1. Introduction

Accounting history literature suggests there are advantages to examining phenomena over an extended historical timeframe (Quinn, 2014; Quinn et al., 2023). For example, “without knowledge of accounting’s past, we have only a limited point of reference from which to critique contemporary practice and thought” (Carnegie & Napier, 2012, p. 354). Such research contributes to understanding accounting concepts and theories of the present day (Cleary et al., 2019; Hiebl et al., 2015; Parker, 2015) as well as shifts over time (Morf et al., 2013).

The research objective of this paper is to explore the fortunes of an Irish railway company through its financial statements using an institutional lens. It aims to answer the research question: how do the three pillars of New Institutional Sociology explain the fortunes of railway companies in Ireland between 1884 and 1947? Edwards (2013) notes that the story of British railway management in the early 20th century is largely untold, and this is also true of Ireland. Although there is a substantial body of literature on the accounting history of railways (e.g. Antonelli et al., 2025; Arnold & McCartney, 2002; Bryer, 2025; J. R. Edwards, 1986; R. Edwards, 1998, 1999, 2010, 2011, 2013; Feeney, 2013; Hoskin & Macve, 2022; McCartney & Arnold, 2002, 2003; Miranti et al., 2023; Quail, 2006; Stevenson-Clarke & Bowden, 2018; Thompson, 2017), there is a dearth of literature in an Irish context. This paper responds to calls from McBride and Verma (2021) and Quinn et al. (2024) for such research by adding an Irish context to the comparative international accounting history literature. It explores the accounting history of railways in Ireland by studying the Londonderry & Lough Swilly Railway Company (hereafter the L&LSRC) from 1884 to 1947. This covers four distinct periods: (1) from 1884, when the earliest set of accounts are available, to 1900; (2) after the Companies Act 1900, which introduced the compulsory audit of accounts, to the partition of Ireland in 1921; (3) after partition to the start of World War II in 1939 (Ó Gráda, 1997); and (4) to the closure of the railway lines and the end of availability of annual accounts for the company in 1947. These time periods also broadly align with prior research on accounting history in railways of the United Kingdom (UK) (e.g., R. Edwards, 1998, 1999, 2010, 2011, 2013) given the amalgamation of Britain’s rail network in 1923, the start of World War II in 1939, and the subsequent nationalisation of the railways in 1947.

This paper makes several contributions to knowledge. Firstly, it is the first accounting history research on railway companies in an Irish context. Secondly, it highlights how the normative aspect is the dominant institutional factor in helping us understand how adapting to technological changes in the external institutional environment conversely provided stability for the L&LSRC.

2. Literature Review

2.1 Introduction

Accounting history has been the subject of much research for some time, offering valuable insights on accounting in history and contributing to our understanding of present-day accounting and business contexts. Prior literature, such as Carnegie and Napier (2002) and McBride and Verma (2021), note the importance of comparative international accounting history. However, as outlined in the Introduction above, there is a dearth of accounting history literature in an Irish context, and especially in relation to the accounting history of railways, which this paper addresses.

2.2 The Accounting History of Railways

The accounting history literature has found rich veins of material to mine on the railway industry, and there has been renewed interest in recent years. Hoskin and Macve (2022) even identify modern management as having been invented on the Pennsylvania Railroad in 1849, arguing that the beginning of the ‘management revolution’ was a crucial complement to the significant technological inventions of the Industrial Revolution. In the global accounting history literature, there are significant contributions based on railways on the interaction between infrastructure construction (Thompson, 2017), service management (Miranti et al., 2023), and the role of government and socio-economic repercussions (Antonelli et al., 2025). Researchers have also focused on the novel accounting practices developed in the 1800s in the United States (US) (Thompson, 2017) and the UK (Arnold & McCartney, 2002; J. R. Edwards, 1986) because of the railways. Accounting practices in different periods and in other countries (e.g. Stevenson-Clarke & Bowden, 2018), management accounting (R. Edwards, 1998; Quail, 2006) and auditing (Feeney, 2013) are also features of the accounting history literature on railway companies.

For example, Edwards (1998) finds that UK railway companies in the early 20th century used the tacit knowledge of managers to obtain an implicit understanding of their cost structures for the purpose of monitoring operations. Edwards (1999) further argues that implicit marginal costing was obtained from non-financial information outside the realm of accounting due to the specific conditions and complexity of operations faced by railway managers. Similarly, Edwards (2010) suggests that the London, Midland & Scottish Railway, although lacking financial sophistication, by reflecting upon internal processes delivered more efficient, although not necessarily more economical, working practices. In a related study, Edwards (2011) explores the implementation of a centralised system of train control in the 1920s and 1930s on the London, Midland & Scottish Railway to collect, collate and analyse information required for monitoring the conveyance of traffic and use of assets, to inform the history of management techniques as a set of routines and to offer caution on too rigorous interpretation of what constitutes specific operating routines as opposed to a separate dynamic capability.

Another strand of literature outlines the relationships between accounting practices and the British ‘railway mania’ crisis in the mid-19th century (e.g., McCartney & Arnold, 2002, 2003). Bryer (2025) notes that the reasons for the railway mania of 1845–1846 remain a puzzle, and proposes that it was a ‘social conspiracy’ by the elite class, whereby Britain’s transition from landed, commercial and money capitalism to industrial capitalism produced the conditions that facilitated the ‘swindle’ underlying the mania. Basing regulation on ‘gentlemanly’ capitalists’ political economy allowed railway directors to resist a falling rate of profit, swindling investors by unscrupulously understating depreciation. Combining private initiatives with public interest was a defining feature of 19th-century European economic policies, particularly in the development of railway systems (Antonelli et al., 2025). Using governmentality and legitimisation theory, Antonelli et al. (2025) demonstrate how accounting practices legitimised and drove the railway initiative in Italy, aligning political objectives, investor confidence, and community aspirations. The strategic use of financial data to shape consensus illustrates the political impact of accounting and its critical role in fostering infrastructure development in Italy.

2.3 Accounting History in an Irish Context

There are some valuable studies of accounting history set in an Irish context. One of the earlier contributions is Ó hOgartaigh and Ó hOgartaigh’s (2004) exploration of the corporate governance archives in the National Archives of Ireland and the Public Record Office of Northern Ireland. Another notable contribution in an Irish context is O’Regan and Killian’s (2021) finding that most accountants were acting independently in the field at the start of the 20th century, with no strategies to act in concert or to erect occupational barriers to entry. The small minority of accountants in Ireland pursuing professionalisation came from a background that was already elite. A more recent example is the contribution by Quinn et al. (2023) to the relatively limited literature on the history of social and environmental accounting/accountability by analysing a fisheries-related section of an annual report of the Irish state-owned electricity company (Electricity Supply Board) for 56 years (1935/36–1993). However, there is relatively little in an Irish context in the overall comparative international accounting history literature (Quinn et al., 2024), and there have not been any accounting history papers on railways in an Irish context. This exploratory research aims to contribute to filling this gap in the literature.

3. Research Methods

3.1 The Londonderry & Lough Swilly Railway Company

Accounting history studies over an extended historical timeframe can support analysis of financial statements as information about business model execution connecting with the wider economic context, or reveal the evolution of an object of study such as the textual characteristics of reports over time through a more case study-based approach that examines financial reports as text (e.g., Moreno et al., 2019). The research behind this paper adopts a qualitative approach to connect business models with the wider economic context by examining the long period of operations from 1884 to 1947 of a single railway company. Historians have engaged with accounting and business archives primarily in the areas of social and economic history. While much of economic and social history draws on macroeconomic data, micro- and firm-level sources have cast new light on old historical issues, such as the development of trade in Ireland and between Ireland and overseas (Ó hOgartaigh & Ó hOgartaigh, 2004). One reason the L&LSRC was chosen is the availability of half-yearly accounts (six-month accounting periods) from 1884 to 1912 and of annual accounts from 1913 to 1947.

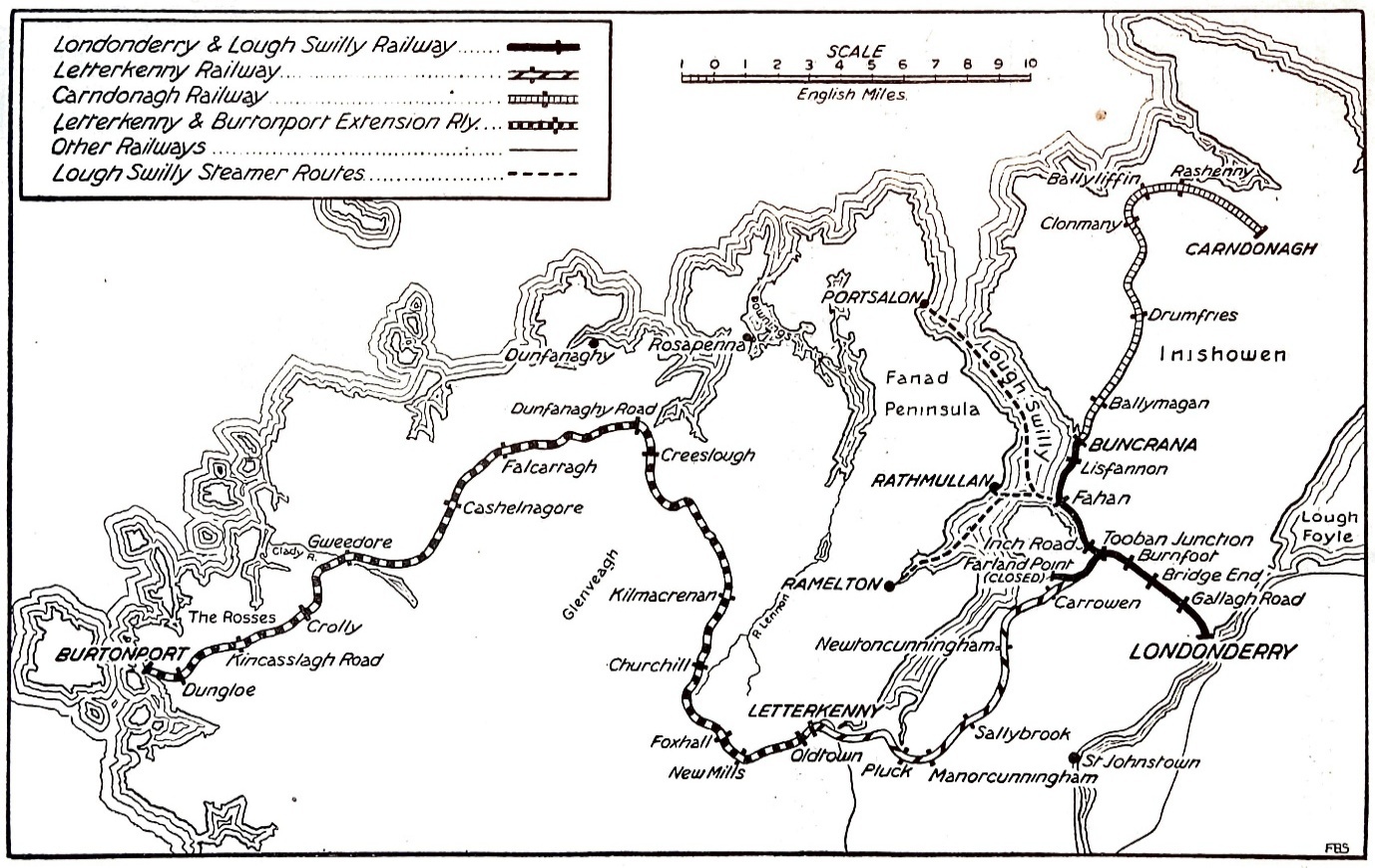

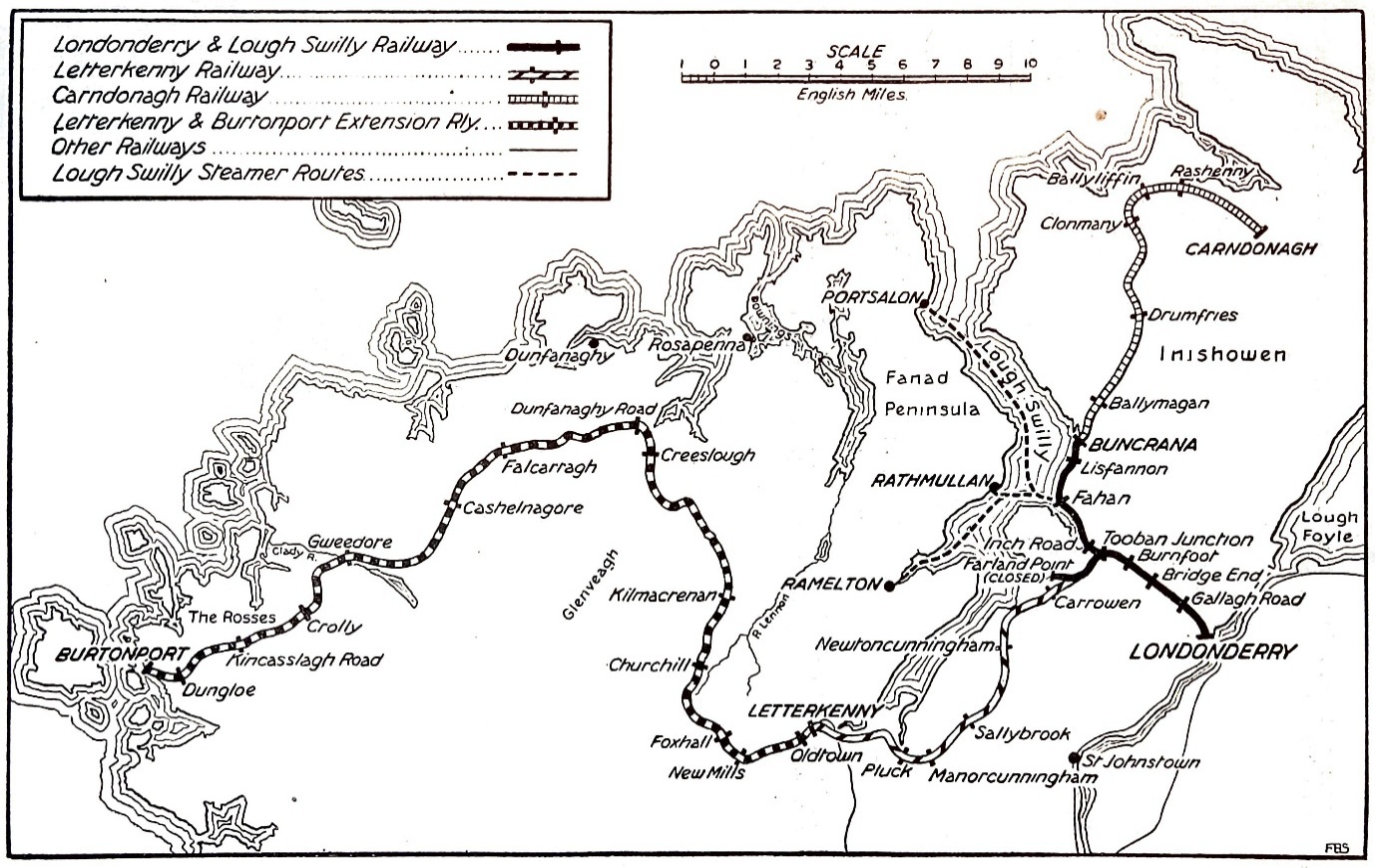

The L&LSRC was an Irish public transport and freight company incorporated in June 1853 by an Act of Parliament (J. McBride, 2022). Ulster was the most industrialised of the four Irish provinces pre-partition in 1921, where the company operated primarily in Counties Derry and Donegal (see Figure 1). In 1885, it converted its track from 5ft 3in (1,600 mm) gauge to 3ft (914 mm) narrow gauge to enable through-running (Hajducki, 1974). In 1887, ownership of the Letterkenny Railway passed to the Irish Board of Works, which continued the agreement by which the company operated the line (Hajducki, 1974). It closed its last short remnant railway line in July 1953.

Notably, the company continued to operate bus services until April 2014, when it went into liquidation, making it by then the oldest railway company established in the Victorian era to continue trading as a commercial concern (J. McBride, 2022). Lee and Saunders (2017) consider researching such outlier case studies to be a valuable means of adding to our knowledge and understanding of processes, behaviour, and theoretical explanations.

The accounts/annual reports of the company from 1884 to 1947 were accessed via the historical records section of the Córas Iompair Éireann (CIÉ) website in early 2025.[1] The accounts/annual reports were reviewed and analysed for both narrative content such as the directors’ report and the auditors’ report, and also for key accounting and operational numbers provided in the financial statements and in other disclosures, as well as other characteristics such as the overall length of the annual accounts, for example.

The analysis is divided into four distinct time periods. The first period is from 1884, when the earliest set of accounts is available, to 1900 when the Companies Act 1900 introduced the compulsory audit of accounts. The second period is from 1901 until the partition of Ireland in 1921, which created a structural break (Turner, 2010). The third period is from 1921 until the start of World War II in 1939, which created another structural break (Ó Gráda, 1997). The fourth period, from 1940 to 1947, covers the years when the railway lines closed and the availability of annual reports for the company ended.

3.2 Neo-institutionalist Theory

One of the key roles of theorisation in historical accounting research is to make a bridge between the specific case study and more general concerns (Napier, 2022). Theorising can help the accounting historian by providing an initial framework for research design, identifying potentially important factors that can be searched for within the evidential material, and ensuring a coherent narrative that is representationally true and sensitive to context (Napier, 2022). This research adopts a neo-institutionalist history approach, using neo-institutionalist theory to illuminate historiography and to help interpret the findings, i.e., it uses institutional theory as a lens to interpret historical facts. Fowler and Keeper (2016) in their study of 20 years of accounting history literature observe how an institutional theory approach has been utilised previously by researchers. Neo-institutionalist history uses primary sources that are more familiar to business historians, such as internal organisational reports and minutes of meetings (Rowlinson & Hassard, 2013). Neo-institutionalist history provides a more rigorous approach to historical research, ensuring that it conforms to the standards of source criticism and verification that are generally accepted by historians. It also highlights the potential for research using the kind of documentary primary sources with which business historians are familiar. Another contribution of neo-institutionalist history is shifting the emphasis away from “importing historical data to illustrate organization theory” and towards “exporting theory to history” (Rowlinson & Hassard, 2013).

New Institutional Sociology is a theoretical perspective emphasising that formal rules, informal norms, and broader social structures and cultural beliefs shape organisational behaviour and outcomes, rather than solely focusing on individual actors’ economic rationality. This research draws on elements of New Institutional Sociology’s ‘three pillars’ (regulative, normative, and cultural-cognitive), which represent the core mechanisms that define and maintain institutions, providing them with structure, meaning, and a basis for social ordering (Scott, 2014). The regulative pillar focuses on rules, regulations, and formal guidelines that govern behaviour and activities within an institution, such as laws, policies, contracts, and specific procedures. The normative pillar emphasises values, beliefs, and ethical standards that shape attitudes and behaviours within an institution, such as cultural norms, moral codes, and professional ethics. The cultural-cognitive pillar encompasses shared knowledge, beliefs, and meanings that provide individuals with an understanding of the institution and its purpose, such as organisational culture, myths, symbols, and cognitive maps that shape how people perceive and interact within the institution (Scott, 2014). These three pillars are interconnected and work together to create a stable and meaningful social environment within institutions, and for how individuals behave, make decisions, and interact with each other within a given institution (Scott, 2014). For this research, each of the annual reports/accounts was reviewed and analysed through the prism of the three pillars of New Institutional Sociology. The findings and analysis are structured by evidence of the three pillars operating within the L&LSRC in each of the four distinct time periods from 1884 to 1947, and then synthesised to contextualise and theoretically frame their historical significance and contribution to knowledge. These will be described next with specific reference to the L&LSRC.

4. Findings and Analysis

4.1 1884–1900: Earliest Available Records to the Introduction of the Companies Act 1900

4.1.1 Regulative Pillar

An interesting aspect of the accounts from 1884 to 1900 is how the L&LSRC was operating commendable corporate governance and accounting practices, even when judged by modern standards (Kirwan et al., 2018). The accounts were prepared half-yearly for each six-month period ended 30 June and 31 December. The overall length of the “Report of Directors and Statement of Accounts to be submitted to the Shareholders at the Half-Yearly General Meeting” is 12 pages in 1884, and there is notice of an “Ordinary half-yearly meeting of the shareholders”, where the accounts were presented on 27 February 1885. The timeliness of the presentation of the accounts within two months of the period-end is noteworthy, as is the length of the report, and the holding of a general meeting for shareholders. The accounts are signed by the Chairman of the Board of Directors and by the Company Secretary.

Notably, the company was audited from the earliest available accounts in 1884. The external audit was possibly intended to protect investors in the company after the ‘railway mania’ of the 1840s (see Bryer, 2025, above), and it even predates the 1888 founding of the Institute of Chartered Accountants in Ireland. In 1884, the accounts are signed by two auditors (Richard Waller and George H. Mitchell) with “we hereby certify that the said Accounts contain a full and true statement of the financial condition of the company”. While the auditors’ report is only one paragraph, the phrase ‘full and true’ is recognisable today. The accounts are also signed by an engineer certifying that the company’s fixed assets are in good condition, and by a “Locomotive Superintendent” certifying that the “rolling stock” is in good condition. The accounts note that the auditors retire by rotation (this appears to be every two years for each auditor), but that each auditor is eligible to offer themselves for re-appointment.

There are nine directors of the company (all male). Two or three directors retire by rotation each year (although they can offer themselves for re-election and there are no limits on the number of terms they can serve). The directors’ report is one page. It is in professional but plain language, for example devoid of modern corporate jargon. It consists of current and prior-year comparisons of turnover broken down by (1) Passengers and Parcels (67% of turnover), (2) Goods (28%), (3) Livestock (4%), and (4) Rents (1%). There is also analysis and detail relating to turnover, expenditure, and operations. The directors’ report is both backward-looking and forward-looking. It is interesting that a directors’ report is presented to shareholders as early as 1884, with similar content in a modern-day directors’ report.

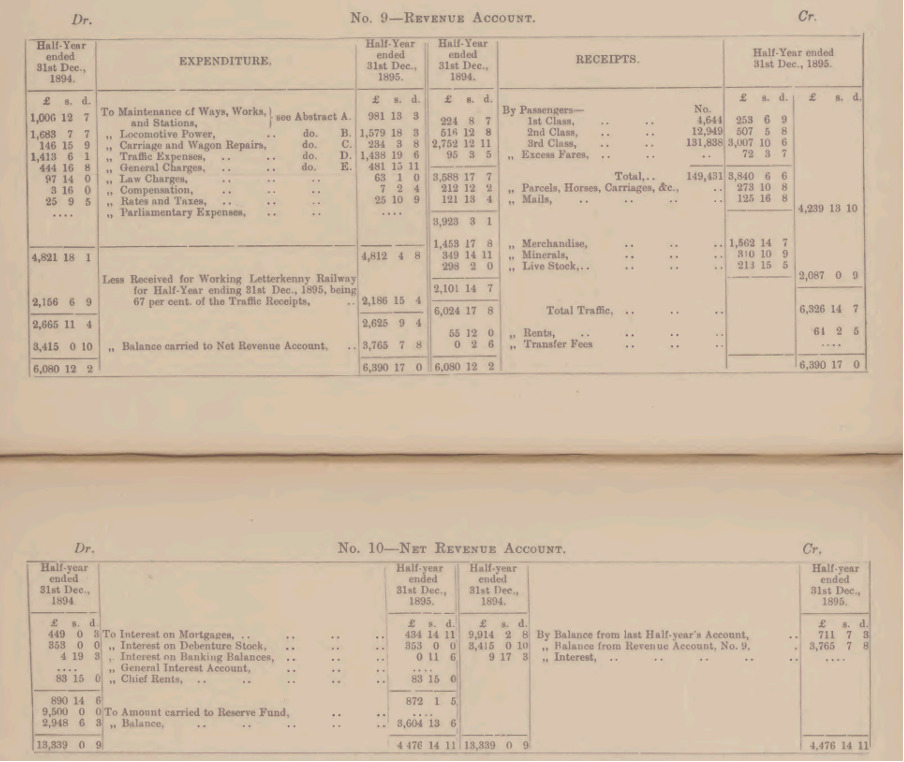

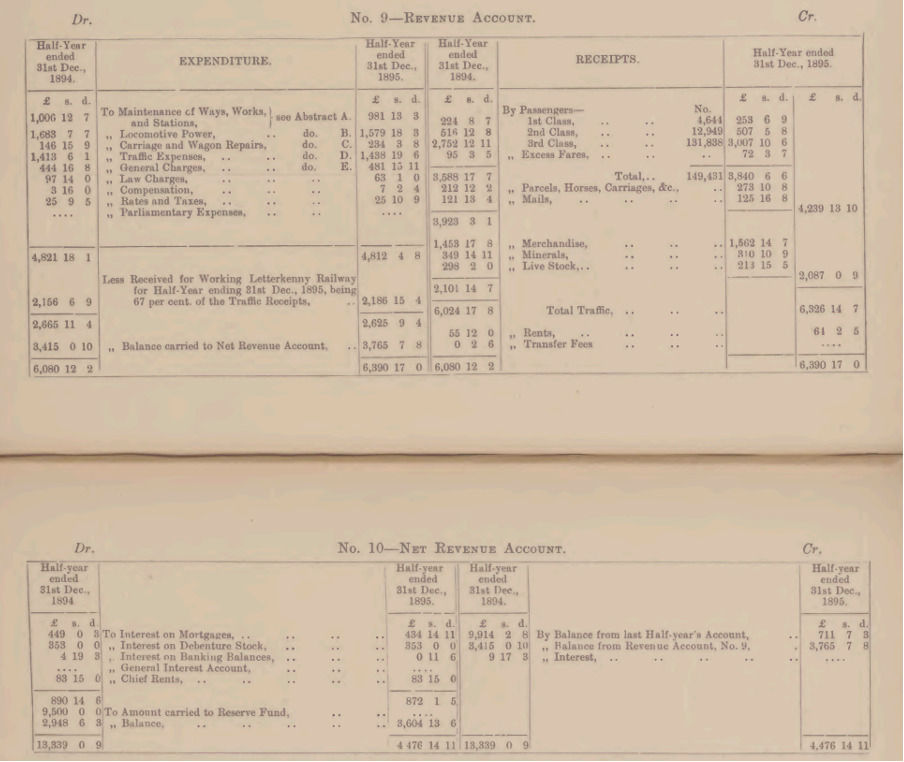

It is noteworthy that all the half-year reports are uniform in structure in terms of overall consistency of layout and headings, which makes it easy to compare them with reports from other reporting periods. However, a notable difference between these accounts and modern accounts is that they are not split into gross profit and net profit in the same way; for example, the expenditure headings are not categorised as ‘cost of sales’ and ‘overheads’ in the layout (see Figure 2). This ‘Revenue Account’ (the P&L equivalent) is presented as a ‘T-account’ (different to today). It shows both the number of passengers and the revenue from passengers by 1st class, 2nd class, and 3rd class. Notably, income and expenditure also show prior-year comparisons. Financing costs are split out separately, showing interest on mortgage and debenture loans, on debenture stock, on banking balances, and on the general interest account.

The ‘General Balance Sheet’ is also presented as a T-account (different to today), and includes, for example, the usual share capital, debts, ‘cash at bankers’, and ‘stock of materials on hand’. The notes to the accounts provide more detail on other aspects of the business. They split out ‘authorised share capital’ and ‘issued share capital’ (and distinguished between ordinary shares and preference shares). The notes also split out ‘authorised loan capital’ and ‘issued loan capital’, and receipts and expenditure on each capital account, such as on railway lines and on trains and carriages. The notes furthermore provide a breakdown of the company’s fixed asset register.

The accounts also have forward-looking disclosure notes: ‘Estimate of Further Expenditure on Capital Account’ and ‘Capital Powers and Other Assets Available to Meet Further Expenditure’. Interestingly, the 1885 directors’ report refers to the purchase of new rolling stock, funded by working capital with temporary loans to be repaid from revenue unless further capital can be raised. The company’s 1888 accounts note the “Directors offered the balance of the Preference Stock to the holders of that stock pro-rata, and are pleased to report that it was eagerly taken up by them. The proceeds of it have gone to clear off debts due in sundry directions, and the benefit of this will be seen in future half-years.” Notably, L&LSRC is replacing more expensive working capital with less expensive long-term capital. Note 3 to the accounts discloses ‘Capital Raised by Loans and Debenture Stock’, providing breakdowns in a way similar to that of a modern statement of changes in equity.

The 1889 accounts note that the shareholders will have to approve a resolution at the half-yearly general meeting to an increase in ‘Capital of the Company’ for a proposed extension of the railway line to Carndonagh. This requirement for resolutions to be approved at shareholder meetings demonstrates the existence of corporate governance processes. In 1896, a ‘Special Meeting of Proprietors’ notice is given to raise £30,000 of capital for the ‘Promotion under Tramways (Ireland) Acts of a Light Railway to Carndonagh’. In 1897, L&LSRC “engaged in negotiations with the Board of Works over the terms of constructing, working, and equipping the Carndonagh and Burtonport Extensions … the interests of the Shareholders are being safeguarded so far as is consistent with the obligations the Company is already under to the Board of Works.”

All the half-yearly accounts in this period show a grant of 67% of the ‘traffic receipts’ for the company working the Letterkenny railway line (only). This is shown in the revenue accounts as being netted off against the expenditure (see Figure 2). The Letterkenny line was owned by the Irish Board of Works and L&LSRC operated it like a modern public–private partnership agreement. Each set of accounts provide a statement of the number of miles of track (e.g., 31 miles owned by the company itself in 1885), and the number of miles covered by their train services (e.g. 42,168 miles in the 1885 half-year accounts, gradually increasing to 66,588 miles in the 1900 half-year accounts).

The reports reveal a surprising emphasis on what would now be termed ‘health & safety regulations’. The 1891 accounts note a fatal incident caused by a driver and guard not following ‘written’ procedures, which led to the subsequent setting up of a provision to cover claims by passengers (the provision is later closed in the 1893 accounts). Earlier, in 1886, the accounts mention renewing ‘the steel rails’ for the safety of the public, and that the ‘Permanent Way and Works’ and ‘Rolling Stock’ are “certified by the proper officers as properly maintained and in good working order”.

The accounts for the 1884 to 1900 period portray a gradually improving business. The 1888 accounts note a 5% dividend per annum on the preference shares. The 1891 accounts propose paying a 2% dividend to ordinary shareholders–this had not been noted in earlier accounts. In 1892, this dividend increases to 4% and the directors’ report notes “the largest gross and net earnings since the Line was opened for traffic … assuring the shareholders that they will yet be recouped for the patience and loss of dividends in the past”. In 1894, the directors’ report notes that 'since the last half-yearly meeting Counsel has been consulted with reference to the balance standing at credit of the Net Revenue Account, and he advises that the amount be transferred to a Reserve Fund Account". In 1898, the directors propose placing £400 into an ‘Engine Renewal Account’. These reserve funds illustrate sound corporate governance and future planning. In 1895, the dividend on ordinary shares increases to 6%, with the half-year accounts to 31 December 1895 illustrating a healthy profit margin for the L&LSRC, with a net profit after interest of £2,892 (i.e., a 45% profit margin after interest). In 1898, the dividend on ordinary shares increases to 7%; it then remains at 7% consistently until 1921.

4.1.2 Normative Pillar

The accounts of the L&LSRC also disclose directors’ remuneration and auditors’ fees. The directors were paid £75 between them per half-year from 1884 to 1900, and the auditors were paid £4 and 4 shillings (£4 4s) between them per half-year from 1884 to 1900 (in contrast to the modern era, these figures remained constant from 1884 until 1904). Reflecting on this, the overall impression from this period is of a prudently run business; for instance, the 1889 accounts note “the strictest economy and supervision, consistent of the right working of the Railway has been exercised by your Directors over every department”. (This is redolent of contemporary language around ‘lean business’.) Turnover is £4,952 for the half-year period to 31 December 1884 and this gradually increases to £7,910 for the period to 31 December 1900. Some statements in the accounts reflect insights into the wider economy, such as in 1886, when the directors’ report notes “an increase in every class of traffic during the half-year, which your Directors’ consider most satisfactory, taking into account the depressed state of trade and the reduced Receipts reported to nearly every other Railway Company in the Three Kingdoms”.

Many of the commercial challenges are similar to what businesses face now. In 1895, "[t]he storms of 22nd and 28th December last did immense damage to the Railway and to Fahan Pier. Immediate steps were taken to repair the damage and put everything in efficient working order, causing considerable increase in the expenses during the half-year, all of which has been charged to Revenue’ (i.e., adverse weather damage). In 1898, the directors’ report notes “the increased price of coal” (i.e., energy inflation). In 1900, there is an “increase in working expenses … due principally to the increased price of coal and materials used by railways generally” (i.e., general inflation).

On the expenditure side, the accounts in this period (1884–1900) provide details under five main headings: ‘Maintenance of Way, Works, etc’, ‘Locomotive Power’, ‘Repairs & Renewals of Carriages and Wagons’, ‘Traffic Expenses’, and ‘General Charges’. General Charges relate to what would now be called overheads, with the other four headings relating to cost of sales. Under each of these headings are cost breakdowns for salaries, materials, office expenses, horses, coal (for the steam engines), repairs, etc. This is very interesting, as it shows that the company’s accounting records are apportioning costs (e.g., wages and salaries, etc) between the different cost centres of the business.

4.1.3 Cultural-Cognitive Pillar

The annual reports for L&LSRC reveal that the company viewed itself as being embedded in the regional community, and a mutual reliance by the company on the fortunes of the people and economy of the region, and by the people and economy of the region on the transportation services provided by the L&LSRC. The 1889 report states: “Your Directors have again the pleasant duty of reporting the continued prosperity of the Railway … it is a source of much satisfaction to your Directors to see the prospects of a good harvest, and of continued prosperity throughout the land, and more especially the growing trade of the City of Derry and surrounding districts.” Similarly, responding to commercial demand, the 1887 annual report notes some customer feedback (probably from commuters): “Residents of the Line have drawn attention to the Directors to the necessity of a train leaving Derry after or about six p.m. during the winter months.”

4.2 1901–1920: From the Companies Act 1900 to the Partition of Ireland

4.2.1 Regulative Pillar

The Companies Act 1900 did not impact the presentation of the accounts for the L&LSRC, unlike many other businesses at this time. The accounts were already being externally audited, and they remained fully consistent with the same format in use from 1884 until the introduction of the Railway Companies (Accounts and Returns) Act 1911, which significantly changed the format of the accounts from then on.

In the half-year period ended 31 December 1901, the turnover is £8,140, split between Passengers & Parcels (65%), Goods & Minerals (31%), ‘Live Stock’ (3%), and Rents & Transfer Fees (1%). The rebate received for working the Letterkenny line is an additional £2,327. The accounts also show the company maintaining a consistent policy of paying a 5% dividend on the £49,625 preference shares (about half the share capital) and a 7% dividend on the £51,315 ordinary shares (about half the share capital). A new auditor, Andrew Armstrong, replaces the previous auditor in the period to 31 December 1901. The auditors’ report for the half-year 1901 states:

“We hereby certify that the above half-yearly Accounts contain a full and true statement of the financial conditions of the Company and that the dividends proposed to be declared on the several stocks and shares are bona fide due thereon, charging the Revenue of the half-year with all expenses which ought in our judgement to be paid thereout.”

In the half-year to 30 June 1903, the accounts note that the Burtonport Railway line extension was opened. Note 5 details that it raised £5,212 in ‘Guaranteed Stock (Shares)’, which it then paid over to the Government to build the railway on its behalf. The company raised this new share capital under the Tramways Order in Council (Ireland) (Londonderry and Lough Swilly (Letterkenny to Burtonport Extension) Railway) Confirmation Act 1898. The number of miles of track owned by the L&LSRC is now 99 miles, and for the half-year ended 31 December 1904 train service mileage increases to 157,405. Interestingly, there is also a first mention of a ‘Moiety Payable to Treasury’ for surplus receipts on the Carndonagh and Burtonport Railways (presumably part of their joint-venture agreement).

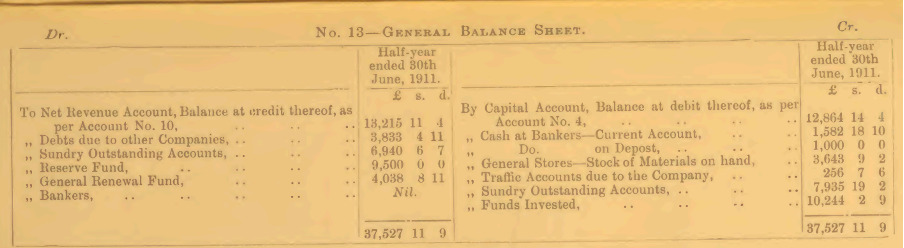

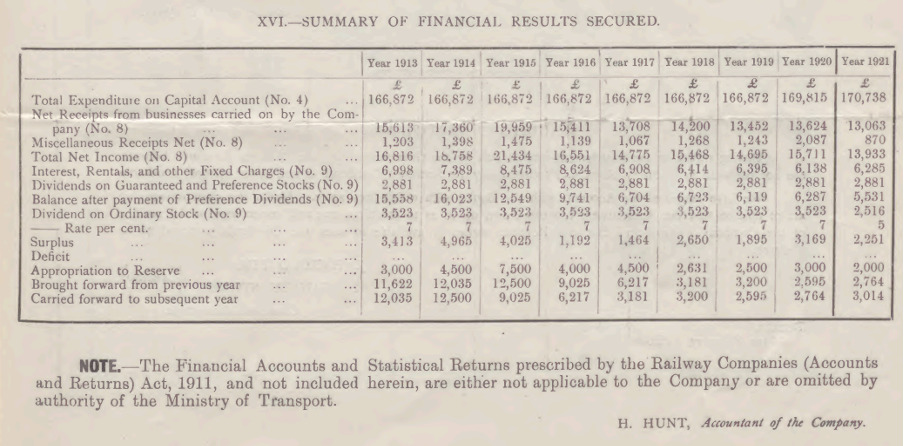

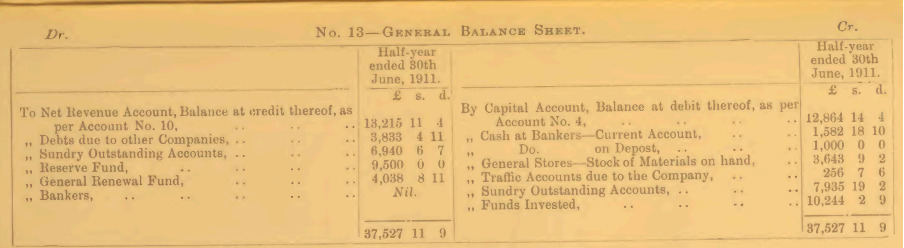

In the half-year ended 30 June 1911, the company replenishes a ‘General Renewal Fund’, “and placing £3,000 to General Renewal Fund, there remains a balance of £13,215 11s 4d available for Dividends” (see Figure 3).

In 1914, the accounts change significantly. Firstly, there is a notable change from half-yearly to “year ended 31st December 1914”. The 1914 accounts also show the first changes to the format since the earliest 1884 accounts: the accounts are now 21 pages in length (see Figure 4). This change in format (e.g., the inclusion of statistical returns breakdowns) is prescribed by the Railway Companies (Accounts and Returns) Act 1911. Overall, the accounts are remarkably sophisticated for what one would expect of financial statements in 1914.

_for_the_financial_accounts_and_statistical_returns.png)

The new statistical returns included in the accounts are interesting. They provide very detailed breakdowns of the assets that the company owns; they also show more financial analysis/management accounting in the accounts. For example, ‘Passenger Traffic and Receipts’ is broken into 1st, 2nd, and 3rd class, and by the number of passengers and income from each category. It then shows ‘average fare per passenger’, along with a comparative table for the prior year. There are similar breakdowns for ‘Goods Traffic & Receipts’ with breakdowns by tonnage, income, etc. A detailed map of the company’s railway network is included for the first time in its annual report. Graphical imagery, such as a map, is an unusual feature of accounts in this era.

1916 was a major inflection point for the railways in Ireland. The accounts of the L&LSRC for that year state:

“In pursuance of an Order in Council made on the 22nd December, 1916, under the provisions of the Regulation of the Forces Act, 1871, the control of the Irish Railways was taken over by the Government as from Midnight on the 31st December, 1916, for which purpose an Executive Committee was appointed, composed of General Managers of certain Companies, with the Under Secretary for Ireland as Chairman. Negotiations as to compensation to be paid by the Government are at present proceeding between the Board of Trade and the Irish Railway Executive Committee.”

It is not specified if this relates to World War I, or to events that followed the Easter Rising in Ireland. The accounts for 1917 and 1918 are not available. In 1919, the train service mileage is up to 267,169 miles. In 1919, the accounts state:

“The Statement of Accounts for the year 1919, is presented in a modified form to meet the situation arising out of the Control of the Railways by the Government, and the arrangement as to the compensation payable to the Railway Companies during such period of control … the customary reports from the officers in charge of the Permanent Way and Rolling Stock are attached, certifying that they have been maintained in as good order as possible, having regard to the circumstances and conditions arising out of the war.”

Notably, in 1919 the auditors are now Stokes Bros. & Pim of Dublin (precursors to KPMG), and the annual report states they are ‘Chartered Accountants’. (Auditors’ reports now include the phrase ‘true and correct view’.)

“Having regard to the arrangement entered into by the Government with the Railways, the above Accounts are not prepared in Statutory Form, and consequently the Statutory Certificate is not, in our opinion, applicable. We have examined the Accounts with the Books, with which they agree. Under the circumstances we are of opinion that the Accounts are properly drawn up so as to exhibit a true and correct view of the position of the Company’s affairs and that the Revenue shown is available to meet the Dividends proposed to be declared.”

However, even despite this wording by the auditors, the accounts are still remarkably detailed for their time. The accounts also split out other income after gross profit, such as rental income, interest income, and profit derived from sale of investments, etc., in much the same manner as today.

4.2.2 Normative Pillar

In 1904, the directors’ half-year remuneration increased to £125, and the auditors’ fees to £6 6s, the first increase since the 1884 accounts. Operationally, the L&LSRC shows confidence, with an emphasis on expansion at the beginning of this period. The most substantive developments in this period for the company are reaching Carndonagh (near Malin Head) by an extension completed in 1901 and completing a separate line to Burtonport (in the west Donegal Gaeltacht) in 1903. Both lines are constructed as joint ventures with the Government, with ownership and liabilities shared between the two parties (Hajducki, 1974). The L&LSRC also demonstrates an eagerness for continuous adaptation and modernisation. In the period to 31 December 1912, the accounts indicate technological advances by the company, for example: “Two new Engines of a powerful type have been placed on the Line during the half-year, and paid for out of Revenue.”

The L&LSRC continued to be an economical, lean and profitable business up to World War I. In 1914, at the start of the war, business is still on an upward trajectory: “The Receipts from all sources show an increase of £2,308 15s 2d, and the Working Expenses an increase of £562 6s 9d, when compared with the corresponding period of 1913.” Notably, the war is not mentioned in the accounts for 1914. In the 1915 accounts (signed by the auditors on 10 February 1916, a very quick turn-around time), turnover is £48,942 and profit before interest and dividends is £21,434, a profit margin of 44%.

4.2.3 Cultural-Cognitive Pillar

During this period, the Railway Companies (Accounts and Returns) Act 1911 standardised and modernised how British and Irish railway companies reported their finances and operational activities, mandating the submission of annual, detailed accounts and statistical returns in a prescribed format to the Board of Trade for oversight. The Act essentially unified accounting practices across diverse railway entities and was very important for improving the consistency of reporting and public transparency, providing comprehensive, comparable information for the government and public. In organisational contexts, the cultural-cognitive pillar can become powerful, because what initially were conscious, legally enforced rules later become subconscious, taken-for-granted shared beliefs and assumptions that underpin everything else. For the L&LSRC, such assumptions provide stability and meaning, and influence what information the directors regard as valid.

4.3 1921–1939: From Partition to the Start of World War II

4.3.1 Regulative Pillar

The partition of Ireland had a significant impact on the business of the company. Its headquarters in Derry/Londonderry and its main depot at Pennyburn Station were only two miles from the new border with the new Irish Free State, where it had the rest of its operations. For example, the 1923 accounts note “The Customs Arrangements between Northern Ireland and the Irish Free State, which came into operation on the 1st April, 1923, necessitated the Company making special arrangements at Londonderry and Tooban Junction for the carrying out of the work, and the cost has been placed to Capital Account.”

In 1921, the “Statement of Accounts for the Year 1921 is presented in a modified form to meet the situation arising out of the Control of the Railways by the Government, and the arrangement as to the compensation payable to the Railway Companies during such period of control.” The ordinary dividends have dropped to only 5% for the first time since 1898 (see Figure 5).

In 1922, the accounts return to the full format prescribed by the 1911 Act: “The Financial Accounts and Statistical Returns for the year ended 31st December, 1922, have been prepared in accordance with the Railway Companies (Accounts and Returns) Act, 1911. They have been duly audited and are presented herewith.” However, because of the commercial interruption caused by contemporary conflicts (World War I and/or the War of Independence), the 1922 accounts also state that the L&LSRC is “appropriating £26,000 from the Company’s share of the Compensation received under the Irish Railway (Settlement of Claims) Act, 1921”. The company also claims £19,000 from this fund in 1923 and continues claiming compensation until 1927. In 1922, the ordinary share dividend is reduced again to 3.5% (and ceases entirely from 1923), in response to commercial pressures. The 1922 accounts go on to state that: “Application has been made to Parliament asking for liberty to lodge a late Bill to enable this Company to raise Capital, and for other purposes.”

In 1925, the directors’ report starts using percentages for the first time when giving comparisons with prior years: “The Gross Traffic Receipts for the year amount to £62,727, compared with £64,467 for the year 1924, a decrease of £1,740, equal to 2.7 per cent.” Previously, numbers were stated but without percentages. Notably, there is no mention in the 1925 directors’ report of the Owencarrow Viaduct disaster in which four people died when a strong gale derailed two carriages, but its monetary effect to the company is accounted for in a separate line in the balance sheet as a ‘special item’ of £1,077 8s 7d.

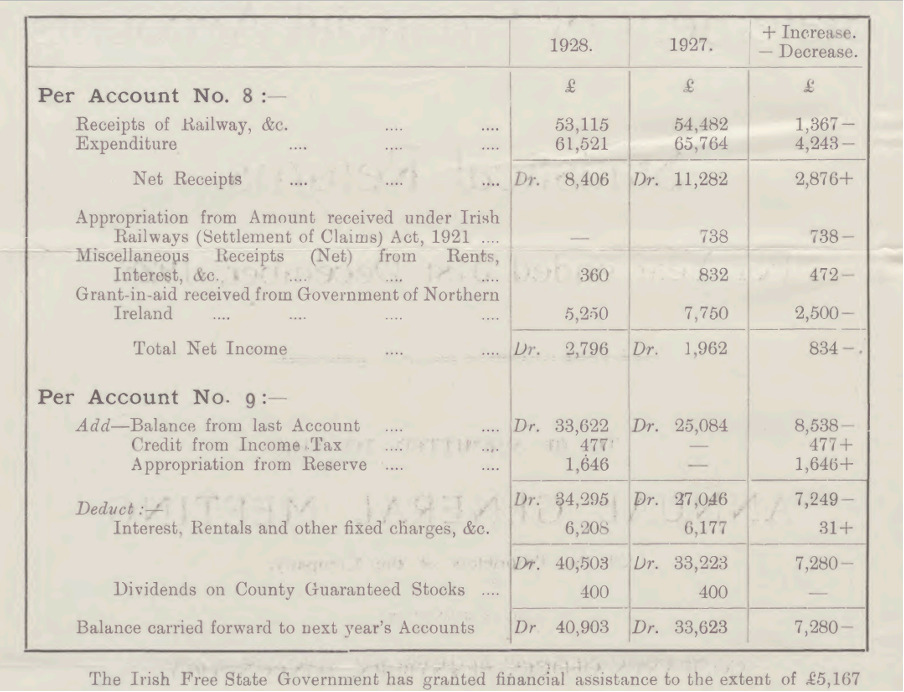

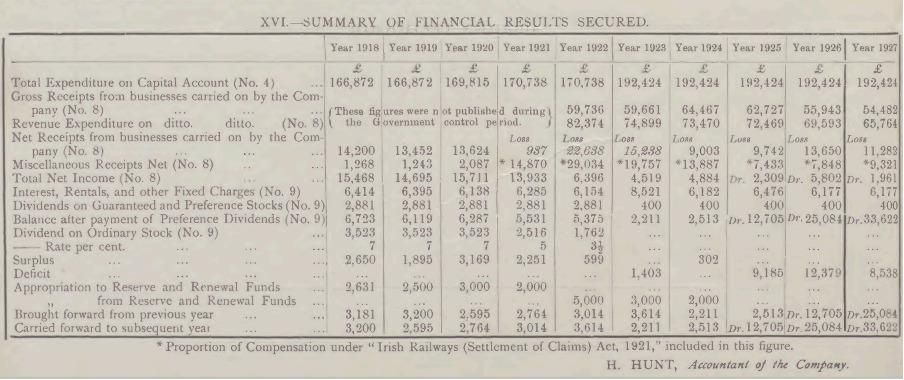

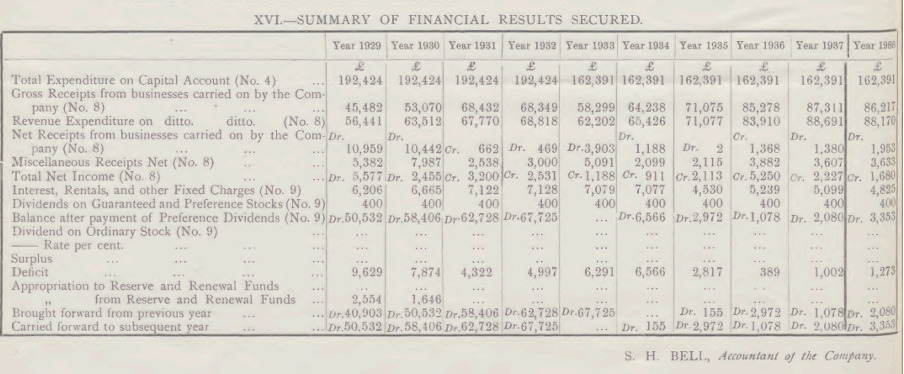

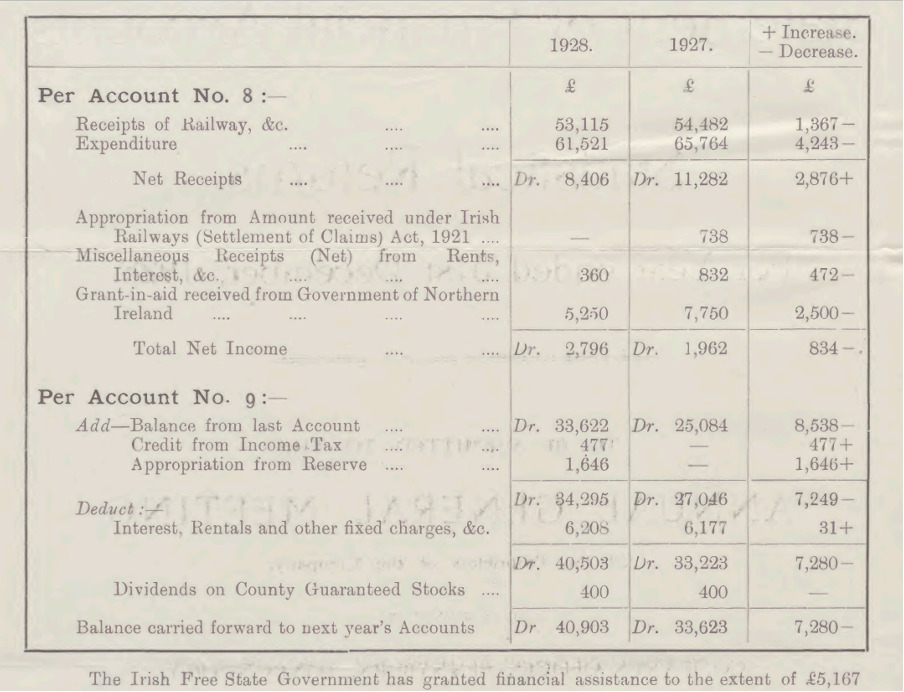

In 1928, there are several modernisations of the accounts. It is the first time the heading “To be submitted to the Annual General Meeting of the Proprietors of the Company” is used; since 1914 “Yearly Ordinary General Meeting” had been used. The 1928 directors’ report also provides a ‘Summary of Receipts and Expenditure on Revenue Account’ table, whereas this information had been provided in narrative form since 1914 (see Figure 6). This summary table is quite like the format of the modern income statement, which separates income and expenditure from non-trading items. Nevertheless, L&LSRC is now in negative equity (see Figure 7).

By 1927, there are only 14 sets of company accounts being collated for Irish railway businesses, with several clustered in the northwest of the island, including those for the L&LSRC, the County Donegal Railway, the Strabane & Letterkenny Railway, and the Castlederg and Victoria Bridge Tramway. When the largest railway company in Ireland – the Great Southern & Western Railway – announced the ceasing of operations in 1923, the Irish Free State government passed the Railways Act 1924 amalgamating four major railway companies and absorbing 22 smaller companies that were wholly within the Irish Free State into the new Great Southern Railways Company (GSRC). Only cross-border railways, such as the Great Northern Railway (GNR) and the L&LSRC remained independent. The Transport Act 1944 later merged the GSRC with the Dublin United Transport Company to form the modern semi-state company Córas Iompair Éireann in 1945 (Clements & McMahon, 2008).

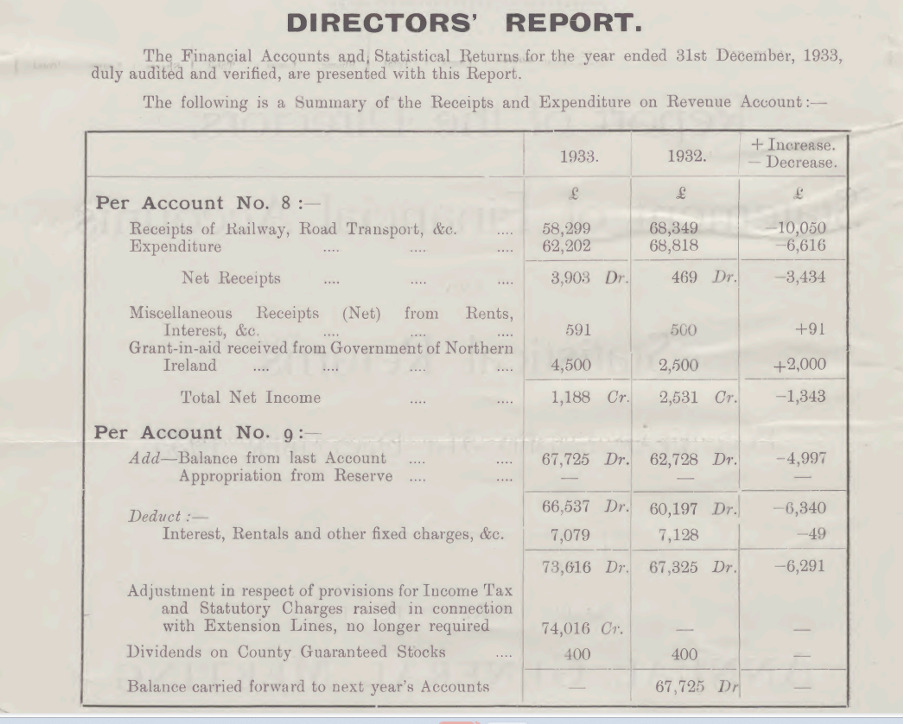

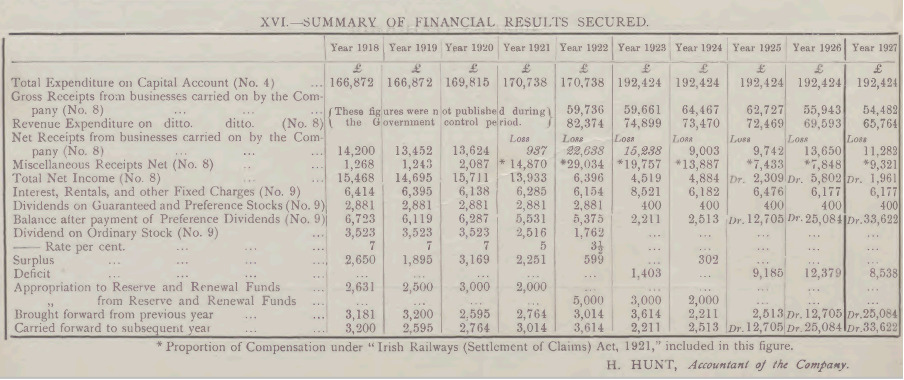

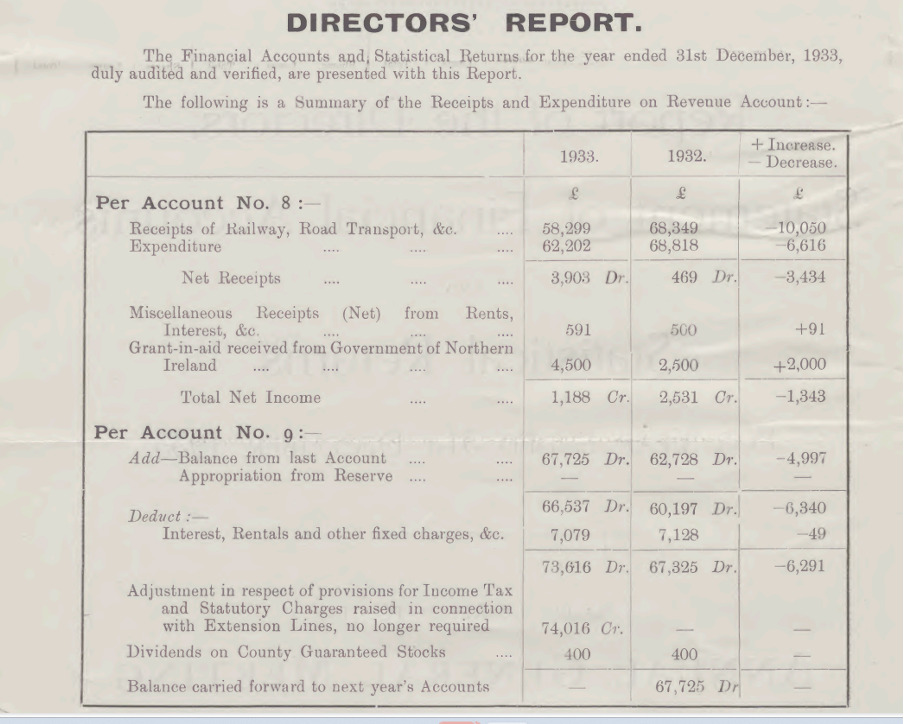

The 1933 accounts of the L&LSRC show an “Adjustment in respect of provisions for Income Tax and Statutory Charges raised in connection with Extension Lines, no longer required” of £74,016 (see Figure 8). The impact of this adjustment is to clear the negative equity from the balance sheet. The directors’ report for that year does not provide any more detail, nor do the notes to the accounts. The adjustment appears to relate to ‘Interest, Rentals & Other Fixed Charges, &c.’ of approximately £7,000 a year payable to the government, as train service mileage has reduced to 118,836 miles with the ceasing of some services (see also ‘Moiety Payable to Treasury’ mentioned in the 1904 accounts, as discussed above). The Irish Railway Tribunal was established under the Railways Act 1924 to provide for financial adjustments based on a reduction in the ‘standard revenue’ of a railway company in connection with some extension lines, rendering “provisions for Income Tax and Statutory Charges raised in connection with Extension Lines, no longer required.”

4.3.2 Normative Pillar

The 1923 accounts of the L&LSRC are notable for not only discussing the recent partition of Ireland, and the depressed economic conditions, but also because it is the first time that the company’s steamboat services feature, and the first time that workers’ unions are mentioned: “A scheme has been agreed between the Irish Railway Companies and the representatives of the Railway Workers’ Unions establishing machinery of negotiation for Ireland to deal with the question of wages, conditions of service, and hours of duty.”

The 1923 directors’ report provides a lot of commercial context for the business, especially in relation to the community and region in which it operates:

“Your Directors regret to report that the lack of employment, and the stagnation of trade, resulting from the failure of the Fishing Industry and other causes, the temporary cessation of the migratory labour, together with the aftermath of the unsettled condition of the country in recent years, have resulted in the Company being unable to earn sufficient revenue to pay working expenses. There is at present, however, hope that the economic conditions are likely to improve in the near future.”

and

“In accordance with the sanction given at the same Meeting [the extraordinary meeting on February 28th 1923], the Company are now working the Steamboat Services between Fahan, Rathmullan, and Ramelton, and considering that the services had been in abeyance so long, and the general slackness of trade in this district, the result, in the opinion of your Directors, justifies the taking over of the service.”

Such remarks by the directors are interesting in that reveal a belief that the L&LSRC views itself as not just a railway business, but as a transport business in a wider sense. The attitude of the directors demonstrates commercial foresight. Commercially, the directors’ report for 1925 also includes the first mention of a new technology and source of competition that would prove to be very significant for the wider railway industry: motorised road transport.

“Your Directors regret that, notwithstanding every effort to maintain the Revenue at the highest possible level, a decrease is recorded, due to the enforced reduction in rates, the continued depression in trade, and the effect of increased road transport; this, however, has to a large extent been met by reductions in expenditure. The Company is still, notwithstanding the utmost economy in expenditure, unable to earn sufficient Revenue to meet the present high level of Working Expenses, the Traffic Expenditure for the year 1925 being equal to 117.61 per cent. of Traffic Receipts, as against 69.43 per cent. for 1916, the year immediately preceding Government Control.”

These remarks also demonstrate that the L&LSRC continues to value an economical, lean and agile business model during the period. Again, in 1927, the directors’ report states that:

“Your Directors regret that, notwithstanding every effort to maintain the Revenue at the highest possible level, a decrease is recorded, due to the enforced reduction in rates and fares and the continued depression in trade; this, however, has been more than counteracted by reductions in expenditure.”

1928 is also somewhat of a high-water mark for rail services provided by the L&LSRC, carrying 340,229 passengers (324,061 in 3rd class, 14,116 in 2nd class, and 2,062 in 1st class), running to 299,645 train service miles that year. 1929 is a seminal year for the company: it strategically pivots its business model by embracing road transport (a decision which ultimately enables it to continue trading into the 21st century). The reason for this is clear: in 1929 turnover is £45,482 – 30% below the 1924 peak of £64,467. In the 1929 accounts, 2nd class railway services are no longer mentioned, for the first time, but road transport (omnibus) services are mentioned, also for the first time: “In December last the Omnibus Service formerly operated by Mr. Edward Barr, Buncrana, between Derry, Buncrana, Ballyliffin, etc., was acquired by the Company, and the working results for this short period appear in Account No. 11. During the year Road Motor delivery services for Goods, etc., traffic were established at several Stations to serve outlying districts in the Burtonport and Carndonagh Extension areas.”

L&LSRC now operates three strands of transportation: passenger and freight railway services, passenger and freight road services, and passenger and freight steamboat services.

The strategic pivot is further evidenced in 1930: “The Omnibus Services formerly operated by … have, during the year, been acquired by the Company. The fleet of 'Buses previously owned by the foregoing Proprietors has, for the purpose of the Company’s extended Road Services, been augmented by a number of other 'Buses acquired by the Company.” The 1931 directors’ report describes a re-structuring and a new strategy of moving from being a railway to a road transport business, especially with the curtailment of government funding for railway services:

“The Omnibus Services formerly operated by … have been acquired during the year by the Company. The acquisition of these privately-owned Road Services has enabled the Company to reorganise and consolidate the Road Passenger Services during last Summer, and the working results under this head are detailed in Account No. 11. Following upon a curtailment of Government aid, which has been granted annually since 1924 towards losses on Rail working, a reorganisation Scheme was introduced in April last, the main feature of which was the curtailment of Rail Passenger Services. This step has resulted in a substantial drop in the loss on Railway working, as detailed in Account No. 10.”

By 1931, this strategic pivot finally returns the company to overall ‘gross’ profitability – the profits from road services outdoing the losses from rail services, with turnover becoming almost equal for road and rail in 1931 (see Table 1).

However, in the 1930s the L&LSRC also faced the wider impacts of the ‘Great Depression’ and the Anglo-Irish Trade War (the ‘Economic War’) which resulted in border tariffs. In 1932, “General trade depression and the Tariffs imposed by the Irish Free State and British Governments during the year adversely affected the Traffic Receipts particularly in the latter months of the year compared with the results for the year 1931.” Then in 1933,

“In the early months of the year the Company’s normal rail services were very seriously interrupted in consequence of a withdrawal of labour by certain grades of Railwaymen; this state of affairs, coupled with the general trade depression, particularly in the Agricultural Markets, has resulted in a very heavy reduction in the Company’s Gross Revenue from Railway Working for the year 1933 compared with 1932. Receipts from Road Passenger Services, however, showed an appreciable increase, due mainly to increased Tourist and Summer Excursion Traffic. Two new Leyland Tiber Coaches were placed in service during the year.”

In 1935,

“The substantial increase in the Gross Receipts from Road Transport recorded above follows upon the acquisition by the Company under the terms of the Irish Free State Road Transport Act (1933) of a large number of merchandise services hitherto operated by licensed carriers in this Company’s area. During the year the Road Passenger Services were extended to include Rathmullan. The Rail Service on the Buncrana–Carndonagh Extension, which in recent years has shown a heavy loss in working, was withdrawn on 2nd December last, alternative services being provided by Road for both passengers and goods.”

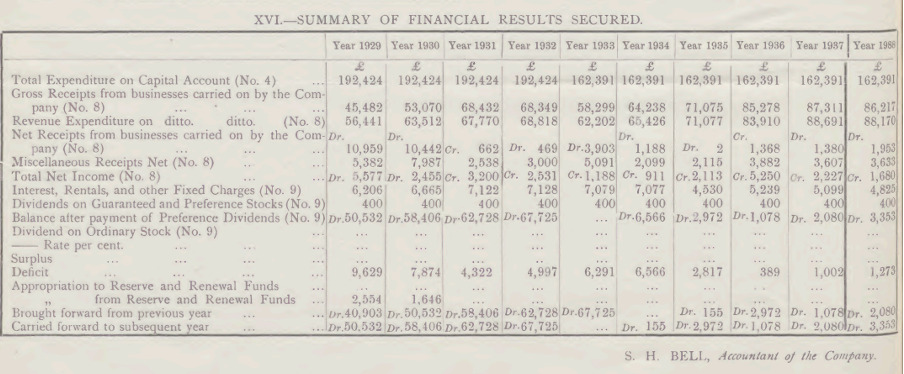

Then in 1938, “One 36-seater Leyland Diesel Omnibus of the latest type, Two Mail Vans, and Six Motor Lorries were placed in service during the year”, and the 1938 accounts illustrate the impact of L&LSRC evolving into more a road transportation company (see Figure 9).

4.3.3 Cultural-Cognitive Pillar

The annual reports of this period (1921–1939) further reveal how the company views itself as being embedded in the community of the region. The company has directors of unionist and nationalist backgrounds, and its business relies on people from these backgrounds on both sides of the border using its freight and passenger services. The evidence also challenges the perception that there was no communication between politicians from the two jurisdictions on the island before 1967. For example, Sir Basil McFarland (of Aberfoyle House, now part of Ulster University’s Derry–Londonderry (Magee) campus) who was a prominent unionist politician and figurehead in Londonderry, and Senator Patrick McLaughlin of Cumann na nGaedheal / Fine Gael in Fahan, County Donegal, were members of the board of directors together from the 1920s to the 1940s. This shows that, while there was little ‘official’ communication between the two governments, there is evidence of ‘unofficial’ communication.

Related to this, the L&LSRC accounts also provide evidence to challenge the perception that there was no cooperation between the two governments on the island of Ireland in this period, as both governments simultaneously provided grant funding to the company for its cross-border services from the 1920s to 1939. For instance, in 1926, both governments are mentioned in the directors’ report:

“After including the sum of £5,500, Grant in Aid received from the Government of Northern Ireland, and appropriating £1,700 from the Company’s share of the Compensation received under the Irish Railways (Settlement of Claims) Act, 1921, and providing for interest on Mortgages, Debenture, and County Guaranteed Stocks, and other fixed charges, a Debit Balance of £25,084 remains. The Irish Free State Government has granted financial assistance to the extent of £5,333 towards the loss on working the Letterkenny, Carndonagh, and Burtonport Extensions during the year.”

And in 1934,

“The balance of the Irish Free State Government Grant towards loss on Railway working for the year 1933 paid during 1934 amounting to £1,639 has been included in the General Balance Sheet Account No. 18. A similar amount from the Government of Northern Ireland is included in Account No. 8.”

The 1939 annual accounts, prepared in early 1940, surprisingly make no reference to World War II, given that Lough Foyle/Derry city would become the main Allied naval base for the North Atlantic, except for the following indirect reference: “Owing to absence abroad Capt. Sir Basil McFarland, Bt., H.M.L., temporarily relinquished his seat on the Board”. Possibly also due to the outbreak of World War II, the grant aid from both the ‘Government of Northern Ireland’ and ‘Government of Éire’ ceases entirely in 1939.

4.4 1940–1947: From World War II to the Closure of the Railway Services and the End of Availability of Annual Accounts

4.4.1 Regulative Pillar

In 1940, there is again no reference to World War II, except an indirect one as per Figure 10, whereby a security measure preventing the publication of maps was implemented during the war. It is noteworthy that the format and detail of the accounts during the World War II period does not change. For example, while the accounts were abbreviated during World War I and caveats applied to certifications, in 1941 the only indirect reference to World War II is a ‘temporary emergency measure’: “The Letterkenny Burtonport Extension, which was closed for all traffic in June, 1940, under the provisions of the Railways Act, 1933, was re-opened for Goods Transport in January, 1941, between Letterkenny and Gweedore as a temporary emergency measure.”

Interestingly however, the war is actually “good for business” as turnover increases substantially in 1941 (see Table 1 above). In 1942, for the first time since 1923 the dividend on the ordinary shares resumes: “From this balance the Directors recommend a Dividend of 5% on the Preference Stock and 1% on the Ordinary Stock, less Income Tax, which together require a sum of £2,984, leaving a balance of £1,046 to be carried forward to next year’s Accounts.”

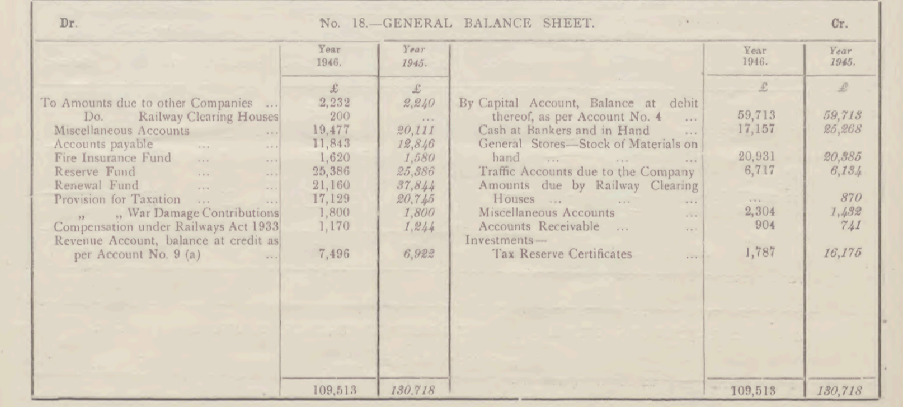

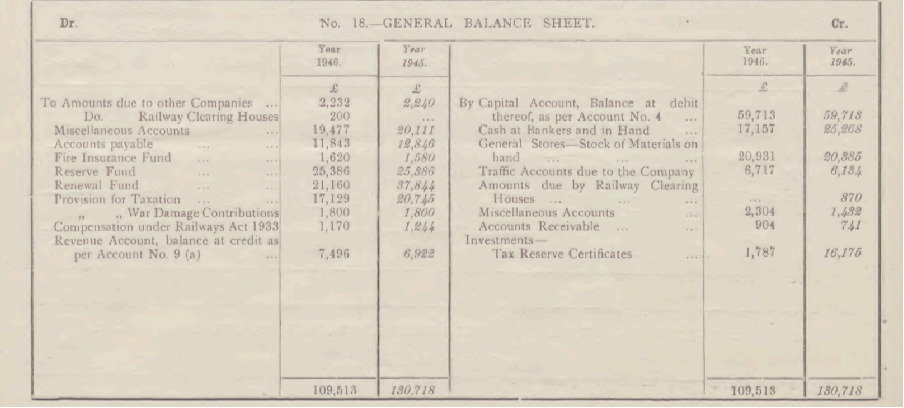

In 1946, the dividend on ordinary shares increases to 5%. The only reference to World War II is a line for ‘Provision for war damage contributions’ in the balance sheet (see Figure 11).

The final year of available accounts is 1947 (still being audited by Stokes Bros. & Pim, Chartered Accountants). Their format is remarkably consistent with the company’s accounts since 1914. The annual general meeting (AGM) is on 26 February 1948: the company has also been remarkably consistent, since 1884, in holding its AGM within two months of the year-end.

4.4.2 Normative Pillar

In 1940, rail services are 23% of turnover and continue to be phased out:

“The Rail Service on the Letterkenny Burtonport Extension, which in recent years has shown a heavy loss in Working, was, under the provisions of the Railways Act, 1933, withdrawn on 2nd June last, alternative services being provided by Road for both passengers and goods. One 3.2-seater Diesel Omnibus and 15 Motor Lorries were purchased, and 2 petrol engined Omnibuses were converted and fitted with Diesel engines during the year, and the cost of these charged to the appropriate Renewal Fund.”

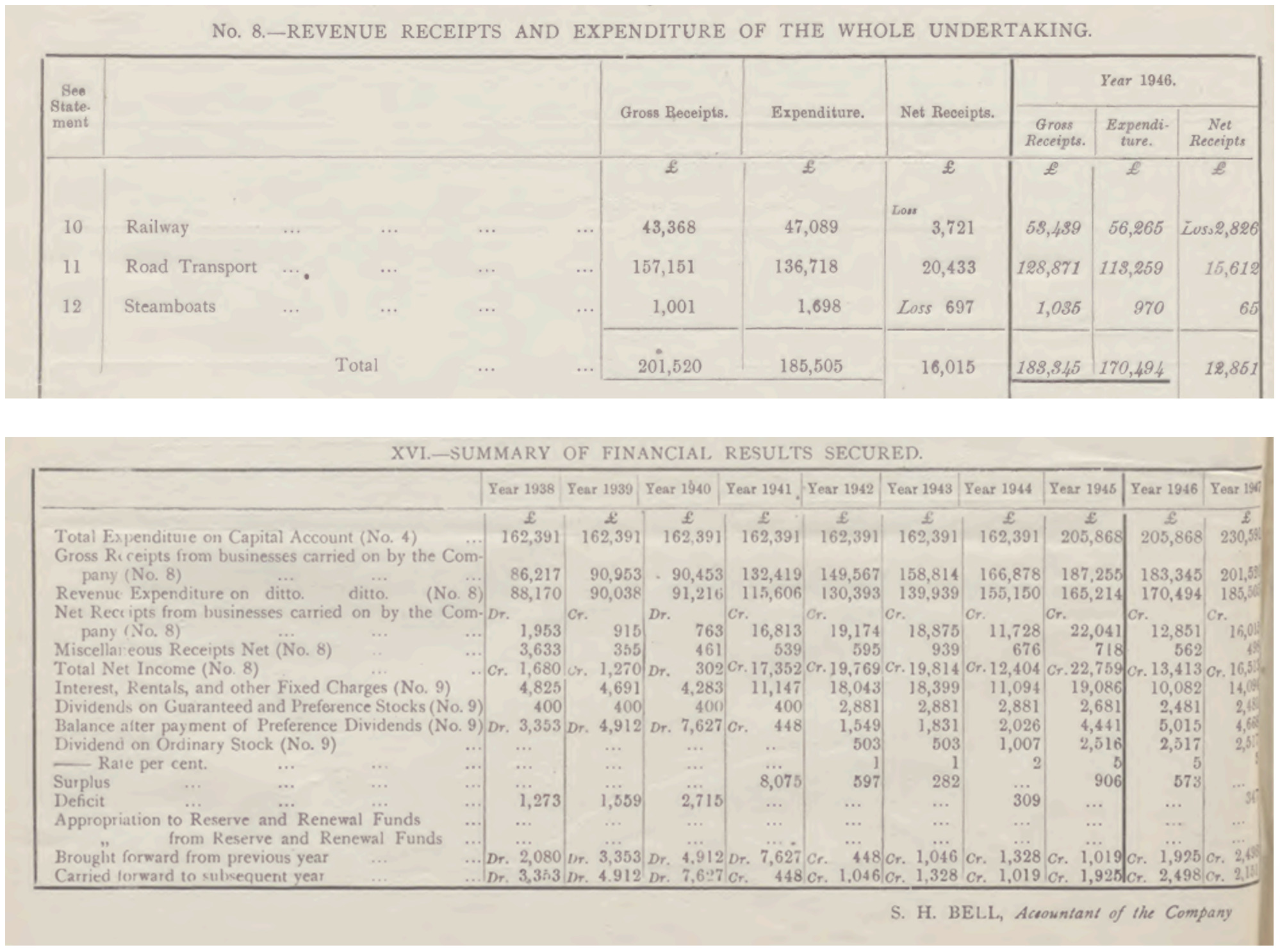

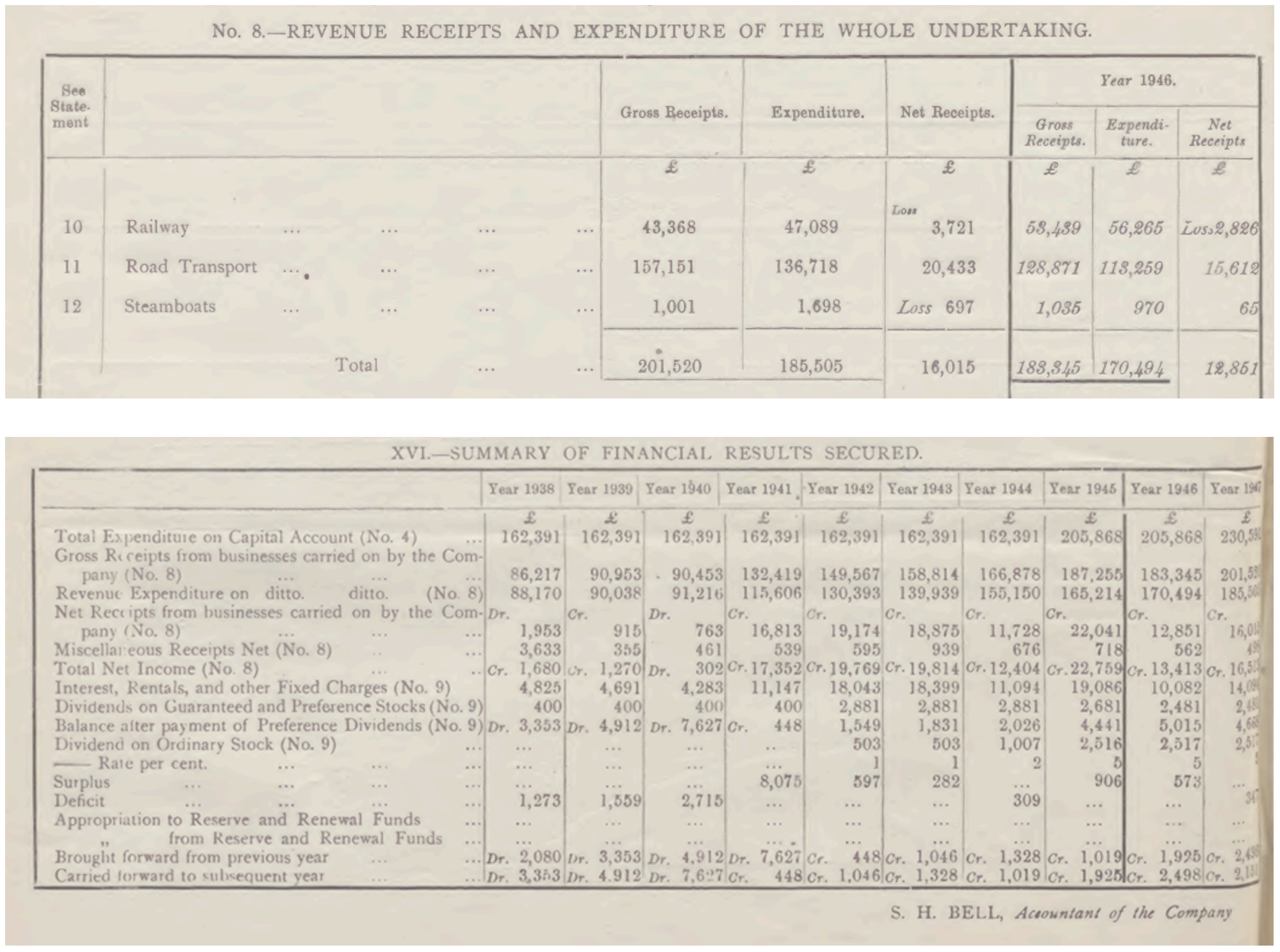

The company is becoming more profitable from road services in the 1940s (see Table 1 above). By 1947, business is clearly dominated by road services (both in turnover and in profits), and the L&LSRC only records 113,585 in train service mileage. The success of the strategic pivot from a rail business to a road transport business, and the boost to business during World War II, is clear from the 1947 accounts (see Figure 12).

The board of directors continues to demonstrate an economical approach to costs during this period, including their own remuneration. In 1940, the directors’ fees are £63 (up from £61 in 1939), but down from £350 in 1916.

4.4.3 Cultural-Cognitive Pillar

In 1945, the accounts note: “It is with deep regret that your Directors record the death on 3rd November last of Mr. I. J. Trew Colquhoun, who had been a member of the Board from 1913, and Chairman since 1924.” In terms of modern corporate governance, it would no longer be considered best practice to have an individual serve as a board member for 32 years and chairman for 21 years. However, as many people served multiple terms on the board of directors of the L&LSRC, such continuity allowed for the sharing of information, knowledge, and values, providing these individuals with an understanding of the institution and its purpose.

4.5 Neo-institutionalist Theory and Comparisons with Prior Literature

“The organisation of railways has long been regarded as an exemplar of managerial hierarchy, and a precursor to the emergence of the modern corporation” (R. Edwards, 2013, p. 479). Railway companies were the first entities to deal with complex issues of control, communication and decision-making, as well as new ways of working (R. Edwards, 2013). Despite this, the performance of the UK’s railways during the period c.1900–1947 has been largely viewed as poor, with historians critical of railway management’s inability to react to changing conditions, being too conservative with their investment policies, as well as a failure to calculate costs (R. Edwards, 2010). However, Edwards (2010) also states there are few archival-based studies to test these criticisms. The findings of this research into the L&LSRC annual reports from 1884 to 1947 challenges some of these widely held views, as the L&LSRC displays ‘lean and agile’ characteristics that ensured it continued in business until 2014.

Somewhat related, Edwards (2013, p. 479) also notes that “the inevitability of the railway as a large, centralised entity has been questioned in Gerald Berk’s study of American railway organisation in the late nineteenth and early twentieth century. He concludes that there was a ‘path not taken’ where smaller regional and local associations were possible, embedded in the local economy.” The L&LSRC is an interesting example (from Ireland) of a where smaller regional railway company, embedded in the local economy, continued in business until 2014, albeit by morphing from a railway company into a road transport company.

The annual reports of the L&LSRC highlight six key external challenges that particularly impacted on the company between 1884 and 1947. Of these six external challenges, three are related to geopolitical conflicts, one is economic in nature, one is technological, and one is regulatory. The first challenge is from the Railway Companies (Accounts and Returns) Act 1911, which standardised the presentation and regulation of annual accounts for railway companies in the UK (and Ireland) in terms of financial information and non-financial information. The second is World War I from 1914 (and within that the Irish War of Independence from 1916), which the company found very damaging commercially. The third is the partition of Ireland in 1921, as the company now operated across a newly created international border, with its main railway depot and headquarters in the port city of Derry/Londonderry only two miles from the border and the rest of its services in the new Irish Free State. The fourth is the advent and increasing use of motorised road transport, in particular competition from lorries and buses from the 1920s onwards, which directly usurped the usefulness of railways. The fifth is the global economic depression of the 1930s (and within that the prolonged Anglo-Irish Trade War from 1932). The sixth is World War II, from which, in contrast to World War I, the company benefitted commercially.

The L&LSRC is an outlier by continuing in business as an independent company until 2014, which is even more surprising given the challenges described in this paper, and as it operated in the most economically deprived and geographically peripheral region of the UK and Ireland (Central Statistics Office, 2021; MySociety, 2020). Scott’s (2014) three pillars, which are interconnected and work together, help frame our understanding of the findings from the annual reports from 1884 to 1947. A key advantage of neo-institutionalism is that it does not limit change to external pressures but acknowledges the agency of organisations and individuals. It allows organisations to respond strategically to these external pressures. While institutions provide stability and order (e.g., accounting systems), they also undergo transition, both incremental and revolutionary (Hwang, 2023).

In terms of the regulative pillar (Scott, 2014), railways were a very regulated industry. The L&LSRC was established by an Act of Parliament; health and safety standards are certified each year; detailed accounts are required and specified by the Railway Companies (Accounts and Returns) Act 1911; timely, accurate and audited annual accounts are published throughout the period; and its operations and accounts adhere to commendable corporate governance processes. The development of new large-scale infrastructure, such as new railway lines, is also governed by a new Act of Parliament for each one, which allows each project to be delivered, in contrast to the process for large-scale infrastructure development in Ireland today.

In terms of the normative pillar (Scott, 2014), the company operates in a ‘lean and agile’ manner. This is evident during periods of commercial downturns, such as when directors’ remuneration is cut. However, it is most evident where, rather than trying to compete against the new existential threat of motor vehicles (lorries and busses), the company instead choses to embrace and invest in this new opportunity and gradually morphs into a fully road-transport business model.

In terms of the cultural-cognitive pillar (Scott, 2014), the annual reports show that the company is embedded in the community in a mutually reliant way. The board of directors is also ‘cross-community’ (unionist/nationalist) in nature, and this helps the company survive several turbulent periods in the early 20th century, with the surprising and unexpected support of not only the unionist and nationalist communities on both sides of the new border, but also the two governments on the island. The conventional wisdom is that there was no co-operation, and even hostility, between these two communities and governments in the early 20th century.

The combination of these three pillars working together enables the company to survive longer than its peers, and in so doing helps build on Edwards’s (2010) call for more archival-based studies to test (and challenge) the widely-held criticisms of UK railway companies in the early 20th century, as well as building on Berk’s (1997) assertion that smaller regional and local operators embedded in the local economy were possible.

Lee and Saunders (2017) consider researching such outlier cases to be a valuable means of adding to our knowledge and understanding. That the L&LSRC is an outlier is a limitation of this study, but conversely it provides additional insights. Why did the L&LSRC outlast its peers and continue trading until 2014? The key reason, beyond all other factors, is its embrace of road transport rather than competing with it. The L&LSRC adapted to changes in the external institutional environment to become a ‘passenger and freight transport business’ rather than just a ‘railway business’, despite the company name not changing. What explains why it adapted and embraced road transport? The normative pillar is built upon collective values and norms, acting as guiding principles and defining appropriate conduct and influencing how individuals and groups pursue their goals. A recurring theme of its annual reports from 1884 to 1947 is that the L&LSRC is run in a lean and agile manner, and this enables it to take advantage of road transport rather than being defeated by it. In essence, change provides stability for the company.

There are many examples of the speed of advances in technology and society overtaking the corresponding response by companies, such as canals being replaced by railways, and in the 21st century high street retailers being replaced by e-commerce, as well as the advent of artificial intelligence creating new disruptions to business models. Oliver (1991) identifies predictors of organisational change, referred to as the ‘Five Cs’, These explain an organisation’s response to institutional pressure: cause, constituents, contents, control, and context. The ‘context’ refers to the environment within which institutional pressures are exerted. The environment changes and institutions may either respond, endure, and flourish or be weakened and give way to new ones, creating a process of deinstitutionalisation (Oliver, 1992). As we recently marked the 200th anniversary of the railways in 2025, the normative pillar can especially help us understand why some companies in our ever-changing world survive by choosing to embrace innovation, and how organisational change and adaptation in the face of changes in the external institutional environment can conversely provide more stability for an organisation.

5. Concluding Remarks

The exploration of the accounts for the L&LSRC from 1884 to 1947 provides interesting insights into commercial priorities, accounting practices, and corporate governance processes during this time, and into social, economic, and political issues of this period. In modern terms, the L&LSRC could be considered a ‘lean and agile’ business. There is a strong focus on cost control in various directors’ reports (e.g., in 1924 “met by reductions in expenditure … the utmost economy in expenditure”). Importantly, the company is successful in strategically pivoting from being a railway company to becoming a road-transport business during periods of great change and turmoil in its external institutional environment, between World War I, the partition of Ireland, new technological advances, the economic depression of the 1930s, and World War II. In contrast to the company’s experience of World War I and the Irish War of Independence, business boomed for the L&LSRC during World War II. The company also benefitted from the unusual support of both the Irish Free State Government and the Government of Northern Ireland, and of the unionist and nationalist communities on both sides of the new border. Ultimately, the L&LSRC continued in business until 2014 as the oldest railway company established in the Victorian era to continue trading as a commercial concern. Notably, County Donegal, in the northwest of Ireland, has not had any railway services since the 1950s.

The company displays surprisingly commendable corporate governance processes during the late 1800s, such as the rotation of directors on the board, resolutions requiring approval at shareholders’ meetings, and the external auditing of very detailed accounts. A major change in the presentation of the accounts is prescribed by the Railway Companies (Accounts and Returns) Act 1911. The 1914 accounts (including the statistical returns) are 21 pages in length and remarkably sophisticated for what one would expect of accounts from the time.

One of the main limitations of this study is that it focuses on only one company. Exploratory research such as this faces challenges related to limited generalisability, arising primarily from its qualitative nature and smaller sample size, and thus findings may not be representative of broader sample populations or diverse contexts. It is also more challenging to gain insights from the cultural-cognitive pillar of New Institutional Sociology, as one must rely on secondary sources when performing accounting history research. With a study of archival documents it can be challenging to gather rich data specifically for the cultural-cognitive pillar due to the inherent limitation that elements of the cultural-cognitive pillar can be largely implicit rather than explicitly documented in archives, including the tacit knowledge of people at the time, the selection bias of only including the perspectives of the people involved in the annual reports, and the subjectivity of interpretation and inference from historical documents by the researcher. The cultural-cognitive pillar could potentially be incorporated more into future research by other research methods and archival materials (e.g., personal records of directors, correspondence, archival interviews, and media articles about directors, workers and people who used the company’s services), or by expanding the research design to include more railway companies and therefore more annual reports. However, another limitation is the availability of digitised or searchable records in relation to the L&LSRC. Although additional publicly available records were searched and reviewed, for example parliamentary debates in Ireland and the UK, it was limited in volume. Any extant internal records of the company are stored by the Public Records Office of Northern Ireland under the D2683 archive; however, none of it is digitised. While it is beyond the scope of the design of this research, such future research could enhance further understanding of information in the annual reports and corresponding theoretical explanations.

The railway companies of Ireland provide a potentially rich source of material for accounting history researchers, especially as their financial statements are easily accessible. There were many independent railway companies throughout Ireland, such as the West Clare Railway made famous by the Percy French song and court case. The Secretary’s Office of the Great Southern & Western Railway collated a book, Reports of Irish Railways, twice a year of the half-yearly accounts for 28 railway companies in Ireland from the late 1800s. Future research could explore more of these companies from an accounting history perspective, especially to draw similarities and points of divergence and enable more generalisability, among companies in Ireland, but also between Irish companies and those in Britain and elsewhere for the same period. Such research could also be designed to apply alternative theoretical perspectives/concepts, for example concepts such as rules and routines (Burns & Scapens, 2000) to establish if routinised accounting practices were common across the railway industry to enrich our understanding, as this paper has studied only one company. A research design that takes a case study-based approach, examining the annual reports as text, for one or more of the 28 railway companies that were collated, could also be an interesting avenue for future researchers. Furthermore, future research could also examine additional extant archival records that may exist for these 28 railway companies; for example, internal records that were not published, such as the minutes of board of directors’ meetings.

This paper makes several contributions to knowledge. Firstly, it is the first accounting history research on railway companies in an Irish context. Secondly, it highlights how the normative aspect is the dominant institutional factor in helping us understand how adapting to technological changes in the external institutional environment conversely provides stability for a company.