded greatly if housing equity is exploited widely.

Research Objectives

In light of the literature review, it is evident that an investigation of Irish attitudes towards home ownership and willingness to extract housing equity to supplement retirement income is warranted. The published research in this field has provided evidence from other countries and the Irish data may offer different perspectives due to a traditionally high level of home ownership, coupled with the subsequent housing crash and recovery, as well as a population profile with the lowest median age among the EU members states. Therefore, the following two research objectives are formed to address these issues:

-

to explore the attitudes of the elderly in Ireland towards home ownership and the use of housing equity to supplement retirement income; and

-

to determine the preferences of the elderly in Ireland for different mediums for the use of housing equity.

The next section details the research methodology. This is followed by the analysis and findings, which are structured around the research objectives.

Methodology

The exploratory nature of this study lends itself to a qualitative approach. We adopt a focus group (FG) approach to draw on participants’ beliefs, attitudes and experiences in a way that would not be attainable using other qualitative methods. In other words, these experiences, beliefs and attitudes are more likely to be revealed via social gatherings and interactions, which are made feasible by the focus group approach (Krueger & Casey, 2014). Barbour and Kitzinger (1999) acknowledge that focus groups are becoming a more established part of the methodological framework within the social sciences and other cognate disciplines.

Focus groups are used to achieve several goals, such as providing ‘social antenna’ (keeping governments informed about key issues emerging within society), improving communication, debating policy issues, and setting policy agendas (Hennink et al., 2010). Previously, qualitative techniques such as focus group interviews have been applied in numerous studies in several EU member states such as the Netherlands (see Toussaint, 2013), the UK (see O’Mahony & Overton, 2015), and Germany (see Jones et al., 2012) to conduct research on home ownership and housing equity withdrawal.

Focus Groups

Focus group interviews for financial research have been used effectively by several researchers (Atkinson et al., 2007; Black et al., 2002). Flexibility within focus group settings enabled an exploration of the elderly’s perceptions of the withdrawal of housing equity (Beckett et al., 2000). Krueger and Casey (2014) advise that the number of focus groups required to reach theoretical saturation is between three and six and recommend four to 12 people as the appropriate size for a focus group discussion. This was borne in mind when devising the focus groups for this study.

The first two focus groups consisted of seven and 10 participants in Dublin and Waterford respectively, with ages ranging from 55 to 80 years. In Waterford they were recruited through Probus Ireland (an organisation comprised of clubs providing a social network for retirees) and in Dublin through professional employment networks. The third focus group was also conducted in Waterford and had 10 participants, who ranged in age from 30 to 80 years (70% of participants were over 55). Most of the elderly participants in this third focus group were re-invited from the first focus group. As the first two focus groups revealed that younger cohorts may not have the same housing equity in their old age as their current elderly counterparts, younger participants, who were in the minority, were invited to the third focus group to explore pre-retired perceptions on housing equity.

These focus groups[3] were conducted in 2016 and 2017. Most of the participants (see Appendix A) were retired homeowners with little or no outstanding mortgages; some also had private pensions. Each focus group lasted approximately two hours. The discussion guide was prepared in advance, as suggested by Al-Umaray et al. (2018), to ask theme-based questions of the participants. A discussion guide is a list of topics or more commonly a series of questions used by the moderator to guide the discussion (Hakim, 2012).

Participants were asked theme-based questions which were designed from the literature in advance as part of the focus group discussion guide. This also contained two cards/vignettes (see Appendix B) which invited participants to rank their sources of retirement income and mediums of withdrawing housing equity. These vignettes also helped in terms of answering the research objectives and facilitated further discussion from the focus group participants under the respective themes. The key insights provided from these vignettes are further elaborated on in the findings and analysis section below.

The participants were invited to sign a consent form before commencing the audio-visual recording of the discussion. Afterwards, transcripts were prepared from the audio-visual recordings to document participants’ experiences and opinions. The transcripts consisted of over 50,000 words in aggregate, which were analysed using NVivo qualitative data analysis software. As this study has pre-determined themes, it is suited to thematic analysis. The authors identified the following themes from the literature regarding home ownership, pensions and equity release:

-

attitudes toward home ownership;

-

housing equity as a source of retirement income;

-

ranking of the mediums of housing equity withdrawal;

-

role of the family and obligation to bequeath.

While the first two themes relate to the first research objective, the latter two themes relate to the second objective of this study.

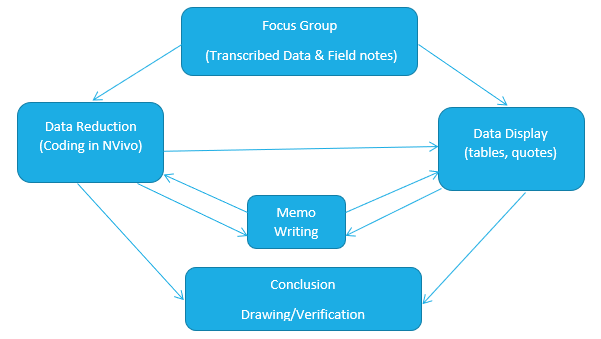

An analysis of the focus groups was conducted using a spiral model (Creswell, 2013), i.e. the process of moving in analytical circles rather than using a fixed linear approach. Miles and Huberman (1994) suggest that there are three components of qualitative data analysis: data reduction; data display; and conclusion drawing/verification. Within these cycles of analyses, the authors also addressed three components as illustrated in Figure 1, where the arrows represent the linkages between the activities of focus group analysis.

Miles and Huberman (1994) explain data reduction as a form of scrutiny that polishes, sorts, focuses, and organises data in such a way that the final conclusions can be drawn and verified. Krueger and Casey (2014) argue that a researcher constantly makes choices about what to register and what not to register, without necessarily being conscious of it. The lead author drew on the themes from the literature and reflected on the research objectives for data shrinkage. Coding is a popular technique for data reduction and NVivo helped to execute it effectively.

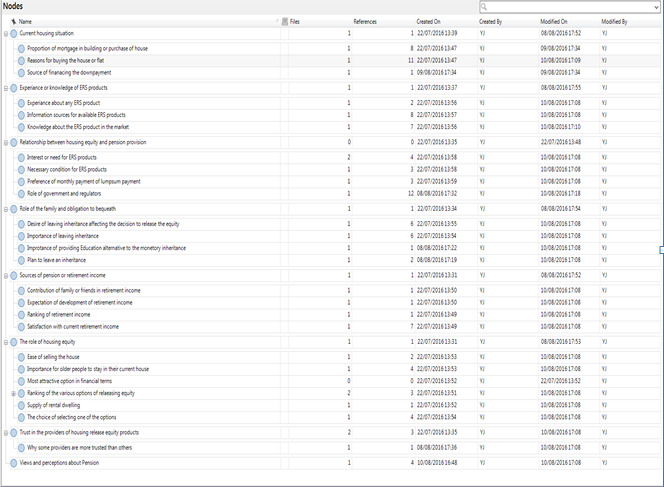

As suggested by Partington (2002), NVivo was utilised for creating nodes and particular data segments were categorised under each node. These nodes (see Appendix C) were then used for coding the themes and patterns emerging from empirical evidence regarding utilisation of housing equity wealth and other income sources in retirement. Hennink et al. (2010) use the term ‘code’ to refer to an issue, topic, idea, opinion, and so forth, that is evident in the data. The initial transcript reading helped to identify explicit codes, which were then refined later in the analysis, as recommended by Barbour and Kitzinger (1999).

Creating an initial list of codes helped the authors to link research objectives or conceptual ideas directly to the data. As suggested by Hennink et al. (2010), the authors made use of the deductive coding in this analysis as issues had already been identified from the literature. The architecture of nodes (see Appendix C) and sub-nodes created in NVivo helped in coding the transcripts and categorising the content into various nodes. Lastly, conclusion drawing/verification involved drawing meaning from the displayed data. This is presented in the discussion and conclusion sections below.

Findings and Analysis

The theme-based investigation was carried out on the transcripts of the focus groups. The findings from the key themes are presented below. Pseudonyms have been used when quoting focus group participants to protect individual confidentiality.

Attitudes toward Home Ownership

This theme explored the participants’ attitudes towards owning a home and their motivation behind the ownership of any other residential properties. When asked about the reasons for buying a dwelling in the past, one participant provided an historical context to home-ownership attitudes:

“I think looking at the history of land ownership in Ireland, it could probably be terribly deep into our roots and we own where we can. Bearing in mind, until the Land Acts [late 19th, early 20th century], we were tenants. In very many instances, in medium to small farms, you were almost tenant at will. I have no doubt that ownership is in our genes and will be in them for many generations. I have no doubt the insecurity of the tenure moved us to property ownership. Deep into our genes, ownership is important.”

(Tony, age < 65, Waterford FG1)

Another participant mentioned how he used tax exemption on interest payments to his advantage to buy multiple properties:

“But I found that the tax benefits that I got on my repayment on loans was very helpful and the tax situation was very favourable at a time to borrow. So, the whole thing worked out satisfactorily for me and the investments I made have proved well worthwhile at my age.”

(Shane, age unspecified, Dublin FG2)

However, nearly all participants recognised the awareness among the younger generations that they may never own their own home and thus may not have enough equity in retirement. The following comment illustrates this:

“For the people in Dublin, property is dear, the rents are dear before you even get to buy and still they have to expect to save tens of thousands for the deposit. And if they have their young families, there are just too many expenses immediately, that is putting home ownership out of reach altogether.”

(John, age 65–75, Waterford FG1)

This view was echoed by some elderly participants who referred to the lack of self-control (as postulated by the BLC hypothesis) and myopia exhibited by the younger generations in terms of not saving enough to accumulate the deposit to get on the property ladder. One participant also highlighted how difficult it is for the younger generations to borrow large sums of money to get onto the property ladder and not having enough equity in retirement to potentially use ERS schemes.

“The current generation has a bigger problem in terms borrowing €300,000 and €400,000 to buy the houses. Would they ever be in the same position to utilise equity in their house? There may not be equity.”

(Michael, age < 65, Dublin FG2)

A young participant from the third focus group referred to the changing attitudes towards home ownership among younger generations: “I think things are changing. I don’t think there is still the same kind of mentality of owning anymore” (Rita, age 30–40, Waterford FG3).

It is evident from the discussion under this theme that the meaning of home ownership and attitudes towards it have altered. While cultural reasons and fiscal support, such as tax relief on mortgage interest, have supported the existing elderly in owning their home, the elderly believe that ‘millennials’ (individuals born between 1981 and 1996) may not have the same opportunities or regard home ownership in a similar way.

Housing Equity as a Source of Retirement Income

Under this theme, we explored and explained existing sources of retirement income as discussed with the first and second focus groups with elderly participants. Further, the dialogue identified the role of housing equity as an existing source of retirement income. To determine this, a ranking card/vignette was designed, listing all the possible retirement income sources and participants were asked to rank income sources according to their importance or the highest proportion of income they would derive from those sources. Participants who were not yet retired were requested to rank these in terms of potential income sources. The participants were also asked whether they were satisfied with their income after retirement and whether they would want to release the equity from their home to supplement their post-retirement income. The results of this ranking exercise are shown in Table 1.

From the analysis, it was revealed that the majority of participants in both the focus groups rely on the occupational pension as their primary source of retirement income. The State Pension was ranked second in Waterford and third in Dublin, which shows a marginal disparity. In Dublin, housing assets (“house that you live in”) were ranked second, perhaps due to participants relying on their current homes (in the form of rent saving) to a significant extent as rental yields tend to be higher in the capital. In Waterford, this was the fifth most important source of retirement income, perhaps due to lower rental yields there. For the same reason, rental income from the other properties was ranked third in Dublin and sixth in Waterford.

Private pensions/insurance were ranked as the third and fifth most important sources of retirement income in Waterford and Dublin, respectively. The fourth rank was given to other assets by participants from both cities. Family support and social benefits were ranked last by both groups. This could be a function of the middle-income cohort, with whom these research interactions occurred, and might not be true for lower income groups.

When asked about their satisfaction with their current retirement income from existing sources as compared to pre-retirement income, those who were retired seemed content with their retirement income. However, many argued that it was not enough to have a good and active lifestyle. Many of them realise the importance of health and see money as of secondary importance. For example, a participant clearly expressed these views: “I would say generally if you have enough to live on and are comfortable, you are living well. But your health is your wealth” (Tom, age 65–75, Waterford FG1).

They were further asked whether they would release housing equity in order to supplement their income and to improve their lifestyle. Depending on their personal circumstances, many participants seemed open to the idea of using housing equity by any suitable medium to supplement their income. It can be interpreted from the focus group discussions that although participants are satisfied with the income received from existing retirement income sources, they are receptive to the idea of releasing equity from their home and improving their lifestyle, as can be surmised from the following comment:

“Well, I think if I was struggling to live comfortably, to have my holidays and things I wanted to do. If I couldn’t afford that, and if I am living in a house worth a million, I would say to myself what a fool I am you know. Hanging out in this lovely apartment to give it to my children. So, that’s why I certainly like the XY Company [an ERS provider in Ireland] idea.”

(Shane, age unspecified, Dublin FG2)

The findings in relation to this theme suggest that most focus group participants seem to be relying on traditional sources of retirement income such as the State Pension or occupational pensions as their primary sources of retirement income. This is followed by private pensions/insurance and other assets.[4] Overall, there appears to be a limited use of housing equity, except in the form of rent savings or imputed income in Dublin. In other words, there seems to be little use of the direct withdrawal of housing equity in the existing environment. There is also evidence of the mental accounting concept of the BLC hypothesis (Thaler, 1990) in that individuals would not contemplate consuming housing equity in the same way as liquid or financial assets. The findings suggest that some intervention from regulators and policy makers may be required to make the release of housing equity more attractive and feasible for retirees.

Ranking of the Mediums of Housing Equity Withdrawal

Under this theme we explored the ranking of different options of accessing equity or asset deployment with the first and second focus groups with the elderly participants. As ERS was one of the alternatives, a brief description and explanation of ERS products was presented to the participants. Participants were provided with a vignette listing different options of releasing equity from their homes. In this vignette, participants were presented with a hypothetical situation of a pensioner household having difficulties with finances. Subsequently, participants were asked to give advice to the household depicted in the vignette.

After the ranking exercise, the most attractive medium of releasing equity in financial terms was also probed. Furthermore, participants were asked about the importance of living in a residential community for elderly as some of these options would require changing their dwelling place. It was also explored whether it would be easy to sell or rent the home in the current environment when downsizing, or if sale-and-rent was a preferred option. The results of the responses to this vignette are presented in Table 2.

From Table 2, it is evident that there are some differences in participants’ views of releasing equity from their homes. These views might be affected by the price and size of houses in both cities. In the case of Waterford, downsizing is the most preferred option, followed by the use of ERS products. The Dublin participants prefer renting-a-room as a first choice due to the significant tax-free income that can be generated. This was followed by ERS and downsizing. For Waterford participants, downsizing may be preferred due to relatively bigger house sizes compared to those in Dublin. One participant summarised these options very eloquently:

“Now, looking at the options for me, I could rent a room in the house and I see [an] article about it in the paper. … If you rent a room, you can get a tax-free income of some significance. Or you borrow against the property and the interest is rolled up. You don’t have to pay anything. You have the money and you spend it. And you live there till you die. Taking your equity and turning it into a private pension or into a benefit to yourself. Then you know you could share your house with other people. But who wants to do that? But it’s there, isn’t it? That’s the possibility.”

(Dev, age 75+, Dublin FG2)

This view was corroborated by another participant who indicated a receptiveness towards housing equity withdrawal:

“Realistically what we all should realise [is that] the value of our house is often bigger than our pension. The house is often, maybe twice as big as your pension. So, it’s an asset that we will have to learn how to use.”

(Robert, age 65–75, Waterford FG1)

Various participants preferred different options based on their personal perceptions and circumstances, as well as the city they live in. For example, a participant in Dublin preferred to opt for downsizing rather than ERS, and a few participants nodded in agreement with him. In his words: “I think I’ll be more likely to sell and look for a smaller dwelling rather than trying to release equity” (Michael, age < 65, Dublin FG 2).

Most of the participants recognised that it is important for older people to stay in their community but not necessarily their current dwelling, which also suggests a preference for downsizing within the same community. As articulated by one of the participants:

“I think people might want to stay in the community basically, with familiar surroundings. Like, for instance, my children: they are probably not going to live in Waterford. If, God forbid, my wife dies, I will be on my own in a four-bedroom house. What do I want a four-bedroom house for? I will go down to John’s College [a voluntary housing association development for the elderly]. I will sell the house.”

(Tony, age < 65, Waterford FG1)

When asked about the availability of suitable dwellings, everyone accepted that there was a lack of sufficient supply. Among the Waterford participants, there was a sense of there being insufficient choice in attractive small residences suitable for the elderly; only one new development in the city (population 53,000) was singled out favourably in that regard. For example, one participant noted in agreement: “It is down to the supply of the right kind of accommodation, which is not there” (Rita, age 65–75, Waterford FG3). This suggests that there is a strong need for accommodation types of different sizes based on individuals’ needs in the same community.

When asked how easy it is to sell a home and buy a smaller one (downsizing), most participants agreed that it would not be easy to do so. For example, one participant expressed the following view:

“Somebody may have a house that theoretically may have had an enormous amount of [equity] – not anymore. But what you are buying has also dropped a lot. So, the scenario is not different [from the pre-financial crisis]. Like, there is not (much) money moving around.”

(Robert, age 65–75, Waterford FG1)

In essence, this suggests that homeowners can release comparatively less capital if trading down or using equity release. This may not be a problem when providing a replacement residence, though capital released for income has less value for that purpose, given that the cost of living has risen more than house prices.

However, a few participants disagreed with the view of downsizing and moving to a smaller residence as they would want to continue living in their current homes. As per the comment made by one participant: “Hugely important, yeah” [to live in your own home] (Dev, Age 75+, Dublin FG2). Some participants agreed and said it was very important to live both in their current home as well as its community. As noted by one of the participants:

“I wouldn’t live in an apartment. I think it is the key question that you don’t have to be uprooted from your environment. I could sell my house [for a] profit and get money and all kind of things, but I don’t want to move from where I am, like. My neighbours I like, the pub I like, the environment.”

(Shane, age unspecified, Dublin FG2)

Another participant specifically expressed her opinion in favour of re-introducing ERS products:

“If the European Community were to make funds available for the companies to be able to bring that scheme back, it would be a very workable practical way for all of us here. We wouldn’t have to sell our houses and we wouldn’t have to make repayments.”

(Kathy, age 65–75, Dublin FG 2)

Both of these comments, along with the comment made by Shane (Dublin FG2) regarding the ERS provider (see the section above on housing equity as a source of retirement income) imply that there is some latent demand for such products. Although participants collectively ranked ERS as a second choice in both the focus groups with elderly participants, they also expressed a view that the interest rates for such products were disproportionate. Nonetheless, participants from both focus groups indicated receptiveness to the idea of using ERS products.

From an analysis of the discussions, it appears that participants are favourably disposed towards employing ERS products as an option for releasing equity, as well the other two principal options of downsizing and renting a room, depending on their location and individual preferences. Moving residence can cause additional financial hardship and physical and emotional stress and the availability of a suitable dwelling is also a concern. Therefore, ERS emerges as a definite choice for those who want to stay in their community in their current homes.

The Role of Family and the Obligation to Bequeath

Participants’ views on leaving inheritances were also explored as it would further help in drawing a conclusion about their willingness to release equity from their dwelling. The primary researcher was particularly interested in probing participants’ view of the importance of bequests and their desire to leave them to their families.

Regarding the importance of leaving an inheritance, many participants noted that business assets (including farms) are more likely to be transferred before death to the next generation than personal assets. This represented an expression of an intergenerational trust: business assets are not for consumption but rather represent a livelihood for the next generation. The participant Noel’s two observations below show contingency and granularity with respect to the provision of legacies. He articulated the range of views reflected in the group on this topic.

“If you were a farmer, and you brought up a son or a daughter to farm, they would reasonably expect that the assets of the farm and the capital would come to them because anything else would not cover them and put them on the road. And the same for any family business, that if you are working on a family business and your family pass it all to you. It isn’t a little thing. It’s a vital thing.”

“I think it all looks at how the family is living. Say if you are a doctor or a teacher and that’s how you earn your living, and your children have different qualifications or the same, they don’t require a capital to make a living. They do not require the land or the machinery as some families do. So, it depends on the circumstances of the family.”

(Noel, age 75+, Waterford FG1)

Also, financial inheritance was not considered important. Instead, providing education to children was considered an important form of bequest. This was expressed by one of the participants: “They (the children) will get an education, the most valuable thing our parents can give us is education” (Michael, age < 65, Dublin FG2).

Most of the participants had a desire to leave something for family members or even carers/neighbours who helped them in retirement. When asked about their plans to leave an inheritance and how this affected their decision to release equity from their home, most nodded in agreement that leaving an inheritance does affect their equity release decision. For example, one participant stated that:

“I think most people don’t want to die penniless. You don’t want a situation … where the money runs out and you run out at the same time. In other words, you would like to think it’s a legacy type of idea.”

(Tony, age < 65, Waterford FG1)

However, for some participants, it was not important to leave an inheritance and they would only do so if they could afford to. As one participant expressed it:

“I wouldn’t consider it very important. It is very nice to leave something but at this stage it isn’t an important thing to do. I would love to be able to leave something for them and I hope so, but it isn’t an issue.”

(John, age 65–75, Waterford FG1)

It is evident from these comments that the participant’s views about leaving an inheritance and their interpretations of the meaning of ‘inheritance’ are quite broad. For most participants, business as opposed to personal assets are more likely to be transferred. Also, intangible assets such as providing education for children fits in with views of bequeathing wealth. The concept of an advance bequest was also strong: perhaps there is more satisfaction in making such a transfer now while alive rather than by bequest later when the recipient’s need perhaps may not be as great. While some do not feel the pressure of leaving something, there is an element of desire to provide some bequest, however modest. Thus, the precautionary motive might incline an individual to preserve some level of assets, both to support a quality of life and to leave a modest bequest. Also, the framing effects in relation to bequests were implied by a couple of participants. One participant demonstrated signs of sound personal financial management by showing a desire to leave something after they die. Another participant deemed education a substitute for a tangible bequest by valuing the provision of the means to make a living as opposed to money left after death.

Discussion

This paper offers evidence on empirical aspects of the views of elderly people in Ireland on the role of residential property in supplementing retirement income in order to address the research objectives.

Although it is evident that currently the State Pension and occupational pensions are the primary sources of retirement income, there seems to be a growing interest in releasing equity from residential property among the elderly in Ireland. Most prefer to stay in the community in which they currently reside and the idea of releasing equity from their housing assets is viewed favourably as a solution to providing or supplementing retirement income in the current economic environment once the location objective is satisfied. Crystallising a cost-effective product design that integrates the supplier and customer cash flows with wider fiscal, housing and social parameters, has so far eluded the market. Thus, retirees are constrained in pursuing a meaningful and realistic pathway to accessing the illiquid but no less valuable capital that they have accumulated in their homes.

The focus group findings are slightly different to the findings from other EU member states (Doling & Elsinga, 2013; Elsinga, 2011; Jones et al., 2012; O’Mahony & Overton, 2015) in which focus group participants seem less interested in releasing housing equity. However, as outlined earlier, nearly all of these cited studies have had a narrow definition of housing equity withdrawal in the sense that they consider only one medium (ERS) as a potential way of releasing housing equity. The differences in the findings are likely to be attributable to the lower net replacement rates for pensions and a less generous public healthcare system in Ireland.

Insofar as withdrawing housing equity is concerned, as discussed earlier, there are alternative mediums and using a financial product is just one among several. Of these, downsizing (trading down) and letting out part of a dwelling (rent-a-room) seem to be the most preferred choices in a small city (Waterford) and a large urban area (Dublin), respectively. Again, as pointed out by Dublin participants, this is due to the unavailability of suitable smaller dwellings within their current community. Also, in the Dublin focus group, using a financial product such as ERS was the second preferred choice while this (ERS) was the third choice for Waterford participants. Therefore, the choice of mediums largely depends on the location, social needs, and ease of access to the medium itself. Nonetheless, here also our findings are quite contradictory to those of previous studies (such as Doling & Elsinga, 2013; Naumanen & Ruonavaara, 2016; Rowlingson, 2006) which report an aversion among the elderly to using housing equity. Perhaps the 2016 introduction of a rent-a-room income tax relief in Ireland has had a bearing here, along with a resistance to housing mobility where choice is limited.

The bequest motive was probed to explore the elderly’s preferences for using housing equity and it emerged that most would prefer to have a better lifestyle in retirement as opposed to leaving a sizable inheritance. Similar results were obtained by Mulligan (2019) in terms of participants giving preference to maintaining their standard of living in retirement. Bequests were considered desirable but not important. This was clearly reflected in the definition of bequeathing. According to the participants, this consists of not just financial or property bequests but also the provision of opportunities for educational advancement to their children or grandchildren and the prospect of financially rewarding careers. This is in line with the studies of Rowlingson (2006) and Overton (2011) who find that the inheritance motive is less important in the UK, and it contrasts with the findings of other scholars (Jones et al., 2012; Toussaint, 2013) where participants believed inheritance to be quite important.

These findings also confirm that participants tend to exhibit an MPC (marginal propensity to consume) in line with the BLC (behavioural life-cycle) hypothesis (Shefrin & Thaler, 1988). The participants believe in consuming first from their existing liquid income and prefer to utilise accumulated assets (financial or physical) only if they were struggling to live comfortably. For example, in line with mental accounting behaviour, the participants signalled that they tend to refrain from consuming accumulated physical assets, such as housing equity, as opposed to liquid and financial assets. This is in contradiction to the original life-cycle hypothesis which implies that individuals smooth their consumption throughout their lives, irrespective of their pre- and post-retirement incomes.

Concluding Remarks and Policy Implications

This paper explores the perception of elderly people in Ireland regarding the use of equity in their homes as a potential source of retirement income. The meaning of home ownership and the salience attached to outright ownership may affect the decision to decumulate housing wealth. While some mediums of releasing housing equity (such as downsizing and sell-and-rent) may compromise ownership in later life, some modes (such as ERS or rent-a-room) may allow elderly homeowners to retain some of the emotional and psychological attachments to their residences. Therefore, individuals’ perceptions and preferences for these mediums also matter, apart from the decision to use one of these mediums for releasing equity from the home. Where you live, your legal title to your property, its milieu, and who else lives there, is a blended scenario which can alter as your life circumstances evolve.

From the discussion in the previous section, there seems to be some surprising and idiosyncratic results emerging that may have some policy implications. First, the meaning of and attitudes towards home ownership in Ireland seem to have changed and a certain amount of detachment towards housing assets is evident. Although participants seem comfortable with the modest State Pension and in some cases occupational or private pensions, they also seem receptive to utilising housing equity to elevate their living standards or at least partially maintain a lifestyle in retirement. Furthermore, BLC factors such as mental accounting and framing (Shefrin & Thaler, 1988; Thaler, 1990) are fairly ingrained in the behaviours of some participants as explained in the analysis section, while there is not much evidence of the third BLC factor, self-control, in the data. However, the limited nature of this exploratory study supports the need for further empirical research.

Furthermore, the opportunity for and choice of mediums for withdrawing housing equity may differ between the different parts of the country, influenced by factors such as the availability of alternative suitable accommodation and the capacity for renting a room for a limited period, e.g. to a student or mobile young worker. The other interesting finding that emerged from this study are elderly people’s attitudes towards the bequest motive, which is certainly distinctive compared to most existing research.

Considering these findings, it may be opportune for the State to consider establishing a policy framework which provides elderly homeowners with the opportunity to utilise the equity reposing in their housing assets. To make this feasible, government agencies, together with private and not-for-profit stakeholders, would need to collaborate to design a framework with risk-proofed mechanisms that is plausible and safe for homeowners. Furthermore, a wider variety of suitable retirement housing would need to be made available in the proximity of the existing communities of elderly people. This could also involve designating housing equity as a fourth pillar in the pensions framework in accordance with the World Bank pillar system. Some initial steps have been taken with respect to social care through what is referred to as the Fair Deal Scheme (Age Action Ireland, 2019). Furthermore, such policy development could also help mitigate a change in the pension expenditure to GDP ratio, as would occur if public and/or non-contributory pensions were not maintained at current levels.

Some caution is necessary due to the limited number of participants involved in the focus group interviews. Furthermore, the focus group data only covered participants from two urban centres in Ireland and findings could differ for rural populations and smaller settlements nationally. The decision to use ERS may be influenced by both contextual (State Pension system, fiscal aspects, culture, role of the family, housing market situation) and individual factors (gender, life expectancy, the level of supplementary pension obtained at retirement, spending patterns, family size, health aspects, number of inheritors).

This research opens a door to examining the nexus between housing assets and retirement income in Ireland. It contributes to the consideration of this complex connection, which involves decades of financial, social, fiscal, and legal phenomena. Therefore, further research would need to be undertaken nationwide across genders, socioeconomic cohorts, and regions to develop concrete policy proposals worthy of implementation.