1. Introduction

Local governments in Ireland, typically constituted as county or city councils, have long been responsible for the provision of essential services such as roads, water, sewage, and social housing (Bertz et al., 2024). From an accounting history perspective, Quinn and Bertz (2024) provide one of the few studies in this area through their examination of accounting for waste management in 1880s Cork city. They demonstrate that the Public Health (Ireland) Act of 1878 acted as an important impetus for Irish local authorities to improve a wide range of public services, with associated developments in accounting practices. In their study, the extension of waste removal services to every household represented a direct response to the Public Health Act, just as the provision of clean water was fundamental to improving public health and sanitation. While contemporary literature has examined accounting for water (see Jollands & Quinn, 2017 for an Irish case), Jack and Napier highlight that “opportunities exist for fully historical studies of how water was or often was not accounted for in the past” (2023, p. 540).

This study responds to these calls by investigating accounting for water supply in Belfast city between 1840 and 1890. Belfast, the largest city in what is now Northern Ireland, and the leading industrial city on the island of Ireland during this period, represents an important yet under-examined context within accounting history research. More specifically, the study analyses the accounts produced by the Belfast Water Commissioners (BWC) with two objectives: first, to document their content and trace changes in these accounts over time and second, to offer explanations for observed patterns of change and stability, drawing on concepts from institutional theory. To address the latter objective, the analysis draws on concepts from institutional theory, particularly Scott’s (2014) three pillars of institutions and organisational routines, i.e. routines (e.g. Quinn & Jackson, 2014).

The remainder of the paper is organised as follows. The next section reviews the relevant literature, after which the study context and research methods are outlined. The findings are subsequently presented, followed by a discussion and concluding remarks.

2. Literature Review

A literature review covering three themes is presented here. First, accounting history in an Irish context; second, accounting and accountability in local government and related public service bodies; and third, accounting for water in both historical and contemporary literature. Together, these literatures highlight the limited attention given to water-related accounting in 19th-century Ireland and illuminate the need for further historical investigation.

2.1 Accounting History in an Irish Context

Accounting history research has covered many time periods and a range of organisational settings but remains relatively modest compared with other international contexts. While the 19th century accounts for a considerable share of global accounting history research (Fowler & Keeper, 2016), Irish-focused studies often concentrate on specific organisations, sectors or professional developments. A stream of research, particularly that based on the archives of the Guinness brewery, explores change and continuity in accounting practices over extended periods. Quinn (2014) and Quinn and Jackson (2014), for example, analysed accounting routines and rules within Guinness to show how practices became embedded or altered in response to external events. Moreno et al. (2019) and Moreno and Quinn (2020) similarly traced the evolution of reporting practices using content analysis and, in the latter case, institutional concepts to interpret observed changes.

Other strands of Irish accounting history address the development of the accounting profession (Annisette & O’Regan, 2007; Clarke, 2005; Murphy & Quinn, 2018; O’Regan, 2008, 2013), the teaching of bookkeeping (Clarke, 2008), and public service decision making (Quinn & Bertz, 2024). These studies demonstrate the value of archival approaches for understanding how accounting practices evolve within specific institutional, organisational, and social contexts. However, they also highlight that there is very little historical accounting research relating to organisations in what is now Northern Ireland, despite its distinctive industrial and economic development (Donaldson, 2017;[1] Hepburn, 1983; Johnson, 2016). This paucity in the literature reinforces the need to examine accounting in Belfast’s public service bodies during the 19th century. Next, we will examine local government accounting history and accounting for water.

2.2 Local Government Accounting History and Quasi-public Organisations

Local authorities in Ireland and Britain historically bore responsibility for essential public services such as water, waste, and sanitation. Yet, accounting history research on municipal or quasi-municipal bodies remains limited. Sargiacomo and Gomes (2011), in a review of local government accounting history, identified four research clusters: the adoption of accounting practices; municipal corporations’ reporting; central-local relations; and accountability in community organisations. Despite these clusters, they noted a dominance of private-sector studies and limited attention to public utilities or infrastructural services.

The BWC, the focus of this study, was not a municipal authority, but a quasi-public organisation: a statutory body responsible for delivering a public service typically associated with local government, i.e. water supply, while operating independently of Belfast Corporation. Such bodies shared many features with municipal corporations, including statutory accountability, authority to levy rates, and responsibility for major capital works. As a result, the institutional, normative and regulatory forces shaping municipal accounting are directly relevant to understanding their financial reporting practices.

Accounting research on British local government also emphasises the influence of 19th-century legislation on accounting development. Coombs and Edwards (1995), for example, documented how municipal responsibilities for public health, water, gas, and sanitation expanded substantially after the 1830s, prompting innovations in reporting practices. They identified five key innovations during the period of their study, namely (1) accruals accounting, (2) accruals-based balance sheets, (3) capital/revenue distinction, (4) the double account system, and (5) aggregate balance sheets. They also concluded that accounting change in municipal corporations was supply-driven, shaped by internal officers, councillors and professional accountants, rather than market forces or public pressure. Although their investigation focused on English and Welsh cities, these developments have clear parallels in Ireland, where public health and sanitation legislation (most notably the Public Health (Ireland) Act 1878) also reshaped responsibilities for water and waste (Quinn & Bertz, 2024). Taken together, this literature shows that the accounting of public service providers is historically under-examined, particularly outside the main British municipal centres and especially in the Irish context.

2.3 Accounting for Water: Contemporary and Historical Perspectives

Research on accounting for water has grown substantially in recent decades, especially in relation to environmental sustainability, governance, and measurement. Contemporary work demonstrates how accounting techniques shape water management decisions and organisational accountability (Godfrey & Chalmers, 2012; Passetti & Rinaldi, 2020; Tello et al., 2016). Irish studies, for example Jollands and Quinn (2017) and Bresnihan (2016), on Irish Water highlighted the governance and political dimensions of water accounting within modern public utilities. In contrast, historical studies of water-related accounting remain scarce. Where historical research does exist, it often focuses on broader themes such as water use (e.g. Anderson, 2016; Chappells et al., 2011) or resource exploitation (Giorgino & Barnabè, 2024). Jack and Napier (2023, p. 540) explicitly noted the absence of detailed historical examinations of accounting for water infrastructure and call for research into how water “was or often was not accounted for” in earlier periods. Giorgino and Barnabè (2024) provided a rare example, exploring medieval Siena’s water accounting through charge-and-discharge records, but their context is not comparable to 19th-century Ireland.

Thus, despite the centrality of water to public health, urban growth and infrastructure in 19th-century cities, there remains no accounting history study examining water supply accounting in 19th-century Ireland or, more broadly, in quasi-public municipal-style water bodies. This absence constitutes a significant gap in both Irish accounting history and the historical study of public service accounting.

3. Theoretical Framework

This study adopts an institutionalist history approach (Rowlinson & Hassard, 2013), following recent work by Quinn and Moreno (2024) that demonstrated the value of applying contemporary institutional theory to interpret accounting practices in historical contexts. Institutional theory is particularly appropriate for long-run studies of governmental or quasi-public bodies, where accounting practices may develop incrementally and become embedded over time. In this case, the approach is used to interpret the accounting practices reflected in the surviving financial statements of the BWC and to consider the extent to which these practices became institutionalised.

Institutional theory conceptualises institutions as comprising regulative, normative and cultural-cognitive elements which, together with associated activities and resources, stabilise organisational behaviour and give meaning to social practices (Scott, 2014, p. 56). These elements (see Table 1) provide a lens through which changes and/or continuities in accounting practices can be interpreted. The regulative pillar concerns the influence of statutory or coercive forces such as local Acts, mandated reporting requirements, or oversight by governmental authorities. The normative pillar captures expectations arising from professional, social or administrative values, including those shaped by the accounting profession and public-sector conventions. These two pillars broadly align with the coercive and normative forms of isomorphism described by DiMaggio and Powell (1983), which help explain how organisations conform to external expectations in pursuit of legitimacy (Suchman, 1995). The cultural-cognitive pillar refers to the shared understandings, classifications and taken-for-granted assumptions that underpin organisational action. As Scott explained, “internal interpretive processes are shaped by external cultural frameworks” (2014, p. 67), meaning that the way organisational actors categorise information or structure accounts reflects their underlying assumptions about what is appropriate, recognisable, or meaningful. Such cognitive templates can be observed historically within a single organisation through the stability of accounting categories and the persistence of reporting formats in statement layouts. Archives frequently preserve these interpretive structures, making cultural-cognitive analysis feasible even without cross-organisational comparison.

To complement the three-pillar framework, this study also draws on the concept of organisational routines, understood as recurrent, recognisable patterns of action that become embedded through repetition. Quinn (2014) demonstrated how routines can both reflect and reinforce institutionalised practices over time. More broadly, Burns and Scapens (2000) offered a foundational institutional perspective on accounting change, arguing that accounting rules and routines become institutionalised through their repeated enactment, yet may also evolve as institutional pressures shift. Their framework highlights the dual nature of accounting practices: they are shaped by existing institutional structures while simultaneously shaping future organisational behaviour. This perspective is particularly relevant for examining the BWC’s accounts, where routine preparation of annual financial statements over several decades provides an opportunity to observe patterns of stability and change in practice. Building on this, Scapens (2006) emphasised that management accounting change must be understood within its institutional context, as practices often persist due to their taken-for-granted nature rather than their technical superiority. These insights complement Burns and Scapens’ (2000) model and are particularly relevant for the present study, where the persistence or alteration of the Commissioners’ accounting formats may reflect deeper institutional dynamics rather than purely technical considerations.

The institutional framework therefore provides a structured means of interpreting changes and continuities in the BWC’s accounts. Regulative influences may be reflected in statutory requirements or directives shaping the content of the statements; normative influences in the adoption of professional or sectoral reporting conventions; and cultural-cognitive influences in the stable categorisations and taken-for-granted structures embedded in the statements over time. When considered alongside evidence of recurrent accounting routines, these elements offer insight into whether and how the Commissioners’ accounting practices became institutionalised over the period examined.

4. Context and Method

4.1 Context

Some general history information is useful to set the context for this study. The text In search of water – A history of the Belfast water supply by Loudan (1940) is particularly useful. This text was written to mark the centenary of the BWC.

According to Loudan (1940), the first piped water supply to Belfast dates from 1678, following appeals to the city corporation by two prominent citizens, George McCartney and Capt. Robert Leathes. By 1790, Loudan (1940, p. 15) noted that the supply was “ill suppled”, and by 1795 the Poorhouse authorities controlled the city’s water supply. The Poorhouse was a charitable society, known as the Belfast Charitable Society, and as noted by Loudan (1940, p. 22), its interest in improving water supplies would contribute directly to improving the general health of citizens. By 1800, “every owner or occupier of a dwelling-house in the town, who wished to have the benefit of pipe water to pay the Charitable Society an annual rent” (Loudan, 1940, pp. 32–33). However, in the early 1800s, the quality of water supplied by pipe was poor, resulting in unpaid rates. This, coupled with costs of expanding the pipe network to southern parts of the city, such as Stranmillis and Malone, left the Charitable Society with financial strains. By 1826, Loudan noted, “it was admitted that all attempts to adequately supply Belfast with water had failed” (1940, p. 36). Loudan reported that the question of forming a joint stock company to replace the Charitable Society was raised, leading to a debate about whether control of a water supply should be in the hands of a private company. As Loudan noted, “that was the position at the end of the year 1839. The town was as badly off as it ever had been, and there was almost unanimous desire for change” (1940, p. 38).

Change came in the guise of the Belfast Water Act 1840. This Act took control of any water supply undertakings from the Charitable Society, handing over control to the BWC, not to the city corporation. Crossman noted that in the year 1840 “[in] Dublin and Belfast, the corporations were found to be wholly inadequate” (1994, p. 77). In recognition of the Charitable Society’s earlier efforts, the Act granted it free water, an annuity of £800 and £5,000 towards clearing its debts. The 1840 Act also gave the BWC wide and varied powers, some of which are worth highlighting. It gave the BWC corporate status and powers to execute the provisions of the Act. Its responsibilities included constructing, maintaining and improving waterworks, as well as acquiring the land and water rights needed to ensure a consistent and adequate supply to Belfast.

The 1840 Act included financial provisions, including the ability to borrow money and levy water rates – with limits on rates to be charged to different types of properties. Certain properties, such as places of worship and public charities, were to be exempt from water rates and provisions were to be made for supplying water to the poor free of charge. From an accounting perspective, the 1840 Act required the BWC to appoint a treasurer, keep books of account and submit accounts every three years. Specifically, Section LXXXVI of the Act stated, “the said Commissioners shall submit the general Statement of Accounts for the previous Three Years, duly audited by the Auditors appointed as herein-after mentioned, with any Report the said Auditors may make thereon” – see Table 2. As will be shown later, the accounts were prepared annually from 1866.

During the period of this study, the BWC did not undertake major infrastructure projects. Large-scale works did not occur until the 1920s, culminating in the construction of the Silent Valley reservoir, completed in 1933 at a cost of approximately £1,350,000 (Loudan, 1940, p. 131), equivalent to about £77 million in 2025 values. Archival records provide data on expenditures from 1875, summarised in Table 3. As shown there, spending in the years 1875–1890 was comparatively modest and largely related to routine operational maintenance rather than major capital works.

4.2. Data Sources and Method

Data was sourced from the Public Records Office of Northern Ireland (PRONI). The records consulted at PRONI contain the financial statements of the BWC. From 1840 to 1865, the financial statements are handwritten and produced triennially. From November 1 1865 the financial statements are annual and printed. All financial statements from 1840 to 1890 were digitised on site by the researchers and stored electronically for offsite analysis. The year 1840 is the first year of analysis given it was the founding year of the BWC, as mentioned in the previous section. The year 1890 is the final year for two reasons. First, and simply, an analysis of 50 years of data is an ample time to observe stability and/or change in the financial statements. Second, and more importantly, the year 1890 is 12 years after the Public Health (Ireland) Act 1878, implying the financial statements may be reflective of efforts of an Irish city to take actions on sewage, water, waste, and other items around public health. Such actions could increase costs and prompt accounting change. In addition to the records at PRONI, legislation relevant to the BWC was examined as required. During the period of analysis, six Acts of parliament were passed – the Belfast Water Acts of 1840, 1865, 1874, 1879, 1884, and 1889.

Limited prior research on water and accounting from a historical perspective puts the present study as one of a few which may, over time, contribute a more complete theoretical understanding of how and why local governments/quasi-public organisations accounted for water in a particular way. That is, this study on its own contributes incrementally to understanding how local governments/quasi-public organisations accounted for their water supplies (see Jollands & Quinn (2017) for an example of accounting for water in a non-monetary sense).

5. Findings

The 1840 Act established the BWC as a corporate body and the Act provided that the BWC would consist of Commissioners elected by qualified ratepayers, who effectively were property owners/occupiers paying water rates, on a rotating basis. The Commissioners were given broad powers to construct, maintain and improve waterworks which would be managed through a governance and financial framework laid out in the 1840 Act. It required the Commissioners to appoint key officers such as the treasurer, clerk, collector, applotters, and an engineer to manage operations. Strict separation of duties was enforced, and the Act prohibited the same person from holding both the clerk and treasurer posts or from one acting as deputy for the other, to prevent conflicts of interest.

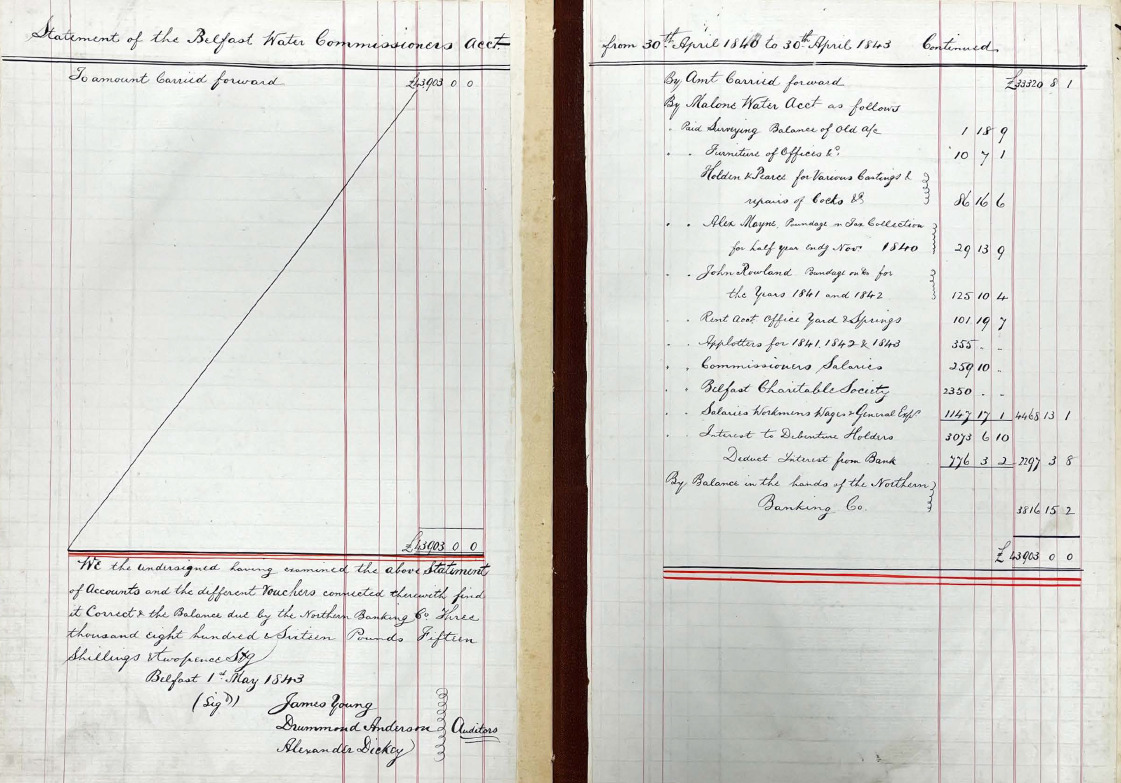

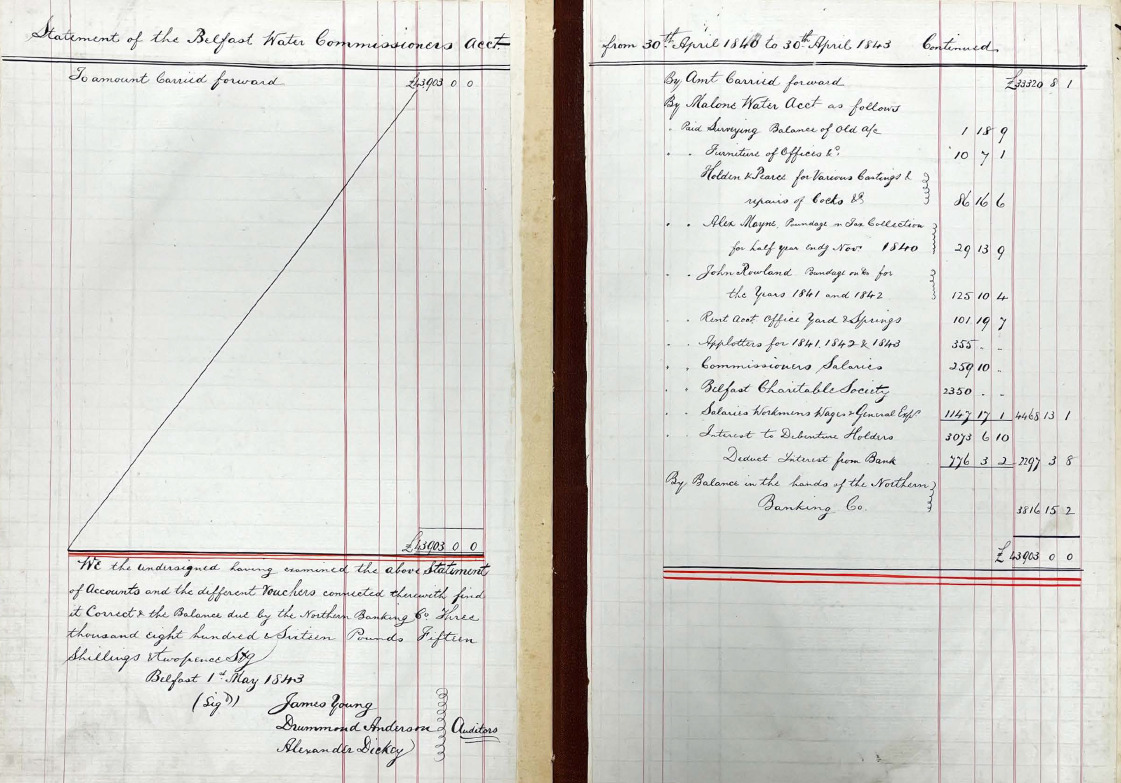

From the outset, the Commissioners were empowered and obliged to keep full and true accounts of all monies received and disbursed for water services – see Table 2. The Act specifically required that they, either through a clerk or themselves, record every contract, receipt, payment, and order, in a book provided for that purpose. These books of account had to detail all revenue (i.e. rates, rents, etc.) and expenditures, including maintenance costs, officer salaries, interest on debts, and any other water expenses. Figure 1 shows an extract of the 1843 handwritten accounts in black ink.

Every appointed officer (e.g. treasurer, collector) was required to provide accounts and deliver vouchers to the Commissioners when requested. They had to account for all matters under their remit along with all money received and paid out. Any officer refusing to produce receipts, account balances, or hand over books within 10 days of being required would face legal action by the Commissioners to recover the books or funds. In effect, the BWC’s founding legislation embedded fundamental principles of financial control and accountability, through segregation of financial responsibilities and documentation of all transactions, to safeguard the public funds under the Commissioners’ stewardship.

The 1840 Act provided multiple funding mechanisms for the undertaking of water supply. The BWC was authorised to raise revenue through water rates (a form of local tax on properties) and water rents or charges for water usage. The Act also empowered the Commissioners to enter special agreements for water supply to large consumers. For capital investment (see Table 3), the Commissioners could borrow money secured on the water rates and assets of the waterworks. They were empowered to mortgage the income of the undertaking or even to sell annuities charged on future water revenues to raise lump-sum funds for construction projects. All such mortgages or annuities had to be executed under the Commissioners’ common seal. The Act required prudent financial management, that is, after covering operating costs, interest, and the £800 annuity to the Charitable Society, the Commissioners were to apply a surplus to a sinking fund of at least 1% per annum on the borrowed principal to gradually pay down debt. This suggests that fiscal discipline was being (or attempted at being) instilled.

Furthermore, the Act built in mechanisms for external oversight and public accountability of the BWC’s finances. It provided for the appointment of independent local auditors drawn from the ratepayers who were paying at least 20 shillings in water rates. Initially, the Commissioners themselves nominated three people as auditors, and thereafter, at the first general meeting of ratepayers, the qualifier ratepayers would then either confirm or appoint three auditors to serve for the next three-year term. Every three years, in May, a general meeting of the ratepayers was held to either reappoint or replace the auditors for the next term. These auditors had the right to inspect all the books, vouchers, and documents of the Commissioners. The Act set the Commissioners’ financial year to April 30 and as soon as possible after April 30 each year, the Commissioners were required to prepare the annual accounts in a prescribed form which was directed by the Commissioners or ratepayers. These annual accounts were then submitted to the auditors for examination. The auditors reviewed the accounts and produced a report of their findings, and the audited accounts were then presented to the ratepayers at their next general meeting. Figure 1 shows the three named ratepayer auditors.

Another key point to note was that a general meeting of ratepayers was mandated every third year (in May) where the Commissioners had to present a “general statement of accounts” for the previous three years, which were audited. In practice, this meant that while accounts might have been prepared annually, the formal public presentation and discussion of the accounts occurred on a triennial cycle. To facilitate informed scrutiny, the Act required the Commissioners to publish an abstract of the accounts in local newspapers at least six days before the triennial meeting. Notice of the meeting itself also had to be advertised in advance. At these general meetings, the assembled ratepayers would hear the audited accounts read out, review the auditors’ report and ask questions, which provided a public forum for holding the Commissioners accountable. The auditors’ term and rotation were arranged so that oversight was continuous, and the outgoing auditors were replaced or reappointed every three years at general meetings.

Additionally, the Act imposed internal controls on disbursements where no money could be drawn by the treasurer except under a written order sanctioned at a Commissioners’ meeting and signed by the meeting chairman. The treasurer’s receipt was the legal discharge for monies paid to the Commission. This ensured that all expenditures had formal approval and a paper trail – see Table 3. Any treasurer who paid out funds without proper order, or any officer who misused funds, was in breach of the Act (subject to penalties or legal action). Overall, the 1840 Act created a governance system with Commissioner oversight, independent auditing by elected ratepayer auditors and transparency to the public via published account summaries and public meetings. There was no direct government audit at this stage, but accountability was enforced through local democracy (ratepayer meetings) and the courts (the Commissioners could sue defaulting officers, and penalties could be recovered in court). This suggests a continual reliance on civic governance and ratepayer oversight rather than the professionalisation of accounting staff.

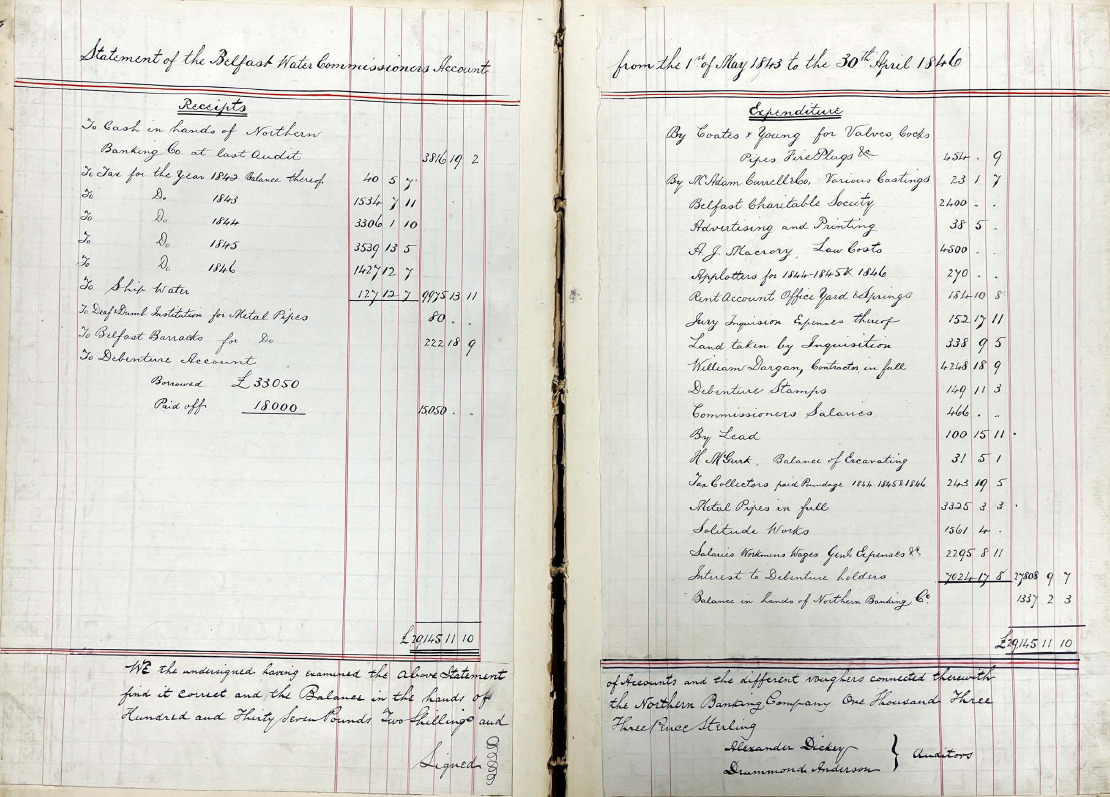

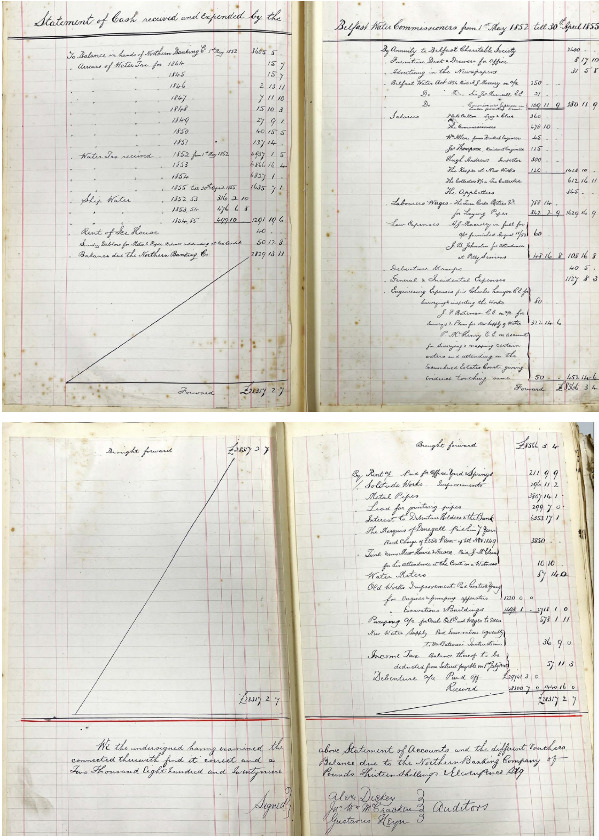

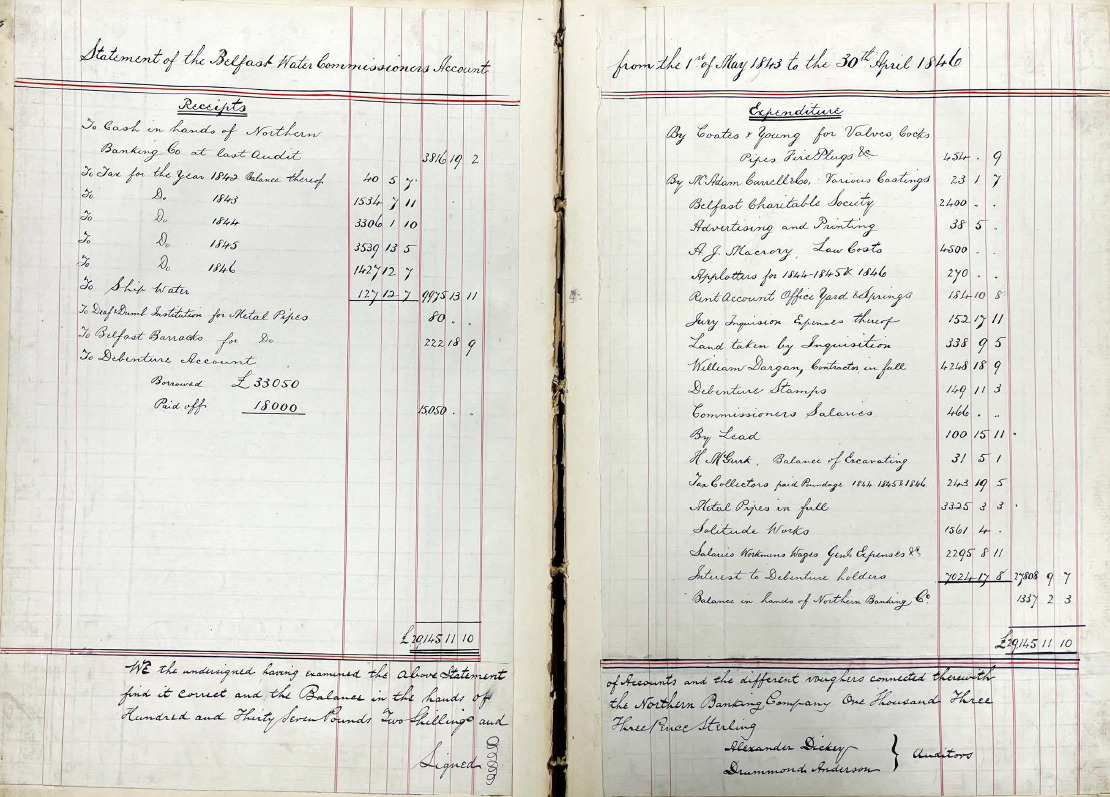

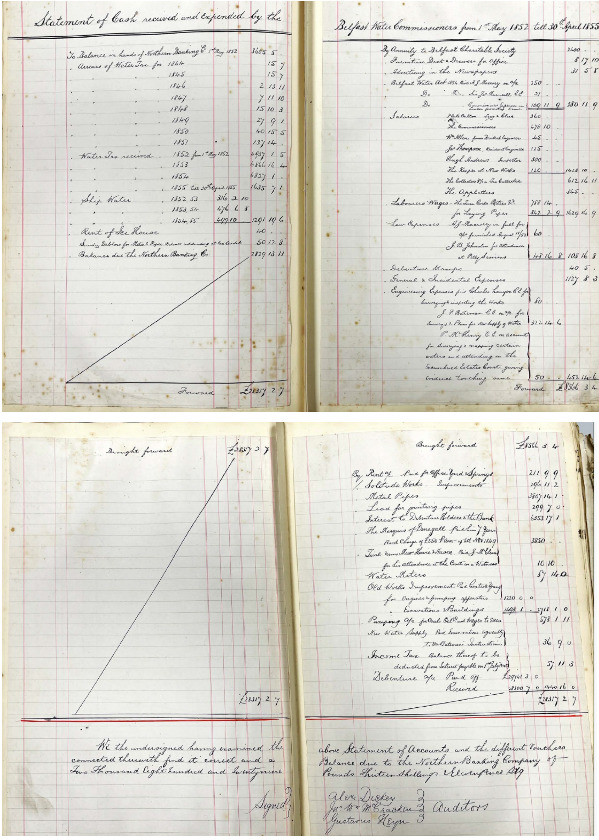

The next triennial set of accounts reflects some minor changes in layout, with “Receipts” and “Expenditure” now appearing as separate headers. Notably, in the accounts for 1849 and 1852, “Expenditure” was instead titled “Disbursements”. Such minor changes in wording did not alter the fundamental content but showed a degree of experimentation or lack of standardisation in format. Furthermore, in a few cases, for example for the years 1846, 1849 and 1852, only two auditors signed the accounts (see Figure 2). It is likely that changes in wider legislation, for example the adoption of the Waterworks Clauses Act 1847 in the United Kingdom (UK) which provided provisions for water companies and Commissioners, may have affected local practice, possibly allowing a quorum of two auditors. Additionally, the accounts became more elaborate, expanding from two to four pages (see Figure 3), suggesting that the volume and detail of transactions had increased as the water network expanded. However, the core content and layout only saw modest refinements, hinting at an early institutionalisation of the reporting routine under the Act’s requirements.

Change came in the mid-1860s driven by both the growth of Belfast and evolving legislation norms. The Belfast Water Act 1865 was enacted “for better supplying… Belfast and other places, and for altering and amending the constitution of the corporation of the Belfast Water Commissioners”. It reconstituted the BWC and expanded its jurisdiction beyond the town. The Act named a new set of Commissioners, including some of the existing ones and additional members, and continued them as “one body corporate” under the same name.

In practical terms, this Act likely broadened representation, for example incorporating areas outside the Borough of Belfast into the Commissioners’ jurisdiction. The statutory limits of water supply were defined to include Belfast and certain surrounding townlands in Antrim and Down. The key staff officers remained much the same, with a treasurer handling finances and a clerk keeping records. Effectively, the 1865 Act modernised governance but preserved the fundamental roles. The treasurer still received and paid out money on behalf of the Commissioners and the clerk still kept the official books.

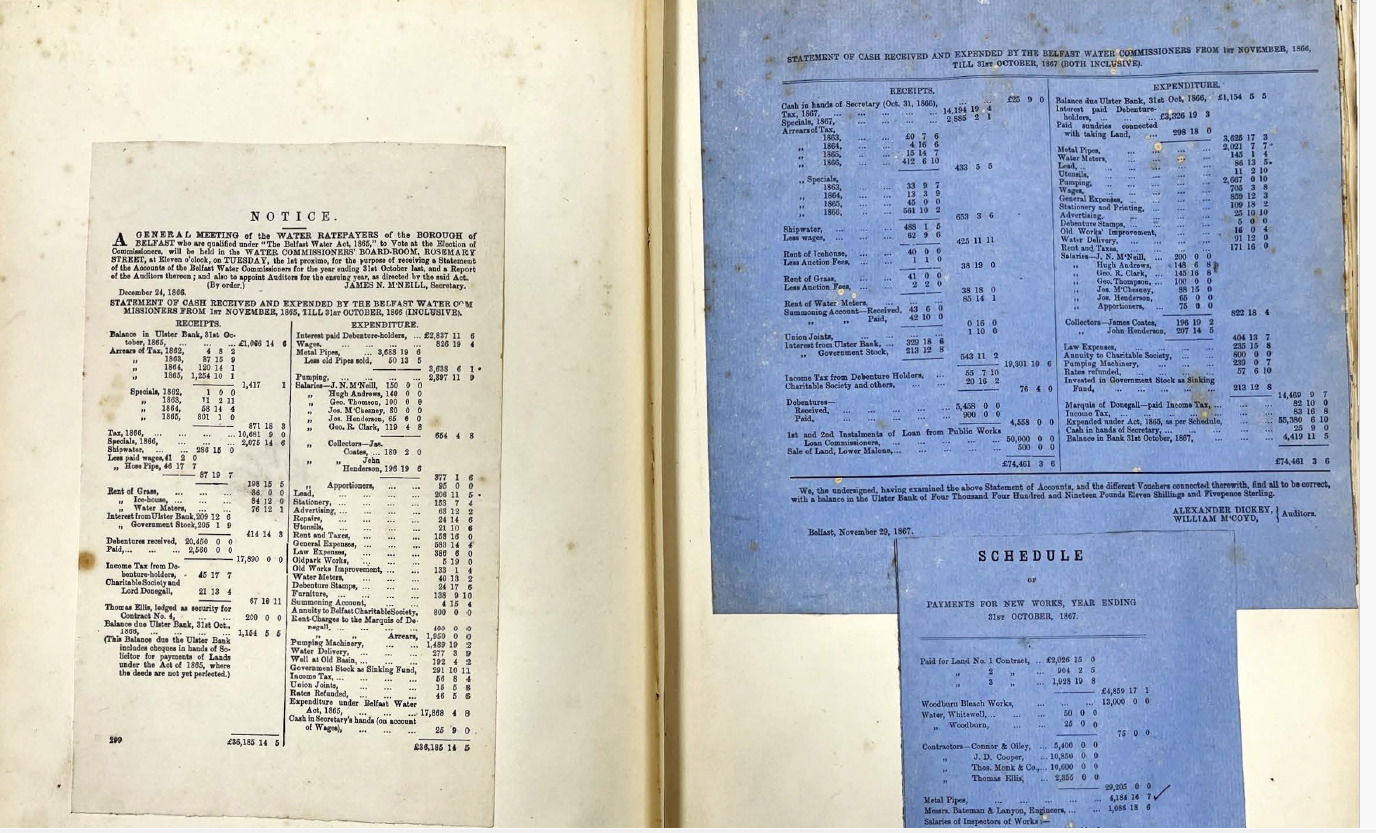

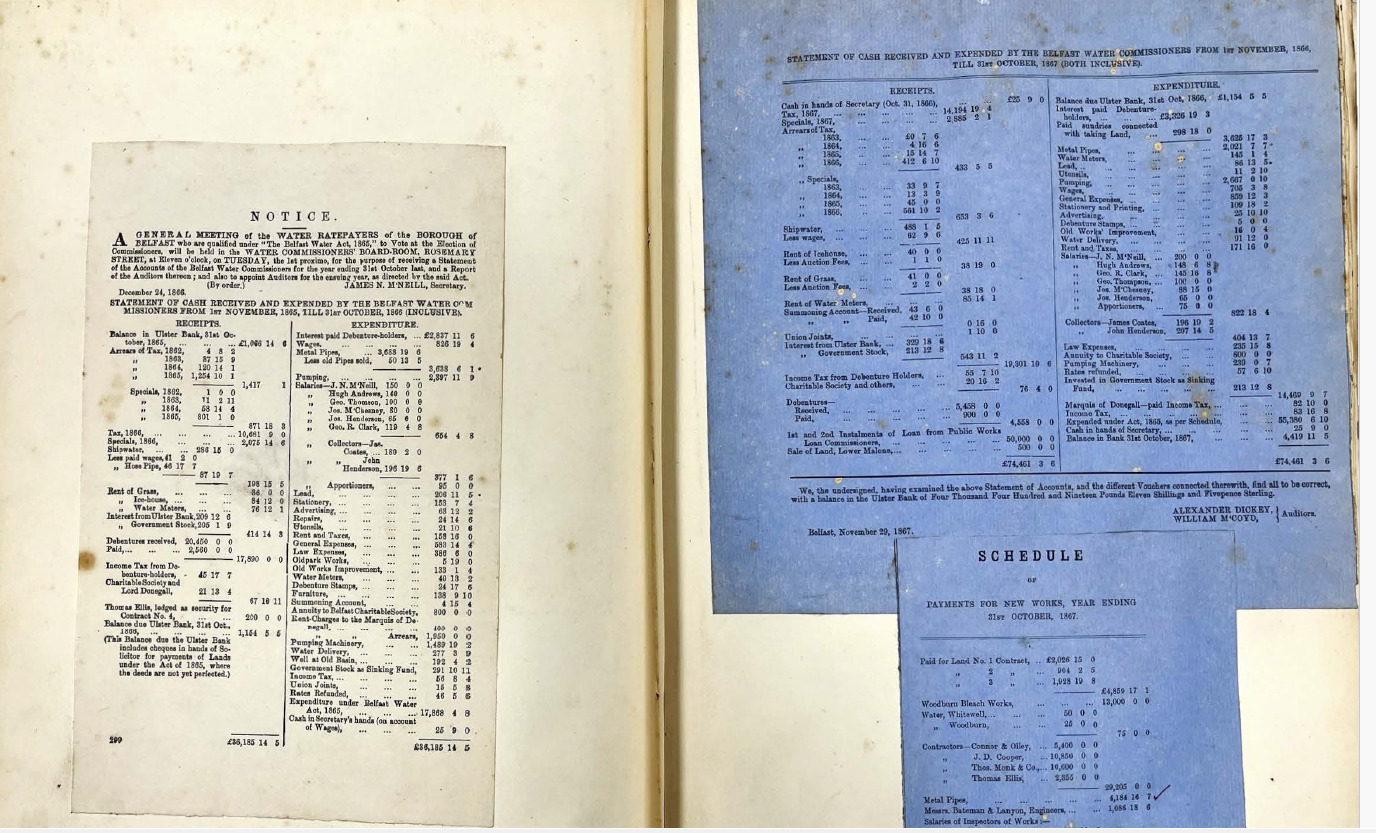

Under the 1865 Act, the Commissioners were still required to maintain accurate accounts of all financial transactions, that is, all income (water rates, rents, etc.) and all outgoings had to be entered into the books by the clerk or treasurer, but a noteworthy change was the move to annual reporting. The Commissioners also had to maintain records of any new loans or mortgages raised under the 1865 Act’s authority. Given the growth in the Belfast water supply, the volume of financial data increased. However, the accounting method, which was a record of receipts and payments, along with minute books for orders, remained fundamentally the same as in 1840. Another important change was in the account format moving from handwritten accounts to typed/printed accounts. The shift to typed accounts made the accounts more legible and somewhat more standardised – see Figure 4.

One other significant development in 1865, along with annual reporting, was the move to annual auditing. The practice of having three auditors for three-year terms was replaced with an annual audit. This was a key change as public accountability was no longer tied solely to a general meeting every third year but became an annual routine process. Furthermore, the 1865 Act called for two auditors, instead of three, to be elected annually by the ratepayers. Reducing auditors from three to two might suggest an effort to improve efficiency or indicate that securing three qualified auditors may have been challenging. As mentioned earlier, the accounts of 1846, 1849 and 1852 had only two auditors. Nevertheless, the Act still preserved the principle of multiple eyes on the accounts. The two auditors continued to “audit and examine the accounts” annually (1865 Act). The annual general meeting of ratepayers would typically hear the audited accounts and elect replacements for outgoing Commissioners, as well as, at times, the next auditors. In this arrangement, oversight may have occurred more regularly and could have become somewhat more attentive, although the extent of this is difficult to determine.

The Commissioners also remained subject to legal accountability and any misuse of funds or failure to account could be taken to the courts. In 1865, there is no indication of direct supervision by central government. Oversight appears still local through the auditors and ratepayers. However, by requiring the accounts to be open to public inspection the Act likely contributed to greater transparency. Thus, the 1865 Act maintained the independent audit and public scrutiny but increased its frequency (annual accounts instead of tri-yearly). We see that while regulative pressures forced certain changes (i.e. frequency of accounts, format, audit arrangements), it seems some aspects of accounting practice were institutionalised routines by then, that is, they continued doing things in the familiar way unless compelled otherwise. In essence, the 1865 Act introduced a degree of regulative oversight (i.e. more formal rules) and may have facilitated increased normative pressure from the public by establishing annual meetings at which the accounts could be discussed.

Subsequent legislation in the late 19th century appears to have influenced the BWC’s operations, though the available evidence suggests that these Acts tended more toward extending powers than fundamentally changing accounting procedures. The 1874 Act was titled “An Act to confer further powers on the BWC and for other purposes”. It did not overhaul the governance structure but rather extended the Commissioners’ powers, mainly to undertake new waterworks and secure additional funding. The corporate body remained the BWC, now operating under the constitution set by 1865. Thus, accounting and oversight provisions from the earlier Acts continued in force. The 1874 Act expressly operated in conjunction with the 1840 and 1865 Acts and it was supplemental. The Commissioners were still obliged to maintain accounts. The fundamental record-keeping methods of receipts and payments, vouchers for every expense and ledger entries remained unchanged – see Figure 5.

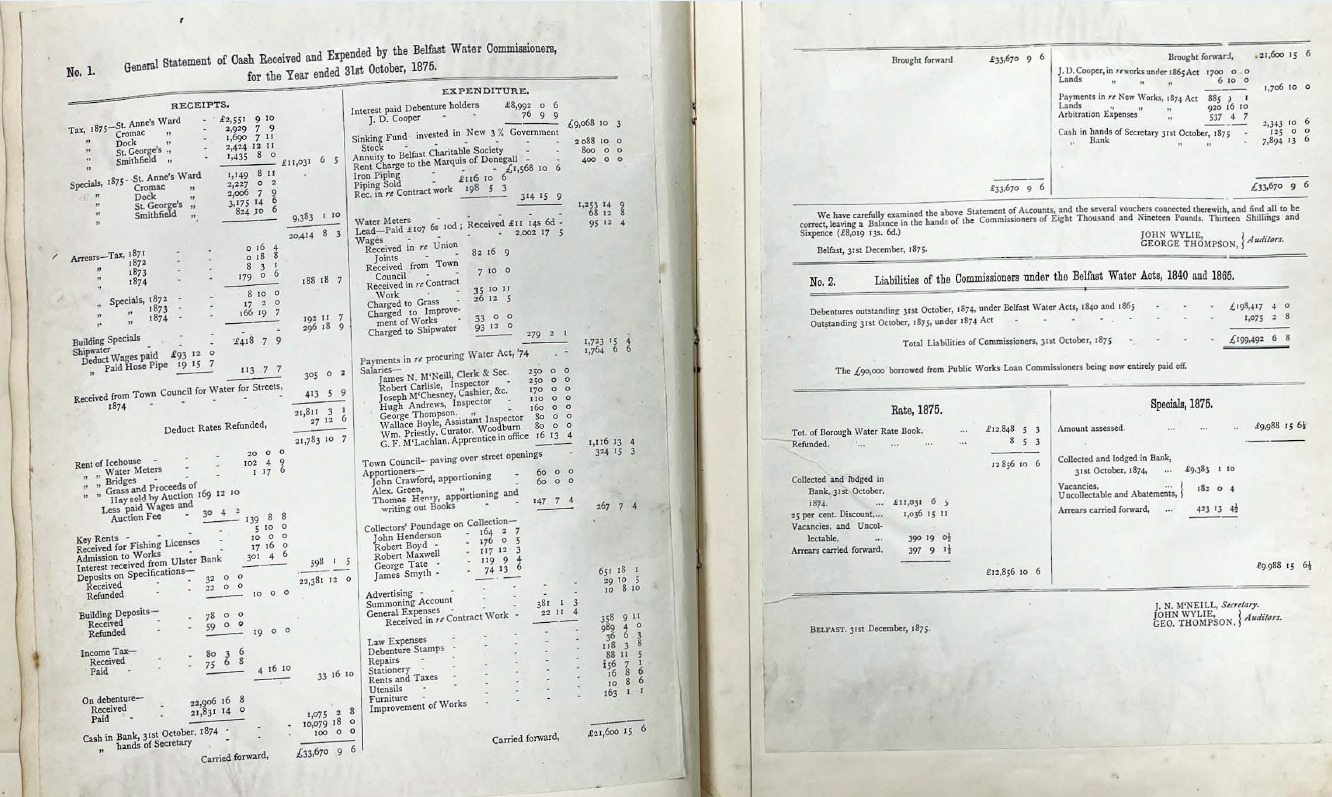

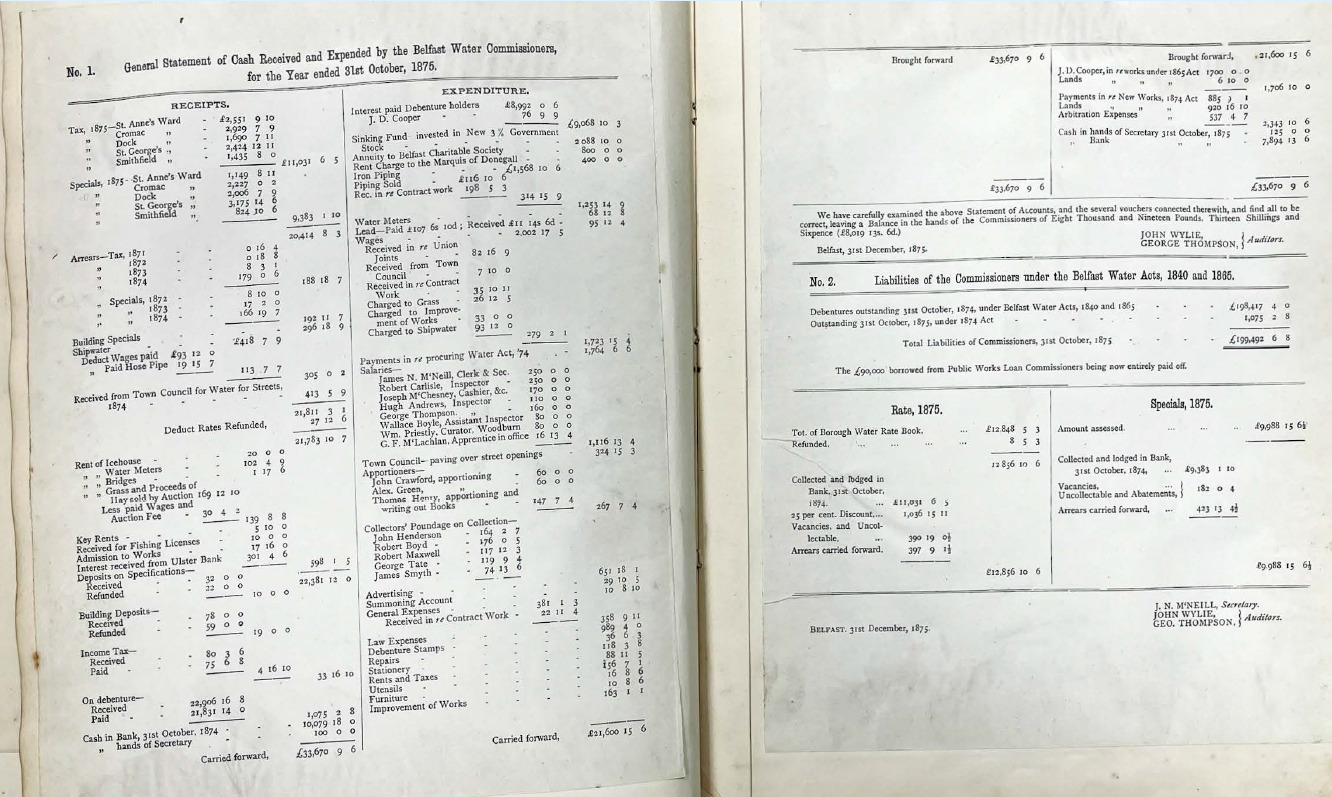

The 1875 typed accounts became more granular and were able to fit more line items on a page, allowing greater detail to be disclosed. This greater detail was likely driven by the complexity of a larger water supply system. We also see by the late 1870s the inclusion of a ‘Secretary’ signature on the accounts, suggesting that the BWC’s administrative staff grew and perhaps a formal secretariat was established.

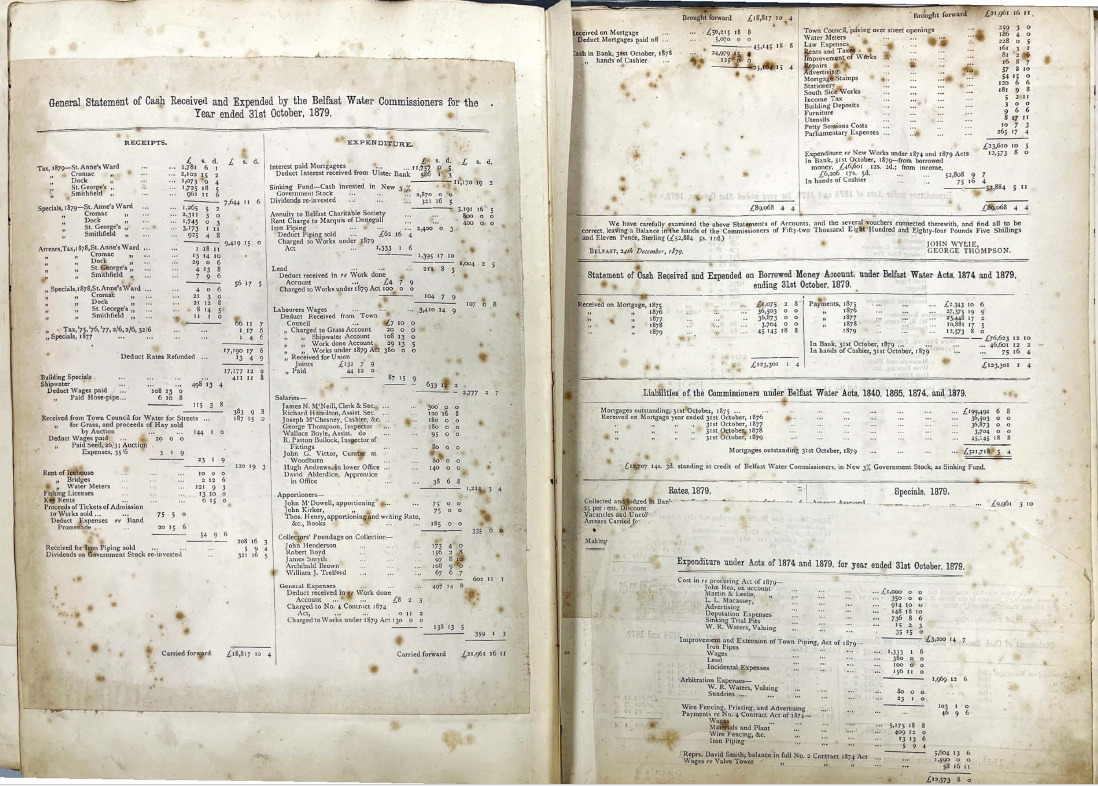

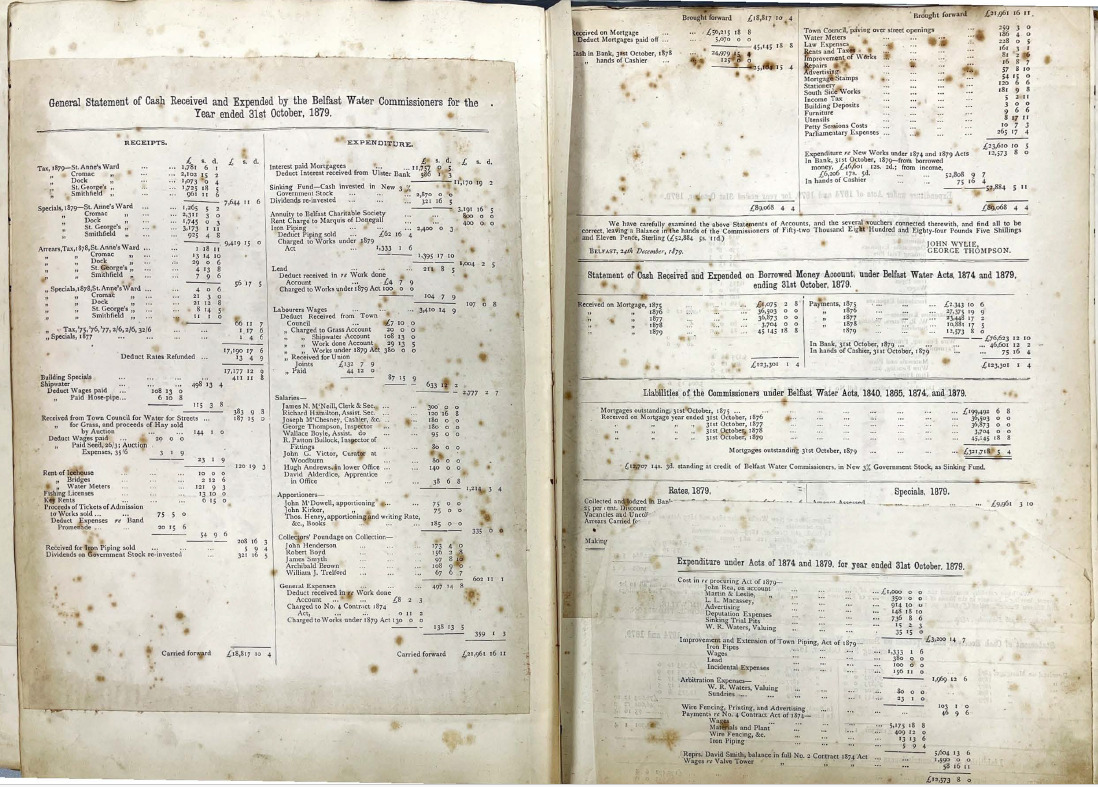

The 1879 Act’s main effect was to authorise new works and raise more capital. By 1879, the Commissioners were serving an even wider “district” around Belfast. All accounting requirements from earlier Acts still applied. The auditing and oversight regimen saw no major change. The accounts continued to be audited annually by the chosen auditors and presented to the ratepayers. If anything, by this period the Commissioners were publishing more detailed annual accounts – see Figure 6.

The 1879 Act did not add external auditors or require oversight by a central body. Thus, public accountability appeared to remain local through published notices, meetings, and the availability of audited accounts. Essentially, the 1879 Act continued the established institutional structure of Commissioners (as financial stewards), treasurer/clerk (as record-keepers), water rates and loans (as funding), and an annual independent audit (as accountability).

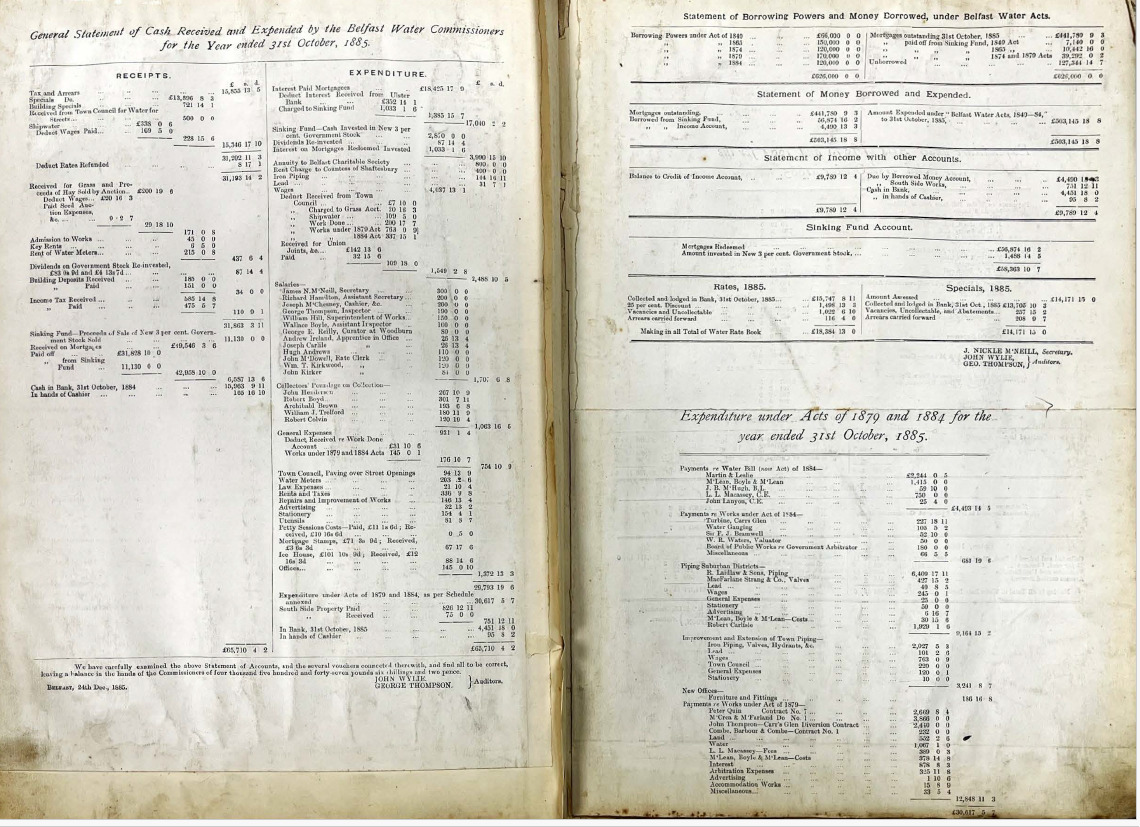

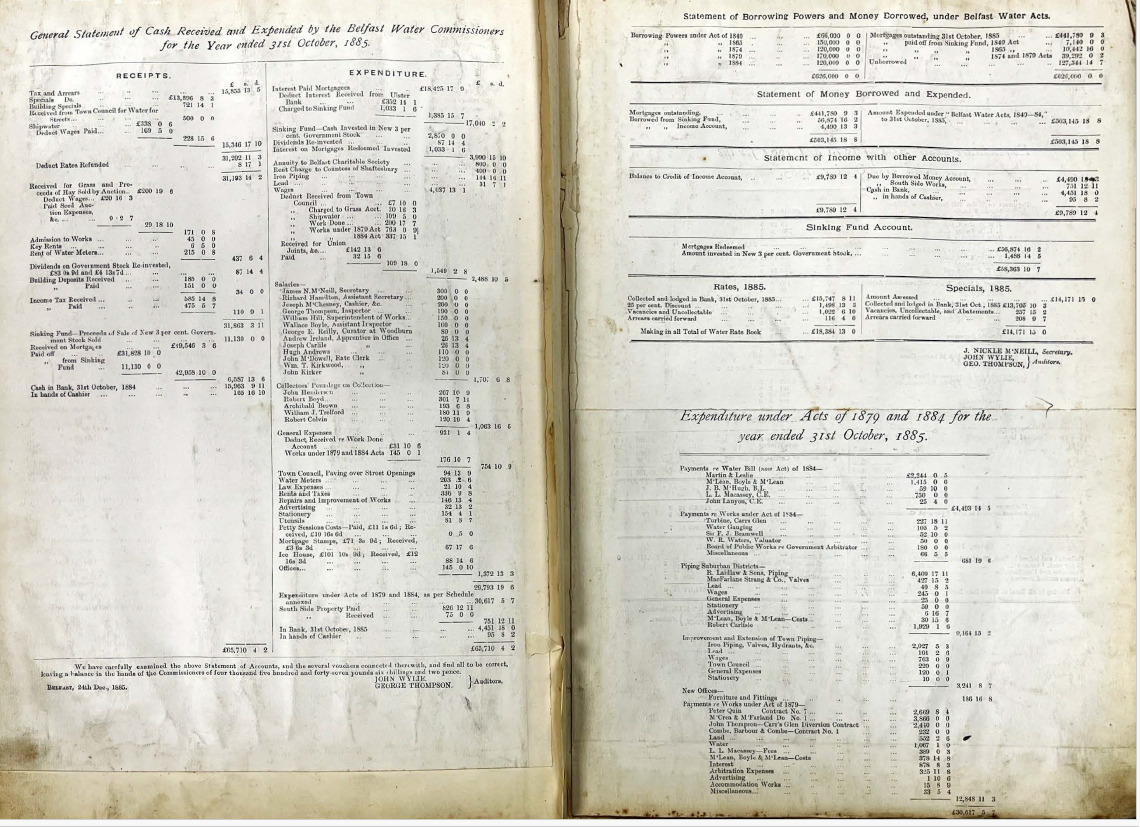

The 1884 Act was another incremental measure. It extended the territorial reach of the water supply and authorised increased capacity and financing, and there was no evidence of any departure from the accounting practices. By this point, after more than 40 years of operation, the Commissioners appear to have developed a well-organised financial administration and routines that were regarded as effective in managing the water utility. So, the financial records remained with one set of books for the whole water undertaking, with internal distinctions for each project. The audit mechanism appeared to remain unchanged with the same process of an annual independent audit by elected auditors. Hence, the 1884 Act reaffirmed the continuity of accounting and audit practices. Local oversight and ingrained financial routines remained the trusted pillars of governance – see Figure 7.

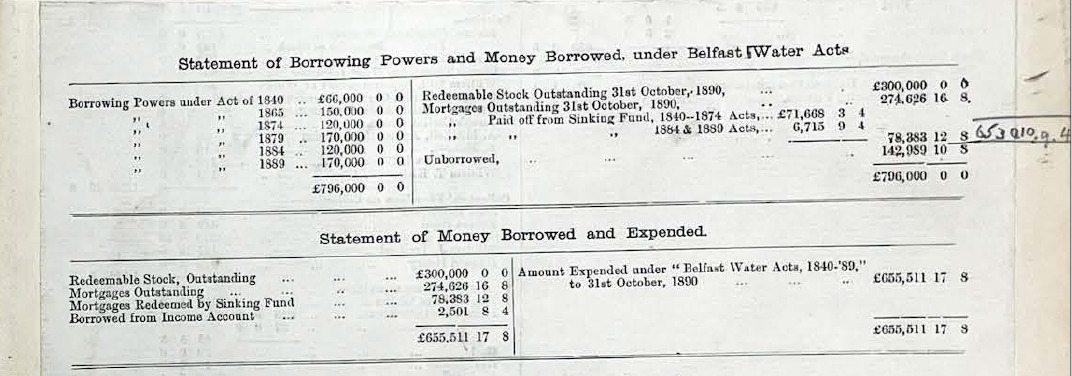

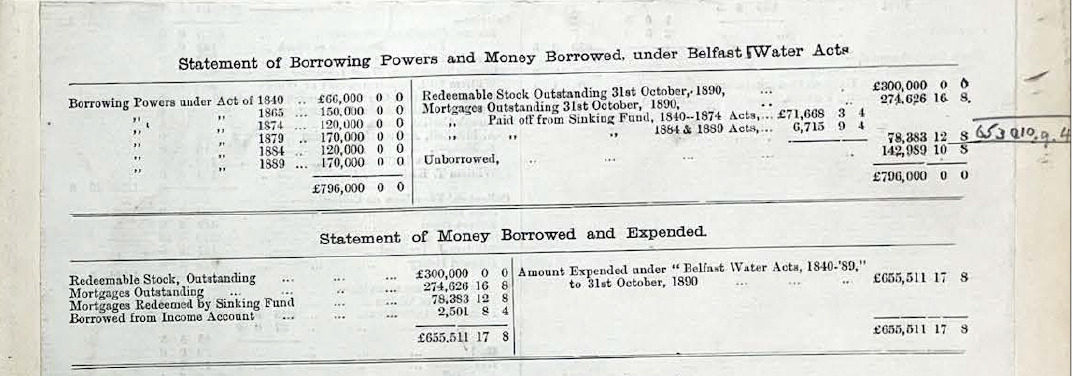

Finally, the Belfast Water Act 1889 was passed toward the end of our study period. This Act again largely maintained the status quo of the Commissioners’ accounting practices and annual audit by locally appointed auditors. However, it introduced at least two noteworthy provisions marking financial modernisation and the increasing involvement of a central authority. First, the 1889 Act allowed the BWC to issue stock, a form of bonded debt or municipal stock, essentially expanding its financing options beyond traditional loans or mortgages. In line with many late 19th-century municipal reforms, this provision gave the BWC access to a broader capital market by issuing securities that could be traded, which could potentially lower borrowing costs or attract more investment for large-scale works. Indeed, the BWC’s accounts for the year 1890 show expenditures related to the first issuance of stock, indicating that the Commissioners took advantage of this new power to raise funds. This move toward issuing stock, see Figure 8, suggests a possible step toward a more sophisticated financial management system, possibly influenced by normative pressures as other cities and utilities began to adopt such practices.

Second, and importantly for accountability, the 1889 Act for the first time required that an abstract of the annual accounts be sent to a central authority, namely the Local Government Board (LGB) (Ireland). By 1889, the LGB had oversight of various aspects of local authorities in Ireland (the LGB had been established in the 1870s to supervise Poor Law Unions and, increasingly, other local bodies). Section 59 of the 1889 Act mandated the BWC to forward a summary of its accounts to the LGB, a measure that might be interpretated as adding some external oversight beyond local ratepayers. While the LGB might not have actively audited these accounts, this step seemed to keep central government aware of the BWC’s financial position and may have allowed it to raise queries where necessary. This step can be understood as aligning with a broader late-century movement toward standardisation and supervision of local government finance in the UK and Ireland, influenced by emerging views that services such as water should be subject to both local and national expectations of accountability and efficiency.

Thus, the archival evidence portrays an organisation balancing on one hand the need to adapt to a changing city, new laws and increasing public scrutiny, and on the other hand a path-dependent reliance on familiar accounting routines and structures that had served it well. In the next section, we delve deeper into interpreting these findings, using Scott’s (2014) pillars of institutions as a framework to understand the influences behind the observed patterns of accounting change and stability.

6. Discussion

The regulative pillar which encompasses formal rules, laws and enforcement mechanisms acted as a dominant force shaping the BWC’s accounting practices. These findings speak directly to the gaps highlighted in the literature review. As noted earlier, accounting history in an Irish context has focused largely on private-sector cases (Moreno & Quinn, 2020; Quinn, 2014; Quinn & Jackson, 2014), with no prior accounting history studies on organisations located in what is now Northern Ireland and very little on water utilities (Jack & Napier, 2023; Quinn & Bertz, 2024). By examining the BWC, this study therefore provides new empirical material from an underexplored context and allows comparison with both Irish accounting histories and the broader local government accounting literature (Coombs & Edwards, 1995; Sargiacomo & Gomes, 2011).

From the very inception of the BWC under the 1840 Act, legal mandates explicitly structured how accounting would be carried out. This statute established the Commission as a corporate body with defined governance and required comprehensive record-keeping, that was all monies received and disbursed had to be duly recorded, with every contract, receipt, payment and order entered into proper books. This early legislation effectively embedded key accounting rules into the organisation’s operations. For example, the Act forced the appointment of a treasurer, clerk, collector and engineer, each with segregated financial responsibilities, and mandated that no single individual could hold both the clerk and treasurer positions. Such provisions enforced checks and balances and ensured that financial transactions were documented and cross-verified as a matter of routine. In Scott’s (2014) terms, these were coercive rules that conferred legitimacy on certain practices, such as maintaining detailed receipt and payment books, preserving vouchers for every expense and regularly producing a statement of accounts, by making them compulsory for the BWC’s continued operation. Accounting practices at the BWC thus began not as ad-hoc choices but as codified requirements, instilling what Burns and Scapens (2000) described as institutionalised accounting habits from the outset. This is consistent with wider 19th-century developments identified in the literature, where municipal and public bodies often had accounting systems that were structured initially by statute rather than by internal innovation (Coombs & Edwards, 1995).

Crucially, the regulative environment not only prescribed the nature of record-keeping but also created an oversight framework that became institutionalised within the BWC’s accounting rules and routines, a pattern consistent with findings in prior accounting history research (Moreno & Quinn, 2020; Quinn & Jackson, 2014). The 1840 Act stipulated that independent local auditors drawn from among rate-paying citizens be appointed to examine the accounts. Accounts had to be prepared at year-end in a prescribed receipts and disbursements form and submitted for audit, after which the audited accounts were presented to the ratepayers in a general meeting. This created a recurrent annual (and at first, triennial) cycle of accounting activities (i.e. closing the books, auditing, reporting) enshrined in law. Even the timing was legislated with the BWC’s financial year ended April 30, with audits and public meetings scheduled by statute. In effect, the law turned financial management into a routine calendar of duties. Such routinisation under legal pressure illustrates how the regulative pillar can powerfully shape organisational behaviour as the BWC faced clear sanctions for non-compliance (e.g. legal action against officers who failed to produce accounts or vouchers on demand) (Scott, 2014). This observation echoes the more general pattern identified by Sargiacomo and Gomes (2011) that local government accounting practices were often strongly shaped by statute and accountability requirements.

Over time, as Belfast grew and its water undertaking became more complex, new legislation periodically adjusted the regulative framework, but these changes tended to reinforce and extend the existing accounting routines rather than overturn them. This pattern reflects how regulative structures typically stabilise and embed practices within organisations (Burns & Scapens, 2000; Scott, 2014). The Belfast Water Act 1865, for instance, was enacted “for better supplying Belfast… and for altering and amending” the BWC’s constitution. In practice, however, the 1865 Act modernised governance (e.g. expanding the Commission’s jurisdiction and representation) while preserving fundamental accounting roles and duties, consistent with the tendency for public-sector reforms to extend existing routines rather than introduce radical change (Carnegie & Napier, 1996, 2002).

Critically, the Act introduced an annual audit and reporting in place of the previous three-year requirement. The new provision mandated two auditors elected annually by ratepayers and an annual general meeting at which audited accounts were presented. This change increased the frequency of an already established routine, thereby tightening regulative oversight rather than altering the underlying nature of accounting practices (see routines as described by Quinn, 2014 and Quinn & Jackson, 2014). The BWC nevertheless continued to maintain its books on a receipts and payments basis and to prepare straightforward annual income and expenditure statements. This type of “more of the same” change is similar to the long-run stability observed by Quinn (2014).

Subsequent legislation – the Acts of 1874 and 1879 – extended the Commission’s operational powers authorising new water works or territorial expansion, yet again without fundamentally modifying accounting practices or internal controls. Such continuity reflects how regulative regimes in public bodies often reproduce earlier statutory requirements for maintaining full accounts, to support every entry with vouchers and to undergo an independent audit, thereby reaffirming those routines in each new act. The path dependency is evident, as in, once certain accounting practices were encoded in law, they became self-reinforcing. The BWC’s officers and Commissioners, accustomed to the legal mandates, continued doing things a certain way unless external pressures or circumstances necessitated a change (Scott, 2014). Thus, the regulative pillar created a strong backbone of stability in the BWC’s accounting. Change, when it came, was typically incremental and externally driven for instance rather than being spontaneous innovation pushed from within (for instance, the 1865 Act directed the account reporting and audit frequency change and the 1889 Act powered the new reporting requirements). This is similar to Quinn (2014) and Moreno and Quinn (2020) where rules and routines were shown to endure over long periods and to shift primarily when pushed by external events or institutional pressures.

By the late 1880s, the regulative environment evolved further to reflect broader trends in public sector oversight. The Belfast Water Act 1889 left the core accounting routines and local audit intact but introduced two significant regulative innovations, that was the power for the BWC to issue municipal stock and the requirement to submit annual account abstracts to the central LGB (Ireland). The stock provision expanded the BWC’s financing options beyond traditional loans, illustrating how laws could add new layers of financial complexity that the accounting system had to accommodate (e.g. accounting for stock issuance and related expenditures appeared in the 1890 accounts). The mandate to forward accounts to the LGB brought in a form of central government oversight for the first time. While the LGB did not audit the BWC’s books, this requirement meant that the BWC’s accounts were now subject to scrutiny against national norms and expectations of efficiency in local government finance. In Scott’s (2014) framework, this represents a strengthening of the regulative pillar via higher-level institutional pressure. The BWC’s accounting routines now had to not only satisfy local stakeholders but also align with the information demands of a central authority. This finding resonates with Coombs and Edwards’ (1995) observation that central legislation and oversight increasingly shaped British municipal reporting. The BWC shows, however, that such central scrutiny could be layered onto an existing cash-based system without transforming its underlying logic.

These changes built upon the BWC’s existing foundations as by 1889 the BWC had already nearly five decades of compliant accounting practice, so adapting to new regulative requirements (like preparing an abstract for the LGB) was likely seen as another step in duty rather than a radical shift. The overall picture is one where laws decisively shaped what counted as proper accounting, providing stability by institutionalising routines and driving change mainly when laws themselves changed. Regulative forces thus explain much of the continuity in the BWC’s accounting – as long as the BWC operated within a steady legislative framework, its financial practices remained a stable, rule-governed routine. Compared with the broader pattern identified by Sargiacomo and Gomes (2011), who noted a greater variety in local government accounting change across countries and periods, this case underscores the particularly strong role of regulation and path dependency in a Victorian utility context.

Beyond the coercive rules of law, the normative pillar of values, expectations and social norms around appropriate behaviour also influenced the BWC’s accounting practices. In Belfast, water was a civic matter and the Water Commissioners were stewards of a public resource. There were normative expectations of transparency and accountability that the BWC had to uphold. The structures set out by law (accounts, audit, public meetings) did not operate in a vacuum; they resonated with norms of civic governance. This is consistent with Carnegie and Napier (2012) (also see McBride & Verma (2021)), who emphasised the role of broader social values and notions of public stewardship in shaping accountability practices in the 19th and early 20th centuries.

For instance, the requirement to hold public meetings where ratepayers could inspect and question the accounts every three years (and subsequently annually) reflects a normative culture where public scrutiny was not just allowed but expected. The local press and community showed active interest in the water supply finances, as evidenced by newspaper notices giving attention to the BWC’s financial dealings. This media attention implicitly pressured the Commissioners to be honest, reinforcing a norm that public utilities must be publicly accountable. In other words, even if the 1840 Act mandated audits and meetings, it was the Victorian norm of civic responsibility that gave those mandates their significance as failing to present clear accounts or address ratepayer concerns would have been seen as a breach of duty and trust. Thus, normative forces worked together with regulative rules, encouraging compliance not just out of fear of legal penalty but from a sense of propriety and legitimacy in the eyes of the community (Suchman, 1995).

Signs of normative pressure are seen in the gradual increase in detail and formality of accounts reporting over the decades. By the 1870s, the BWC’s annual accounts had become more granular and professionally presented (transitioning from handwritten accounts to typed accounts). While the law did not explicitly demand typed or highly detailed accounts, the move to provide more line items and a clearer format suggests a response to unwritten expectations. As Belfast city and its finances grew, stakeholders likely expected more information and clarity. The inclusion of a Secretary’s signature on the later 1870s accounts hints at a growing administrative professionalism within the BWC. This could reflect emerging normative influences from the broader municipal sector. Here, the case of the BWC complements studies such as Quinn and Bertz (2024), who showed how accounting practices in local government are shaped by a combination of economic and public health concerns, both of which carry strong normative overtones about proper stewardship of public resources.

Similarly, the 1889 Act’s allowance for issuing stock, while a regulative change, could have possibly been influenced by normative pressures as other cities and utilities began to adopt such practices. In other words, the BWC’s move toward a more sophisticated financing method was in line with what was becoming a norm among peer institutions in the late 19th century. Even without direct coercion, seeing other municipal utilities successfully issue municipal stock would have created a normative impetus for the BWC to do the same to remain progressive and reputable. The normative pillar here is evident as a mimetic tendency (to follow what others deem good practice) and a standard of legitimacy (to be seen as up to date in financial management), something that also aligns with DiMaggio and Powell’s (1983) notion of mimetic and normative isomorphism.

Local civic norms also reinforced routine accountability. The fact that auditors were drawn from respected local ratepayers and that their role was reaffirmed in each Act indicates that having community representatives scrutinise the books was itself a valued norm. This practice persisted even when, by the late 1880s, professional accounting in the modern sense was taking off in Ireland (Annisette & O’Regan, 2007). The BWC continued to rely on lay auditors rather than outside accountants. The Commissioners and the community seem to have trusted this traditional model of oversight, suggesting a normative belief that honest citizens could ensure accountability as effectively as any professional auditor. The BWC diverges from Coombs and Edwards’ (1995) findings where municipalities turned to professional accountants.

Indeed, well into the late 19th century, public accountability remained a locally driven affair with statements of account published in newspapers ahead of public meetings and inviting community review. Discussions in those meetings provided a forum for normative feedback based on whether the Commissioners managed funds in line with societal expectations of stewardship. There is no evidence in the archives of any scandal or strong public outcry over the BWC’s accounting during the period studied, which implies that BWC’s routines succeeded in meeting the normative benchmark of good public management in the eyes of its contemporaries. We might say the BWC enjoyed a degree of moral legitimacy (Suchman, 1995) in its financial management. By adhering to norms of transparency and regular reporting, it maintained public confidence. This finding echoes Giorgino and Barnabè’s (2024) argument that accounting for water can underpin broader social and environmental objectives, but here in a Victorian, rather than medieval, context.

However, it is also worth noting the relative absence of certain normative influences that might have prompted change. Unlike private firms or some larger municipalities, the BWC did not face pressure from an accounting profession. The accounting profession in the UK and Ireland was still evolving in this era and municipal corporations only gradually adopted professional accounting standards. In the case of the BWC, the normative environment seems to have been dominated by local civic values rather than professional accounting norms. As Quinn and Moreno (2024) observed in a different historical context, a weak presence of formalised accounting education or professional norms can mean that compliance with the basic legislative requirements becomes the primary “need” for accounting, with little incentive to go beyond that. The BWC’s accounting practices indeed appear to have focused on fulfilling statutory and civic expectations of balancing the books, avoiding deficits and providing accountability to ratepayers. They did not venture into more advanced accounting techniques that were not yet normatively demanded. The normative pillar in the BWC case complements the regulative pillar by promoting adherence and stability. Civic expectations encouraged the Commissioners to follow the established routines and to gradually enhance disclosure in line with what the public deemed appropriate, but they did not push for radical changes so long as the BWC’s practices were seen as legitimate and adequate. This alignment of normative approval with existing routines contributed to the stability of accounting practices at the BWC across several decades.

The cultural-cognitive pillar refers to the shared understandings, taken-for-granted assumptions and ingrained ways of thinking that guide behaviour in an organisation (and which often go unquestioned by its members). In the context of the BWC, many of the accounting practices, once established by law and reinforced by norm, appear to have gradually become internalised as the way “things are actually done” (Burns & Scapens, 2000, p. 6). This pillar is subtler to observe in archival records, but several indications point to the BWC’s financial routines attaining a status of cultural common acceptance within the organisation. For example, the basic format of the BWC’s account statements were essentially a cash-based summary of receipts and expenditures/disbursements which remained fundamentally unchanged from the 1840s through to the 1880s. Only minor cosmetic tweaks occurred such as using the term “Disbursements” in some years instead of “Expenditure” and even those did not consistently persist. This uniformity suggests that the Commissioners and staff had a collective cognitive template for what an “account” should look like, likely rooted in the standard of the first accounts prepared under the 1840 Act. Over time, reproducing this format would have required little conscious deliberation as it was taken for granted as the way to present their transactions. Such continuity of format and approach, even as the scale of operations grew, indicates a cultural lock-in. The accounting routines had become institutionalised to the point that altering them was perhaps not even considered. At that time alternative accounting methods like accrual-based profit and loss statements lay outside the prevailing cognitive model of public-sector accounting within the BWC. This helps explain why some of the innovations noted by Coombs and Edwards (1995) in English local governments did not emerge in the Belfast water context.

Internally, the roles and language around accounting also demonstrate cultural-cognitive stability. For example, the treasurer, clerk, auditors (and later secretary) titles and functions carried on with continuity, and with them, the associated expectations. The treasurer was always the custodian of money, the clerk kept the books, the auditors checked the figures. These roles were defined by law, but decades of practice cemented them in the organisational culture. One can assume that new Commissioners or staff joining the BWC were socialised into these practices, learning from predecessors the routine of recording every receipt and payment, the procedure of authorising disbursements with a signed order and the cycle of annually closing accounts. The archival evidence shows no controversy or debate about these procedures implying that the procedures were unquestioned internally. For instance, even when the volume of transactions increased significantly, the BWC did not radically redesign the ledger system, but kept one set of books for the whole undertaking, with internal distinctions by project as needed. This one-book system had been effective in managing water services and thus continued, a possible reflection of the shared belief that the established system was sufficient and proper. In cultural-cognitive terms, it is possible that the actors within the BWC had a common belief that if the auditors and public were satisfied, the accounting process was correct. This shared mindset would have been reinforced at every annual audit and public meeting, which served as a ritual confirming of the BWC’s way of accounting as legitimate (Scapens, 2006; Suchman, 1995).

Successive favourable audits and the absence of financial scandal appeared to have strengthened the taken-for-granted nature of the routines. It is also possible to see cultural-cognitive influences in how the BWC responded to change. When new regulative demands arose (like the 1865 annual audit or the 1889 LGB returns), the BWC complied. The annual audit, once introduced, simply became part of the yearly routine which was a new norm that was quickly absorbed into how it operated as an organisation. The 1889 requirement to send accounts to Dublin (to the LGB) might have been a challenge, but the BWC had been publishing abstracts in newspapers for locals for years, so sending an abstract to a government office likely seemed a logical extension of what it already did. In other words, the BWC’s organisational culture was adaptable but possibly only up to a point where it could embrace changes that were congruent with its existing practices and beliefs about accountability. The cultural-cognitive pillar thus underpins the inertia and stability observed. The routines had become the way things were at the BWC, and unless actors were confronted with reasons/contradictions to question them (which they were not, given the success of the water undertaking and the lack of crises), those routines appeared to endure unquestioned. This aligns with Scott’s (2014) view that the cultural-cognitive element of institutions provides the deepest social stability, as it involves shared understandings that make alternate ways of doing things less conceivable. This continuity suggests the accounting routines had become habituated/accustomed and internally legitimated, beyond mere rule compliance or external pressure. In comparison with other historical cases, such as Guinness (Quinn, 2014; Quinn & Jackson, 2014) or medieval Siena’s water system (Giorgino & Barnabè, 2024), the BWC appears to exemplify a form of institutionalism, where regulative, normative and cultural-cognitive pillars align to sustain a relatively simple yet enduring accounting system for a vital public utility.

Following Gomes and Sargiacomo (2013), the case shows that the rationales underlying accounting practices at the BWC were primarily institutional rather than technical. The Commissioners’ adherence to simple, cash-based accounting was justified not through efficiency or financial sophistication but through social expectations of civic stewardship, compliance with statutory norms, and taken-for-granted beliefs about what constituted ‘proper’ public accounting. These rationales, rooted in Victorian governance culture and reinforced by legislative oversight and community scrutiny, explain why practices remained stable for decades and why change occurred only when new institutional demands realigned these rationales.

7. Concluding Comments

This paper set out to explore the historical accounting practices of the BWC from 1840 to 1890, addressing a gap in both Irish accounting history and the accounting history of water. By examining the content and evolution of the BWC’s accounts and interpreting them through an institutional lens, we sought to understand both the continuity and change in their accounting practices over five decades. The findings illustrate how accounting routines were deeply shaped by the regulative environment, underpinned by civic norms, and gradually embedded into the cultural-cognitive fabric of the organisation.

While this research contributes to a better understanding of historical public water utility accounting in an Irish context, several limitations must be acknowledged. First, the study is grounded in a single case – the specific context of Belfast, a rapidly industrialising city in 19th-century Ireland. As such, the findings may not be generalisable to other local government bodies or to different historical or geographic settings. Second, while institutional theory, and particularly Scott’s (2014) tripartite model, has offered a valuable interpretive framework, our analysis, especially in relation to the cultural-cognitive pillar, is scrutinised through the lenses of the researchers. Archival materials provide limited access to the internal thought processes, beliefs and taken-for-granted assumptions of the historical actors involved. Thus, while we have inferred shared meanings and cognitive routines from patterns in practice, these remain interpretations rather than definitive accounts of the actors’ internal perspectives. Finally, the study responds to ongoing calls for more historical work on local government accounting and accounting for water but also highlights the broader need for further empirical studies in this area. Comparative studies could enrich our understanding of how institutional forces interact with local contexts to shape accounting routines.

In summary, this study offers an initial step toward recovering and understanding a neglected aspect of Irish accounting history. The case of the BWC demonstrates the enduring influence of legal mandates, civic norms and internalised routines in shaping public-sector accounting over time. However, a fuller picture of accounting’s role in historical water governance awaits further investigation, ideally drawing on diverse contexts and interdisciplinary approaches.

The reader is encouraged to explore the Irish Economic and Social History journal for further examples.