1. Introduction

In the multifaceted and volatile landscape of contemporary finance, accurate valuation of assets is a key challenge. Amid the global financial configuration, valuation serves as a guiding compass to the complex terrain of financial decision-making. Far from definitive, it is regarded as a synthesis of both art and science that calls for quantitative rigor and an analyst’s subjective judgment and contextual understanding (Brown, 1998). This rebuts the long-held assumption of a singular intrinsic value in corporate finance. Analysts employ diverse methodologies contingent upon the objective and prevailing context. Common approaches include residual income, net asset value, discounted cash flow, and relative valuation (Lukanima, 2023; Reilly & Schweihs, 1999). Diverse methodologies may produce differing estimated values, owing to their distinctive perspectives and foundational assumptions. While valuation theory encompasses diverse paradigms from intrinsic value estimation to derivative-based frameworks, this study delimits its scope to relative valuation commonly termed valuation or market multiples. Multiples are a staple in equity analysts’ reports, investment bankers’ fairness opinions, and a multitude of corporate transactions, such as mergers and acquisitions (M&A), initial public offers (IPOs), and spinoffs (Demirakos et al., 2004; Fabozzi et al., 2017; Yu & Tan, 2018). Even sophisticated valuation techniques incorporate multiples, either to estimate a terminal value or to corroborate results. Their wider applicability is grounded in the assumption that market prices predominantly exhibit equitable reflections of intrinsic value. The inherent flexibility of valuation multiples allows analysts to adapt their framework to evolving market conditions, even when speculative bubbles and transient market disruptions violate the equilibrium.

In accordance with the “law of one price”, the foundation for the application of valuation multiples, comparable assets should trade at a similar valuation level in an efficient market (Fama, 1970). Following this premise, this valuation multiples approach has two facets: first, prices must be standardised by expressing them as multiples of a common value driver, such as earnings, book value, or revenue. Second, the identification of comparable assets poses a challenge since no two assets are precisely identical (Damodaran, 2016). Consequently, scholarly work on valuation multiples falls into two broad classifications. The first set of academic research focuses on finding suitable peers for comparison (Alford, 1992; Benninga & Sarig, 1997; Bhojraj, Lee, & Ng, 2003; Bhojraj, Lee, & Oler, 2003; Boatsman & Baskin, 1981; Cooper & Lambertides, 2023; Penman, 2013). The second set of scholars has researched valuation multiples and their drivers (Chastenet & Marion, 2015; Harbula, 2009; Keun Yoo, 2006; Liu et al., 2002; Yooyanyong et al., 2019). In addition, valuation multiples fall into two distinct sets: enterprise and equity value multiples (Damodaran, 2016; Lukanima, 2023).

Owing to both practical significance and theoretical appeal, academicians have extensively studied and researched the area. That resulted in a substantial and growing body of literature. Building on this foundation, scholars have conducted a few reviews to synthesise key findings. In a number of recent review studies, the research area has been viewed from particular angles (Table 1). Pätäri and Leivo (2017) focused on the value anomaly by categorising the studies on the basis of multiple employees. On the other hand, Shaffer (2024) reviewed studies that highlight the valuation multiples considered in the M&A advisory. In a more recent study, Olbert (2024b) explored the preferred valuation model in determining a stock’s target price within 25 Global Industry Classification Standard (GICS) industry groups. In another study, Olbert (2024a) attempted to comprehend what is referred to as the “black box” of valuation. This study shed light on what valuation tools are employed by analysts across diverse industries and concluded price-to-earnings (P/E) ratio as the most favoured model. In contrast to previous reviews, which intended to emphasise the specific domains related to the market multiples, the scope of our study is to present a holistic overview of their multifaceted role in financial decision-making.

This study adds to the growing body of literature on market multiples by synthesising existing research and situating it within a broader context, offering three key contributions. First, despite the widespread use of comparable company analysis, no comprehensive review has examined its literature in its entirety. Second, the study adopts a systematic review methodology supported by two bibliometric techniques (Donthu et al., 2021; Kraus et al., 2022; Lim et al., 2022; Mukherjee et al., 2022a): one, performance analysis, which evaluates the publication trends and identifies key contributors; two, science mapping, which visually represents the intellectual framework of the domain. These tools offer a quantitative lens to identify thematic linkages and coherence among the reviewed studies (Blanco-Mesa et al., 2017; Li et al., 2017). Third, this study highlights the applicability of valuation multiples across diverse stakeholder groups within the financial ecosystem. For analysts, investors, corporate executives, and regulators, it summarises how valuation multiples are applied across contexts. Through their identification of research gaps and scope for further studies, this advances the agenda of both academics and practitioners in the field of valuation research.

The study is organised in the following manner: Section 2 outlines the methodological approach. Section 3 evaluates the results of the performance assessment, and Section 4 analyses the findings of scientific mapping. Section 5 discusses the key takeaways from the analysis and potential needs for future academic research, and the paper concludes with Section 6.

2. Review Methods and Sample Selection

2.1 Identifying Relevant Articles

The study performs a Systematic Literature Review (SLR) to trace the theoretical evolution of the studies on valuation multiples (Booth et al., 2016). In contrast to conventional narrative reviews that often rely on the subjective judgment of the researcher (Denyer & Tranfield, 2006), SLR provides a structured, transparent, and rule-based methodology. Thus, the synthesis from this approach enhances comprehensiveness and minimises potential biases (Booth et al., 2016; Dumay, 2014; Guthrie et al., 2012; Guthrie & Murthy, 2009; Guthrie & Parker, 2012; Massaro et al., 2016; Tranfield et al., 2003). The study adheres to the three-stage paradigm proposed by Tranfield et al. (2003); the review proceeds through sequential phases, which are planning the review, conducting the review, and reporting and dissemination.

Stage 1 – planning the review includes outlining the study’s motivation and scope.

Building on the previous section, the study attempts to provide an overview of the development of academic research on valuation multiples, emphasising their wide range of applications in investment and financial decision-making (Massaro et al., 2016). To define the scope of the study, the following three core research questions are posed:

What are the temporal trends and who are the influential contributors in the valuation multiples literature?

What are the primary research themes and intellectual clusters in the valuation multiples literature?

What are the significant research gaps in the valuation multiples literature, and what future research directions would advance the field?

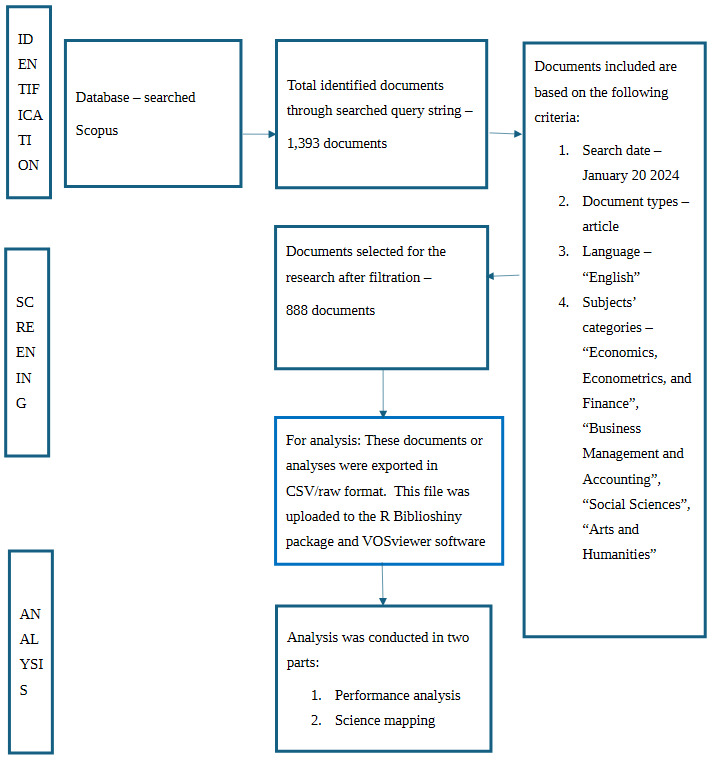

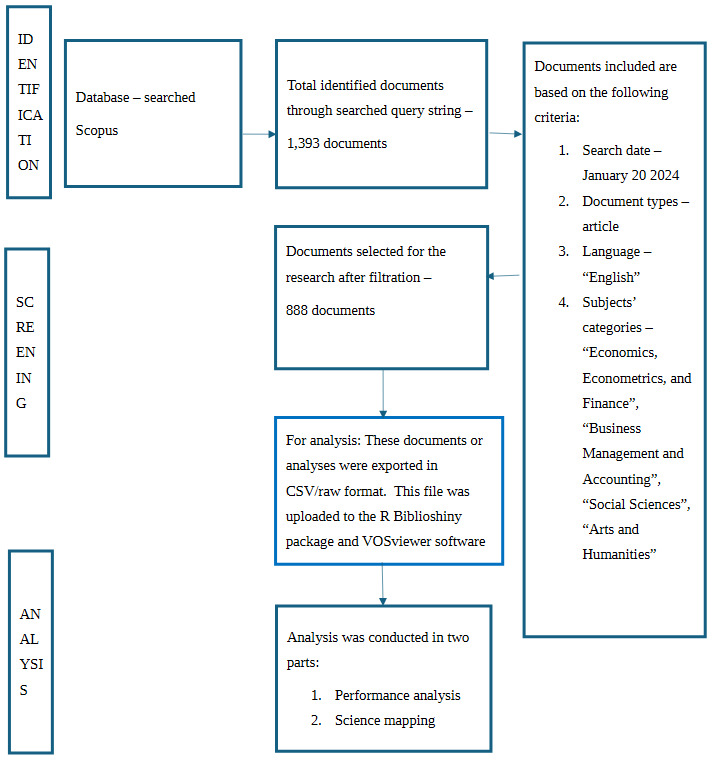

Stage 2 – conducting the review entails the identification, selection, and quality review of the corpus. The study utilises the Scopus database for the search of pertinent corpus at the beginning of November 2024. The decision to use Scopus was driven by its recognition as one of the most comprehensive and sizable multidisciplinary databases in economics and business (Bar-Ilan, 2010; Bartol et al., 2014; Norris & Oppenheim, 2007; Vieira & Gomes, 2009). Although Google Scholar may generate more information, evaluating the quality of data poses more challenges. Therefore, Scopus is a more prudent alternative for this bibliometric study (Corbet et al., 2019; Franceschet, 2010).

The query string used is outlined in Table 2. The string was developed on Kraus et al.'s (2022) three E’s: “expertise, experience, and exposure”. The overall search and screening strategy (Kraus et al., 2022; Paul et al., 2021) is illustrated in Figure 1.

Stage 3 – reporting and dissemination concentrates on communicating the results and formulating practical recommendations along with implications.

2.2 Bibliometric Analysis

Meta-analysis and bibliometric analysis are two major quantitative techniques for analysing the results of an SLR. Meta-analysis is a statistical approach that involves meticulously analysing data to summarise and validate previous study findings (Knoll & Matthes, 2017; Ladeira et al., 2023; Paul & Barari, 2022). By examining key themes in a specific field, scientometric analysis, commonly referred to as bibliometric analysis, is a method used to evaluate the production and impact of research (Mukherjee et al., 2022b; Randhawa et al., 2016; Zupic & Čater, 2014). The VOSviewer and Biblioshiny tools from the R package software facilitated the extensive network mapping of the refined dataset, enabling effective data visualisation and close alignment with filtered parameters (Ingale & Paluri, 2022; Srivastava & Anand, 2024; Vijay Kumar & Senthil Kumar, 2023; Yadav & Banerji, 2023).

Table 3 presents a detailed enumeration of the analytical scheme or methodology employed in the current study.

3. Performance Analysis

3.1 Characterisation and Evolution of Research Landscape

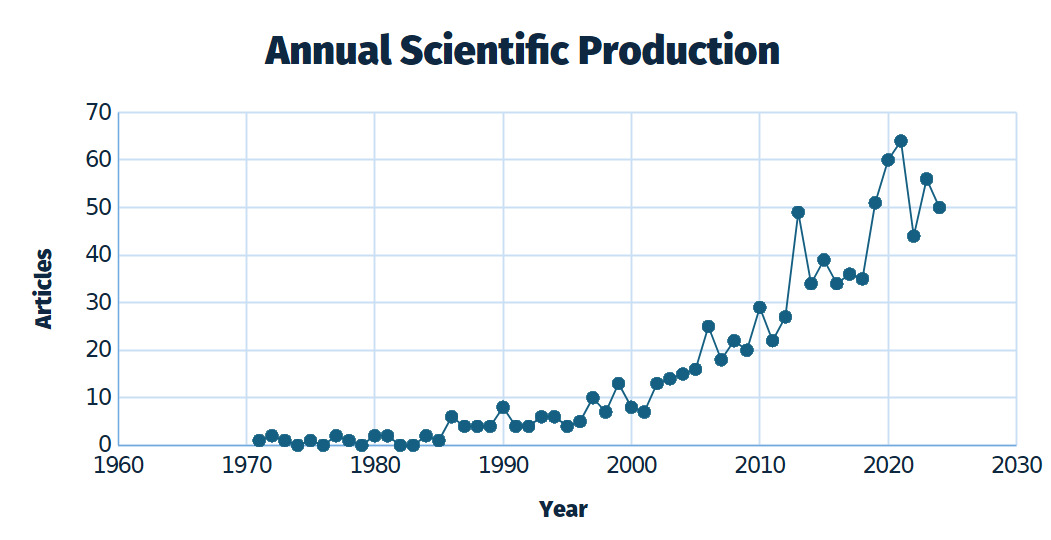

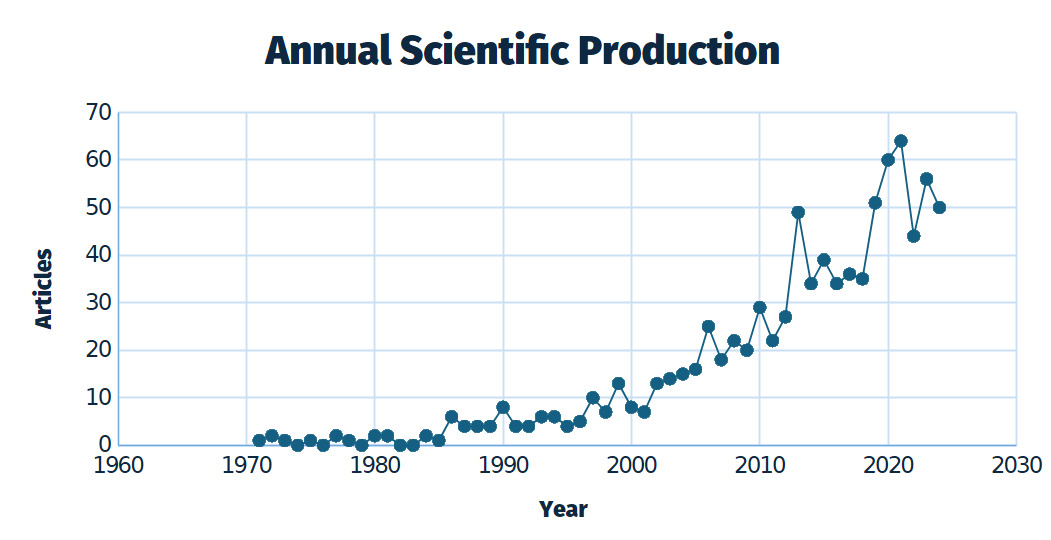

Decadal variations in scientific production in scientific publications reveal noteworthy patterns in academic research. Scholars began developing notions on the fair value of common stocks as early as the 1930s, after the Great Depression started with the stock market collapse. However, academic interest began to gain momentum in the 1970s. As illustrated in Figures 2 and 3, 888 articles were published in more than 50 journals between 1970 and 2024. Out of the total articles, a relatively small percentage (11.26%) was published between 1970 and 2000, and approximately 21.05% between 2000 and 2010, signalling a gradual rise in research interest. The past decade has seen a significant surge in publications, accounting for nearly 67% of the total output, depicting an increase in interest in the research field, emerging modern financial problems, and evolving decision-making frameworks. Research in the discipline is still showing an upward trend, even when the analysts are emphasising multimodal valuation frameworks. The rationale is that analysts persist in prioritising the P/E ratio over other models.

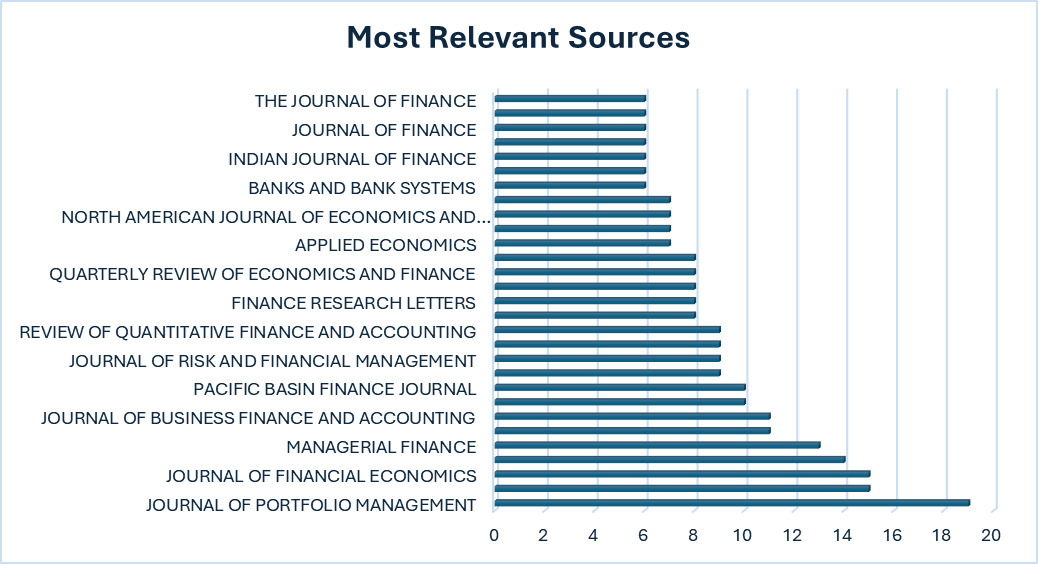

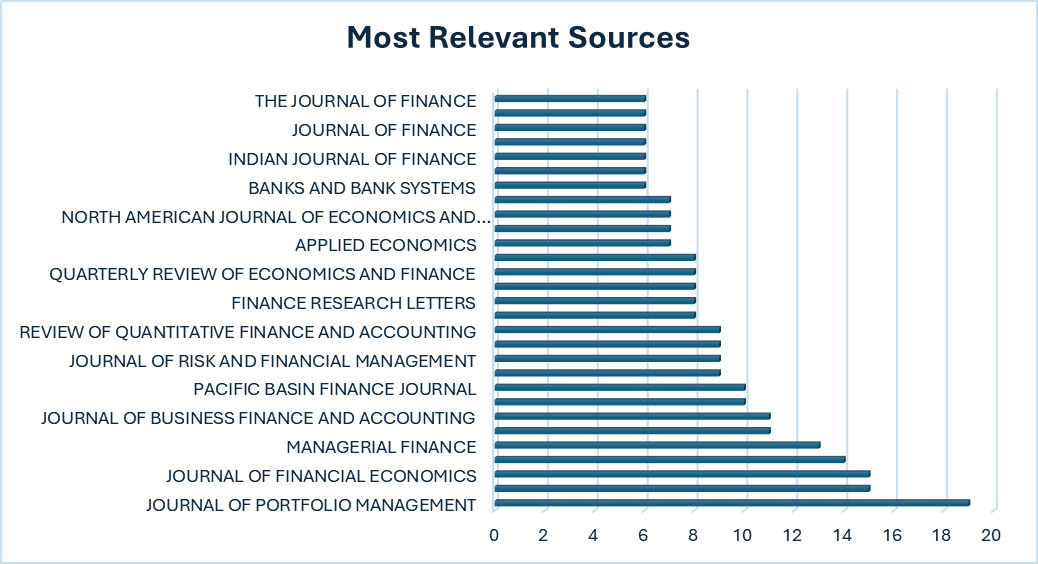

Among the wide range of academic journals that provide an assessment of valuation multiples – into three prominent categories: economics, finance, and accounting – the most prolific journals include the Journal of Portfolio Management, Journal of Finance, Journal of Financial Economics and Review of Quantitative Finance and Accounting. The field is acknowledged in highly qualified business and management research publication journals. Many of these are rated A*, A or B by the Australian Business Deans Council (ABDC) and hold strong rankings from the Chartered Association of Business Schools (CABS).

3.2 Keyword Analysis

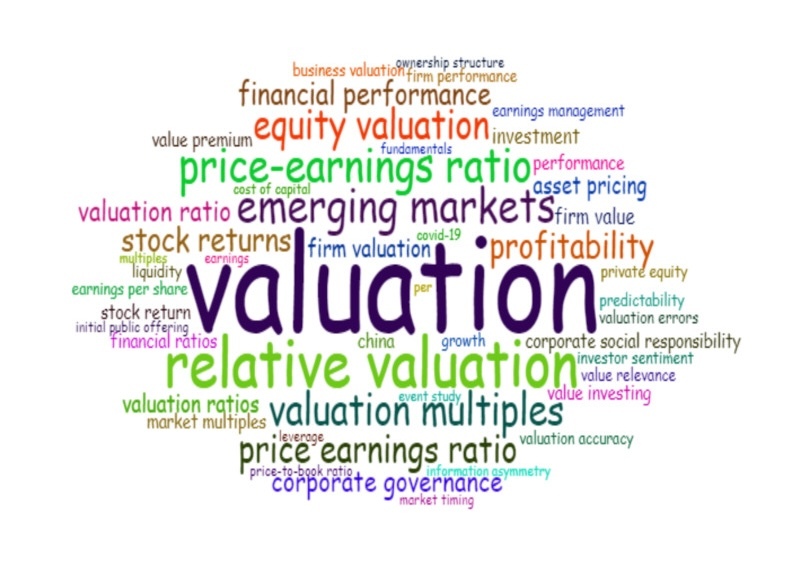

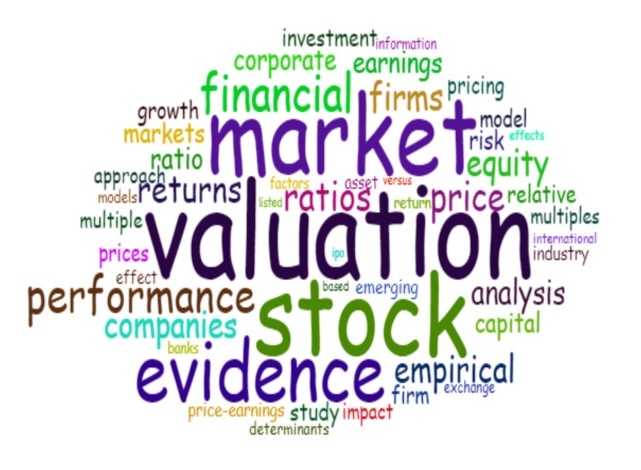

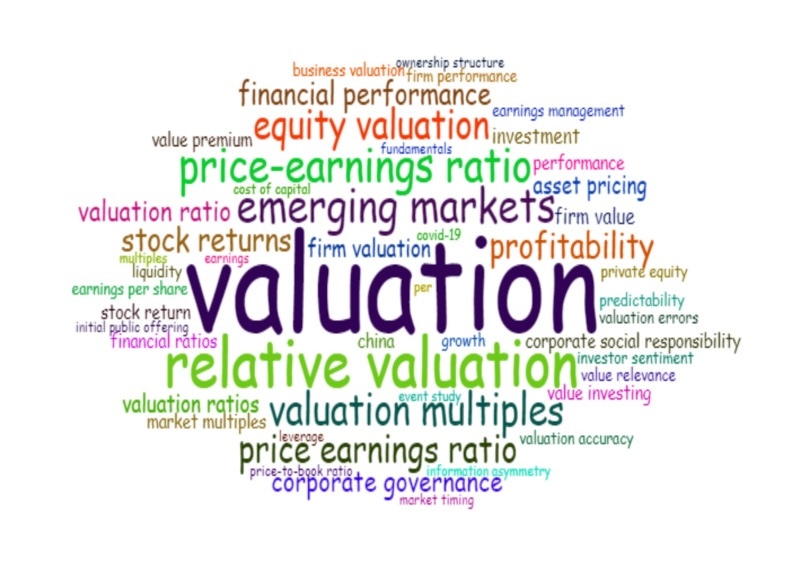

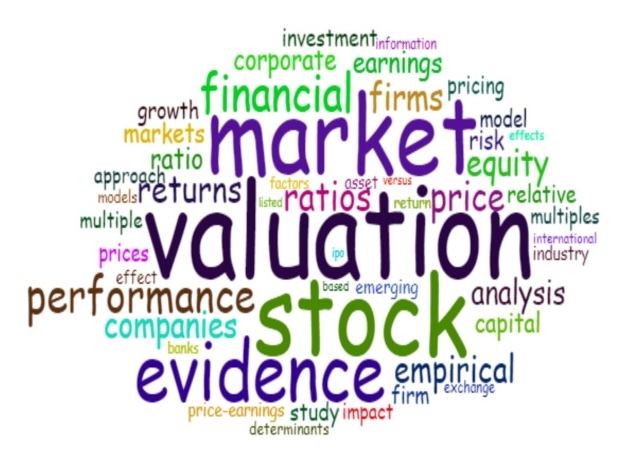

This section offers a detailed perspective on the frequently used authors’ terms. This provides a nuanced view of the key terms, trends and areas of focus in the academic body of literature. Additionally, the “keyword plus” is derived from the article’s titles, providing an additional layer of context by highlighting broader associations and related topics (see Table 4).

Moreover, the word clouds in Figures 4 and 5 visually represent textual data, with the size and prominence of each term reflecting its frequency and significance within the dataset.

3.3 Countries’ Academic Contribution

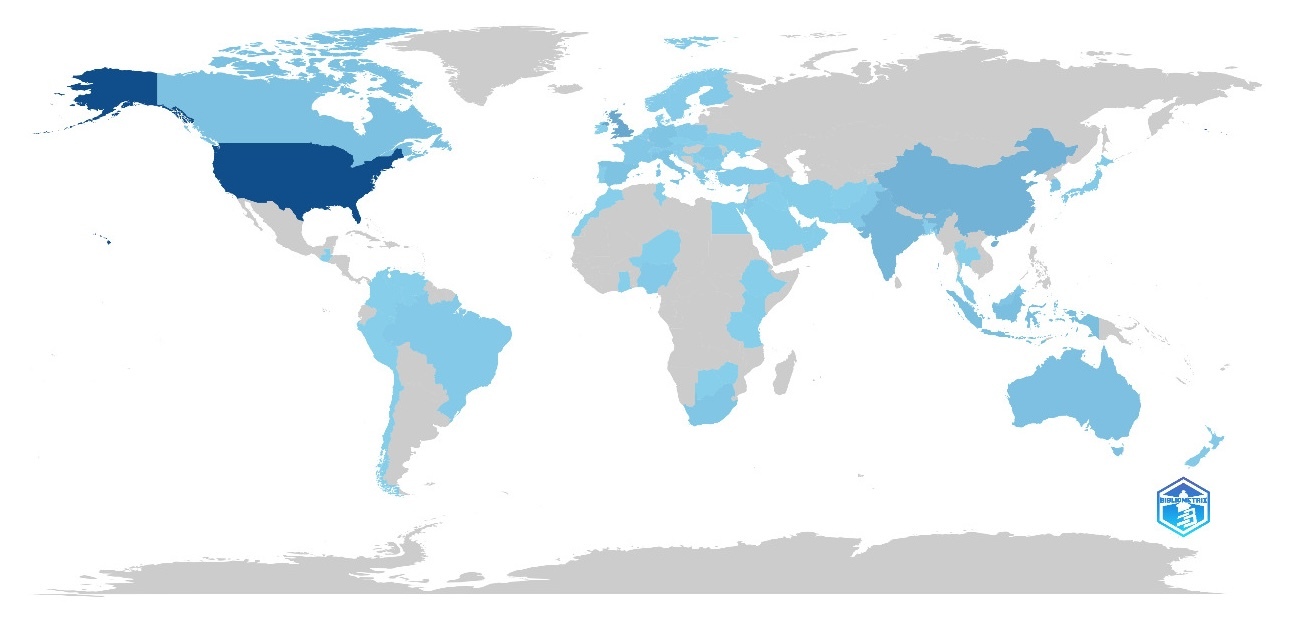

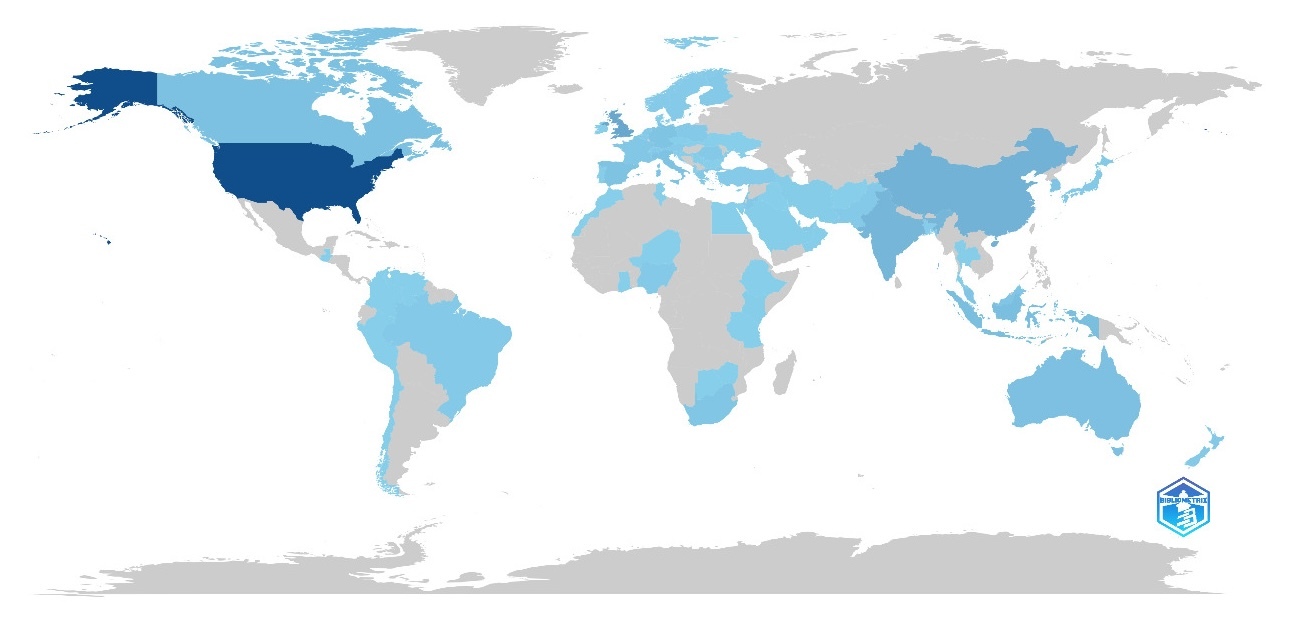

Figure 6 highlights the geographic distribution of academic research in valuation multiples. The United States leads in publishing volume. Western Europe emerges as a significant hub with nations such as the UK, Ireland, and France making considerable contributions. This underscores Europe’s sustained interest in the areas of finance, accounting and specifically valuation research. The map illustrates a heightened scholarly presence from Asia, particularly China and Japan. Conversely, several African and small economies are inadequately represented.

4. Science Mapping

4.1 Cluster Analysis Using VOSviewer

This section delves into the use of extensive bibliometric techniques for an exhaustive exploration of key themes in the literature on valuation multiples. We constructed maps employing VOSviewer for interactive visualisation and features like zooming, scrolling, and search. We address the bibliographic coupling of publications based on reference similarity and the keyword co-occurrence to provide a full picture of the valuation multiple for the second objective. This integrated approach offers a nuanced and multidimensional understanding of the field’s structure, highlighting core research areas and developments.

4.1.1 Cluster/Themes of Valuation Multiples Identified Through Keyword Co-Occurrence Analysis

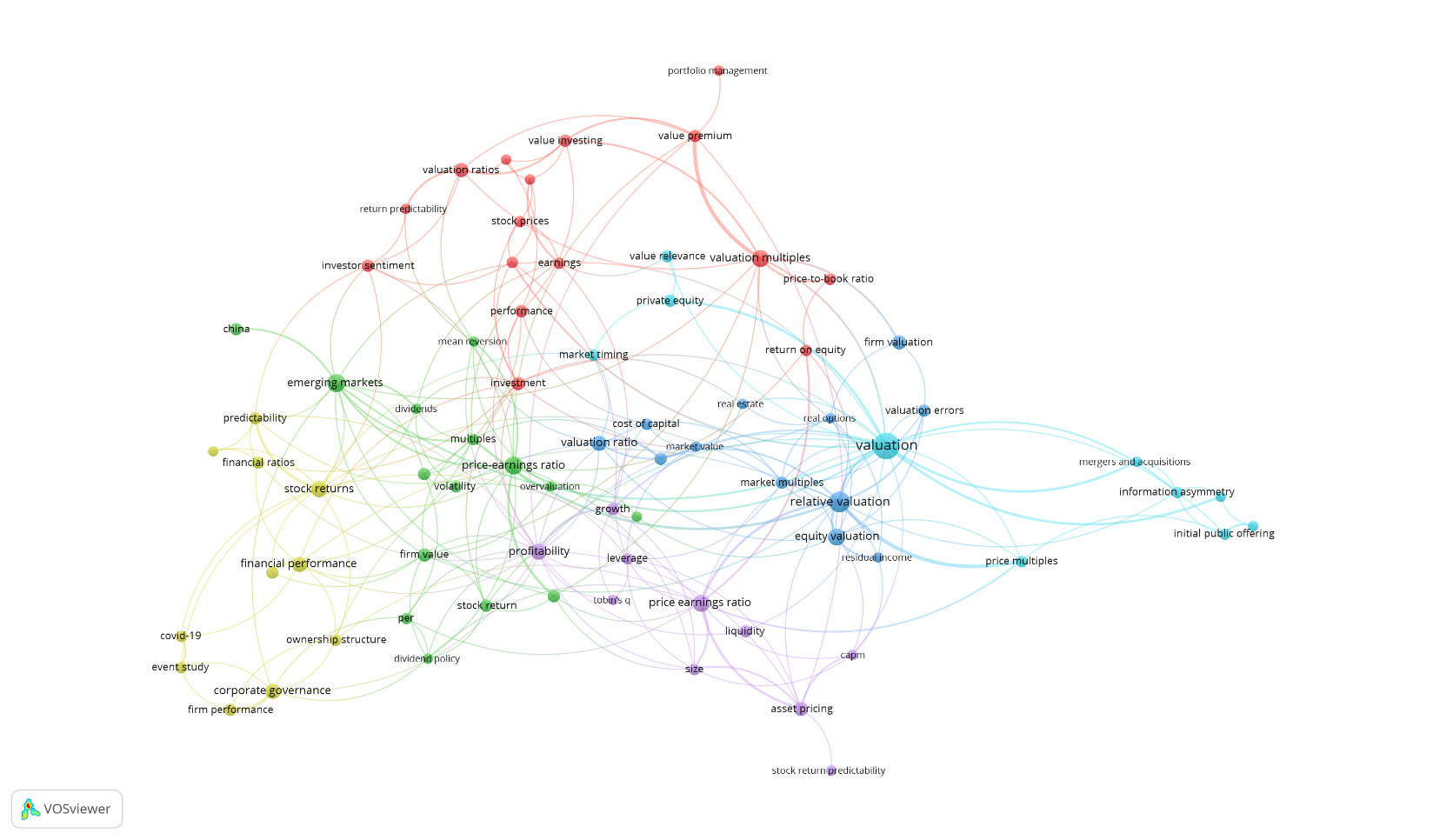

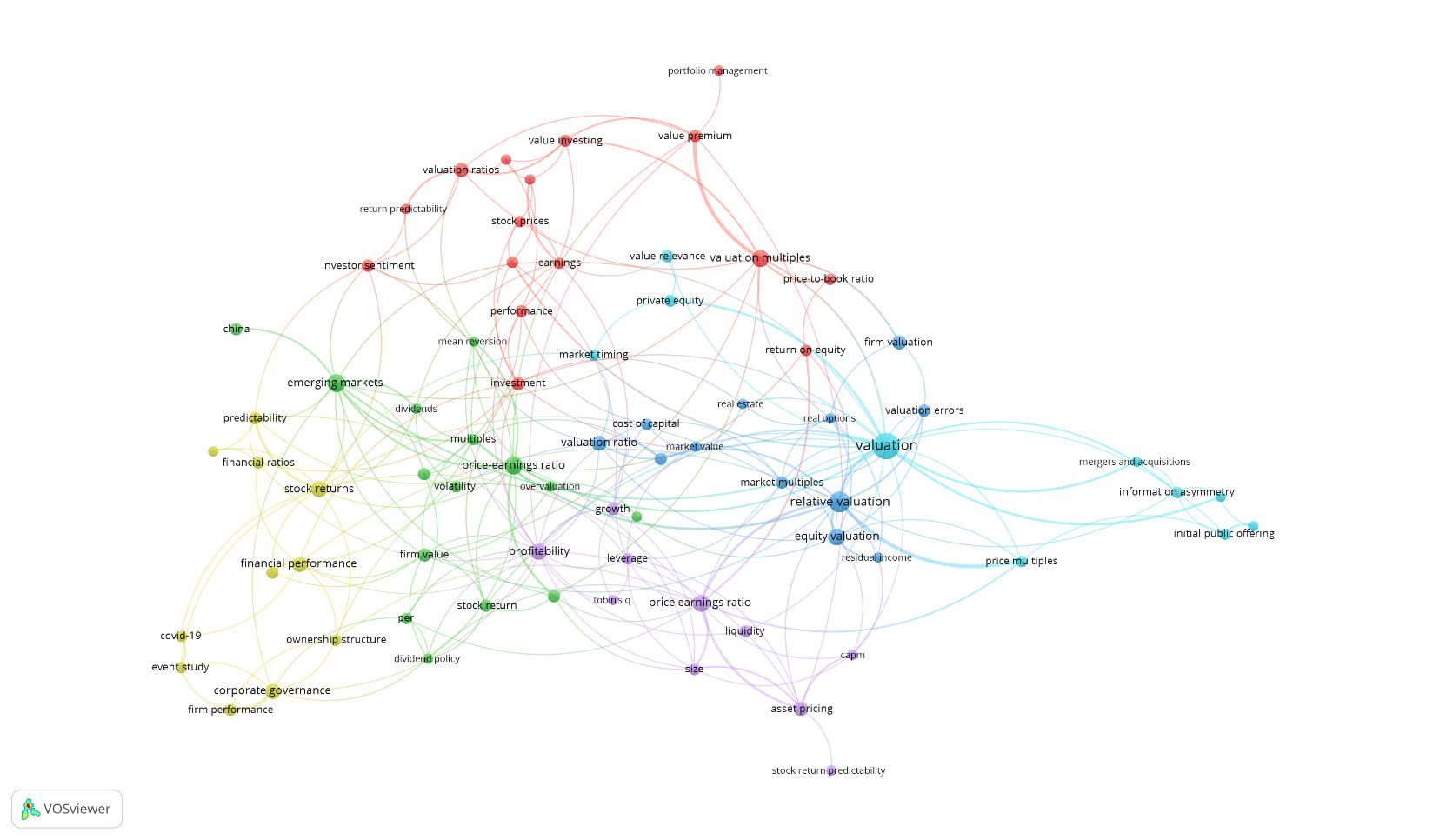

Among the 2,282 keywords employed by various authors throughout the study, encompassing 888 documents, a discerning analysis reveals that only 75 meet the threshold of minimum occurrence of five times. These have been categorised into five clusters. These clusters identify a common theme based on the author’s co-occurrence analysis of their keywords, which encapsulates the essence of their research (see Figure 7).

Keyword Co-Occurrence Cluster/Theme 1: Application of Valuation Multiples

The blue cluster/theme concentrates on the linkage between valuation multiples and their practical application across various financial contexts. At the core of this is the keyword “valuation”, which connects with the keywords like “relative valuation”, “equity valuation”, “mergers & acquisitions”, “initial public offer”, “real options”, “cost of capital”, “real estate”, “private equity”, “market value”, “valuation ratios”, and “price multiples”. Collectively, these terms indicate that valuation multiples are vital instruments in many financial decisions, including corporate finance, investment analysis, and capital market operations. Hence, this cluster emphasises how valuation multiples are widely applicable and versatile in both theoretical modelling and practical implementations.

Keyword Co-Occurrence Cluster/Theme 2: P/E Ratio, Valuation Dynamics and Emerging Markets

The green cluster focuses on the P/E ratio, one of the most debated ratios, and its role in valuation behaviour. This theme connects the P/E ratio with terms such as “volatility”, “mean reversion”, “stock return”, “overvaluation”, “company value”, “dividends”, and “dividend policy”. This suggests the significance of the P/E ratio in capturing pricing inefficiencies and market corrections. The use of region-specific terms, such as “China” and “emerging markets”, suggests a growing body of research on geographical variations in valuation procedures. Collectively, this cluster illustrates the P/E ratio’s critical role as a diagnostic tool for understanding valuation trends and market dynamics.

Keyword Co-Occurrence Cluster/Theme 3: Financial Ratios, Performance and Market Predictability

The yellow cluster centres on the relationship between financial performance and the predictability of valuation multiples. Terms like “firm performance”, “stock returns”, “corporate governance”, and “valuation accuracy” are the key themes indicating a strong emphasis on how firm financial metrics influence market outcomes. Additionally, this cluster includes references to external shocks, including COVID-19, through event study methodologies. This highlights how macro-level disruptions can affect the valuation and market response.

Keyword Co-Occurrence Cluster/Theme 4: P/E Ratio in Asset Pricing and Firm Characteristics

The purple cluster centres on how asset pricing models include the P/E ratio and its relation to firm-specific fundamentals. Coupling the P/E ratio to terms like “growth”, “liquidity”, “firm size”, and “Tobin’s Q” highlights its function in measuring a firm’s value with its fundamentals and the P/E ratio’s incorporation into asset pricing models, such as the Capital Asset Pricing Model (CAPM), and its predictive capacity for stock returns. This theme underscores the P/E ratio’s multifaceted role in both valuation theory and empirical asset pricing research.

Keyword Co-Occurrence Cluster/Theme 5: Linkages Between Valuation Multiples and Investment

The red cluster delves into one of the most pertinent functions of valuation multiples. This theme presents an apparent link between valuation ratios like “price-to-book value” and key investment themes like “portfolio management”, “value investing”, and “return predictability”. This cluster additionally features the notable inclusion of “investor sentiment”, which shapes market perception; it also links with “stock prices”. By taking behavioural factors into account, this theme underscores the role of market sentiment in shaping stock market valuation. It highlights the dynamic interaction between valuation ratios, investor behaviour, and portfolio performance.

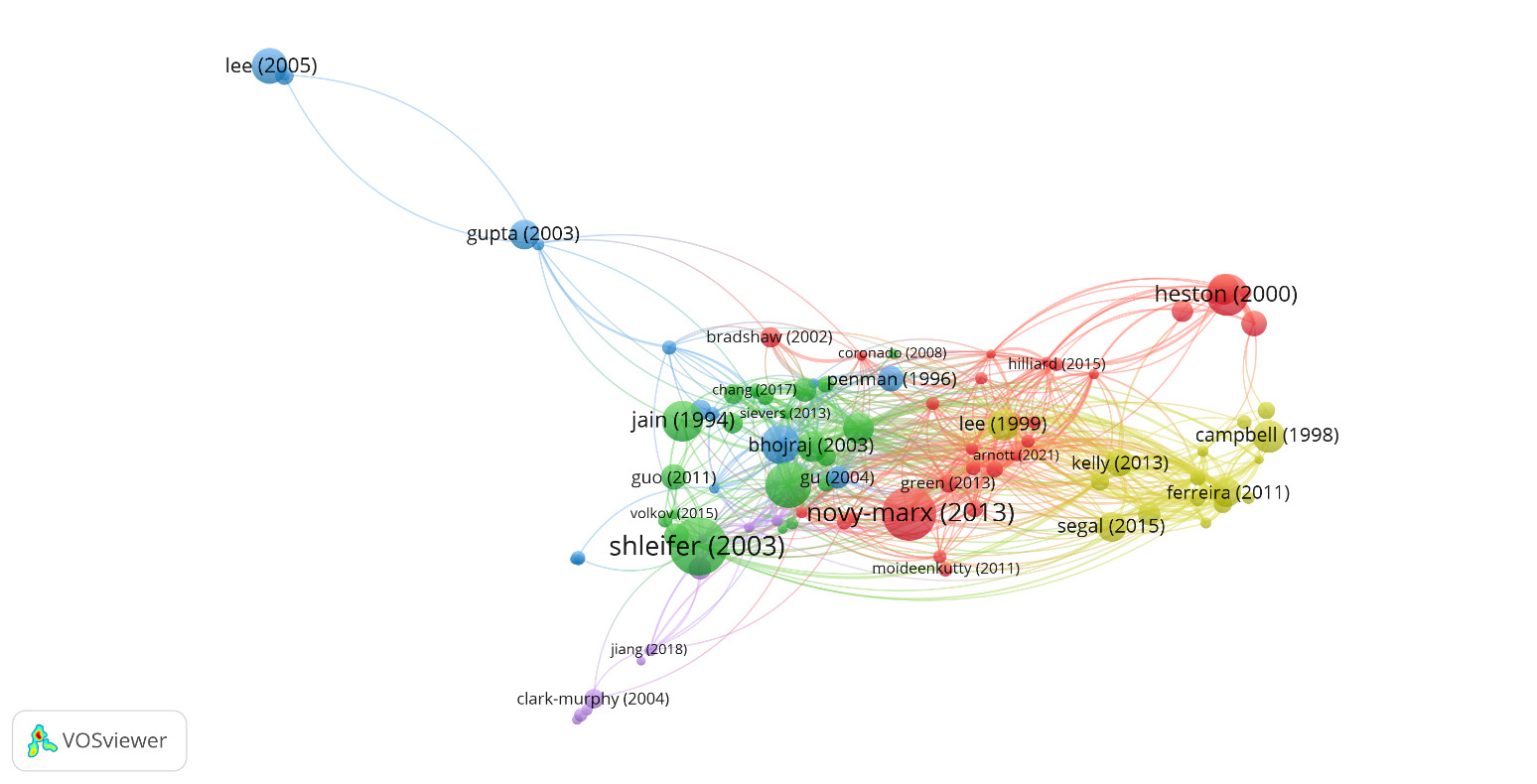

4.1.2 Clusters/Themes of Valuation Multiples Derived from the Bibliographic Coupling of Articles Through Referencing Similarity

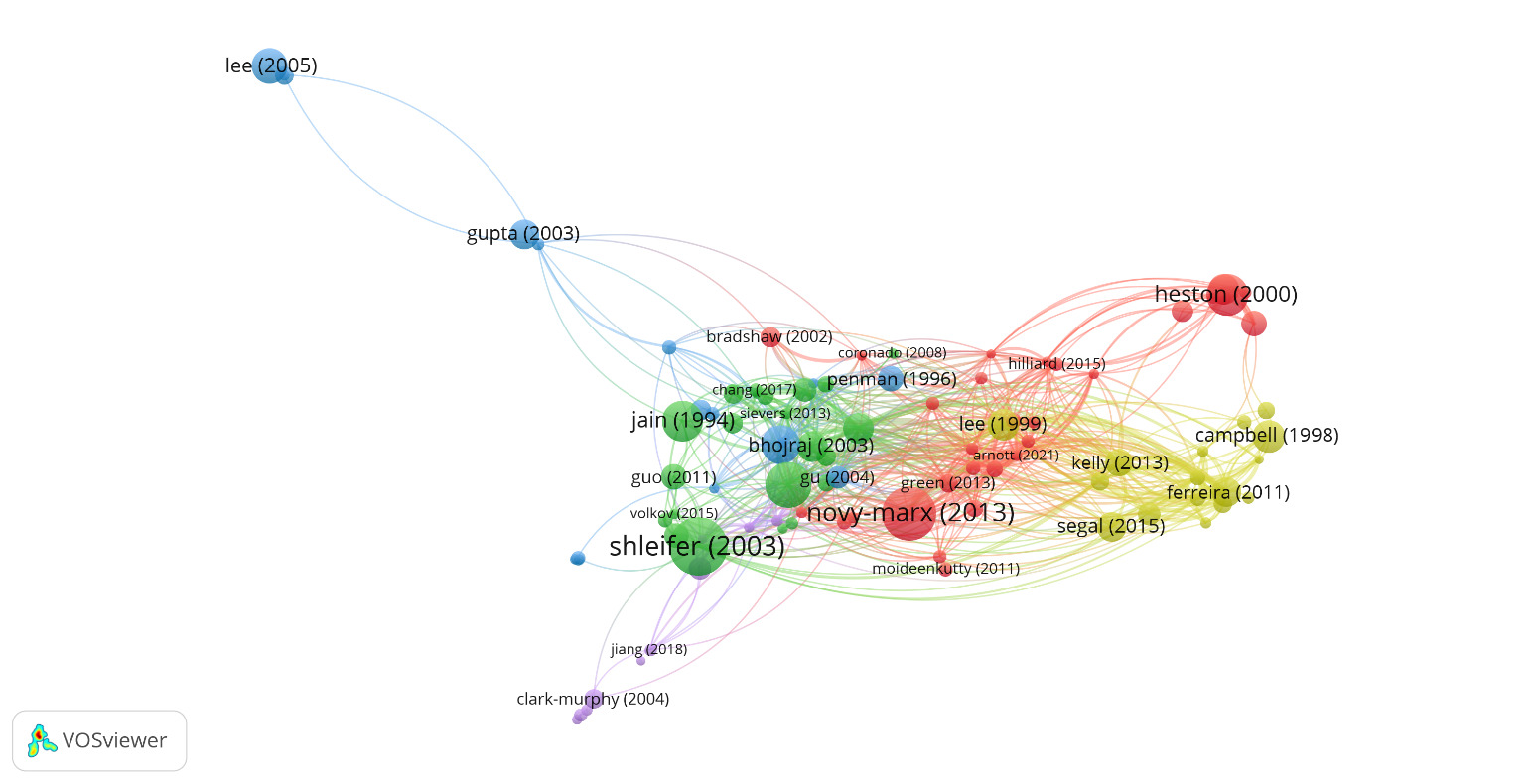

By coupling documents based on reference similarities, 141 highly cited articles, each amassing a minimum of 30 citations, were identified from the corpus. Four main clusters have been formed from these articles, each of which encapsulates prevalent themes within the field. Clustering the research provides a succinct illustration of the theoretical underpinnings and practical significance (see Figure 8).

Bibliographic Coupling Theme/Cluster 1: Industry Classification and Valuation Multiples in Corporate Transactions

The green cluster shows the research around the approach to selecting comparable firms for valuations and incorporation of valuation multiples in financial decisions like IPOs, M&A, spinoffs, firm valuation, and other venture capitalist investment decisions.

Bhojraj and Lee (2002) made a foundational contribution with their “Warranted Multiple” approach to the selection of comparable firms for valuation assessment. They concluded that compared with other techniques, the firm selected through this approach offers significant improvements over comparable firms selected on the basis of other techniques. An extended study by Bhojraj, Lee & Ng (2003) highlighted that GICS outperforms the alternatives, such as the Standard Industry Classification (SIC) and the North American Industry Classification System (NAICS). GICS showed superior performance in explaining stock return co-movements, cross-sectional variations in valuation multiples, projected growth, R&D expenditures, and various financial ratios. In the same field Lee et al. (2015) stated that the “co-search” algorithm or “Search-based Peers” is a novel method for the identification of peer firms for estimating their relative valuation.

This cluster also includes a body of literature on corporate transactions. One of the highly cited studies in IPO valuation is Purnanandam and Swaminathan (2004), which studied a sample of more than 2,000 IPOs and stated that the median is considerably overpriced at the offer price compared with values based on industry peer price multiples. Jain and Kini (1994) documented the decline in the market-to-book (M/B) ratio, P/E ratio, and earnings per share post-issue. Paleari et al. (2014) stated that multiple-based valuation of IPOs enables underwriters’ discretion when selecting comparable firms.

On the M&A front, the cluster includes studies such as Guo et al. (2011) and Rhodes–Kropf et al. (2005). A seminal contribution here is Shleifer and Vishny (2003), who developed a stock market-driven acquisition model incorporating a market-based valuation approach, which is relative valuation. In addition, the cluster also highlighted multiplier-based valuation for valuing branded businesses (Mizik & Jacobson, 2009). In the study, Sievers et al. (2013) concluded that industry-specific total asset multiples outperform the revenue multiples model while valuing venture capital investments.

Bibliographic Coupling Theme/Cluster 2: Valuation Ratios and Stock Performance

The red cluster showcases the diverse range of topics around valuation multiples, stock market dynamics, and the effect of interest rates, risk, profitability, and growth on valuation ratios.

A foundational study by Ang and Liu (2001) analysed how macroeconomic factors affect the price-to-book (P/B) ratio. The most cited article in this cluster is Novy-Marx (2013), which offered a new perspective on the value-growth debate, suggesting that book-to-market has a considerable impact on stock performance and returns. Fama and French (2007) demonstrated how the P/B ratio explains returns on value and growth stocks. As value firms improve profitability, their P/B ratio converges, while growth firms’ P/B ratio declines as their growth potential diminishes.

Nissim and Penman (2003) empirically proved that P/B ratios explain cross-sectional variance in current and future rates of returns that are based on return on equity. Kogan and Papanikolaou (2013) linked P/B ratio, P/E ratio to variance in stock returns by linking them to a firm’s exposure to investment-specific (technology) shocks. While in a conflicting study, Lehn et al. (2007) argued that between 1980 and 1985, there was no discernible correlation between governance indices in the 1990s and contemporary valuation multiples.

This cluster also addresses analysts’ target price forecasts, with studies such as Da and Schaumburg (2011) and Kerl (2011). It includes country-specific evidence on valuation-return dynamics from the US (Brammer et al., 2009) and UK (Al-Horani et al., 2003). Moreover, the other prominent research theme in the cluster is the valuation of real options. Key contributions include Christoffersen and Jacobs (2004), Heston and Nandi (2000), and Trigeorgis (1993), who examine derivative pricing models and their relevance in asset valuation.

Bibliographic Coupling Theme/Cluster 3: Valuation Ratios – Fundamental, Behavioural, and Macroeconomic Factors

The research in the yellow cluster concentrates on variables that affect valuation ratios, such as firm fundamentals, investor behaviour, and macroeconomics.

Segal et al. (2015) stated that there are two kinds of uncertainties – good and bad. While both uncertainties contribute positively to risk premia, good uncertainties like investment, output and consumption are positively related to valuation ratios. Conversely, asset prices tend to decrease when uncertainties like a decline in economic growth occur. Nguyen and Faff (2003) found that shorter horizon exchange rate exposure has a negative impact on a firm’s P/E ratio.

Coakley and Fuertes (2006) highlighted relevant results stating that fundamental factors drive long-term mean reversion of valuation ratios, while investor sentiment fuels short-term price deviations during bull markets. In bull markets, positive shocks have more powerful and enduring effects; yet, valuation multiples eventually return to equilibrium, ensuring that prices are in line with fundamentals. Further supporting the role of sentiment, Arif and Lee (2014) observed that corporate investments reach their highest point when investor sentiment is favourable, yet these times are usually followed by poorer stock returns. Even after controlling for variables like discount rates, equity flows, valuation multiples, and other sentiment indicators, this pattern remains consistent across the majority of developed economies.

Bibliographic Coupling Theme/Cluster 4: Valuation Multiples as Indicators of Financial Performance and Industry Dynamics

The blue cluster explores how valuation multiples are tools for assessing firm performance and industry-specific trends. The theoretical underpinnings are provided by Damodaran (2007), who highlights that these ratios are anchored in fundamental determinants: growth, risk, and profitability. Empirical studies support this. Penman (1996) first articulated the two prominent ratios P/E and the market-to-book ratio (M/B) and described M/B as an indicator of future return of equity and a representation of growth. According to the study by Barth et al. (1998), the ability of book value to explain firm value increases, while the relevance of net income declines in the five years before bankruptcy. This demonstrates how book value becomes a crucial criterion when financial turbulence makes earnings less reliable measures of firm value. This study sampled three industries: pharmaceutical, financial, and manufacturing, and found that book value is a stronger determinant of valuation compared with net income. Damodaran (2009) supported this view by emphasising that equity-based multiples, such as P/B, are more appropriate than enterprise value multiples when valuing financial firms. He argued that due to the unique capital structures and regulatory frameworks of these firms, enterprise value multiples are less suitable. The effectiveness of two value drivers, P/E and price-to-sales (P/S) ratios, for creating stock price projections is examined in the study by Pandey (2012). Consequently, Sehgal and Pandey (2014) researched price multiples such as P/E, P/B, and P/S, which may be utilised to create effective trading strategies. With a focus on the Indian stock market, this study adds to the body of research on asset pricing and equity valuation for emerging countries. In a recent empirical study, Soewarno and Tjahjadi (2020) concluded that for banking industries, the presence of strong intellectual capital is associated with a higher P/B ratio and enhanced investor confidence. Collectively, these studies support the importance of tailoring valuation approaches to the unique characteristics of specific industries.

5. Key Takeaways and Future Research Avenues

5.1 Key Takeaways from Performance Analysis

The literature on valuation multiples reflects a wide spectrum of perspectives, illustrating the diversity of the discipline. The study underscores the need for continuous contributions from diverse sectors and economies to deepen the understanding of relative valuation and its role in financial and investment decision-making. Drawing on performance analysis, the literature identifies several key insights and underlying structural gaps as follows.

5.1.1 Temporal Trends in Annual Research Production

Analysts and academics began to signal a move toward sophisticated valuation models around the onset of the 21st century. However, there is a general upward trajectory in annual research production. Despite the collapse of the internet bubble in 2000 and the financial crisis of 2008, there has been a notable increase in academic literature, although this growth has been reactionary, characterised by publication spikes after crises rather than sustained or proactive momentum.

5.1.2 Keyword Emphasis

Keyword visualisation shows strong concentration on terms like “stock returns” and “market valuation”. Nevertheless, other significant factors, like investors’ perspectives, corporate governance, and emerging market valuation methodologies have received comparatively little attention. This disparity suggests underrepresented aspects in the research field and hence requires more diverse studies.

5.1.3 Geographic Representation

The study depicts a clear bias in the research’s geographic representation, with growing attention to a few emerging economies and little or no focus on developing markets. There is a knowledge vacuum about how valuation multiples function under varied market structures, levels of efficiency or regulatory environments. The UK, Germany, France, Italy, and the Netherlands contribute significantly to academia. However, the whole of Europe still lacks in the total production of academic literature, citation effect, and cohesiveness. Europe might shape global valuation research via cross-border cooperation, regional research networks, and EU policy coherence. This is important for Ireland and other open economies as valuation multiples affect market efficiency and capital allocation.

5.2 Key Takeaways from the Science Mapping of Valuation Multiples

Our research has successfully mapped out the valuation multiples’ various clusters and themes. This comprehensive framework provides a deep understanding of this crucial area of financial decision-making and portfolio management. The science mapping reveals a dominant theme and influential contributors. This analysis also identifies structural gaps, offering valuable direction for future research, managerial practice, and policy development.

5.2.1 Keyword Co-Occurrence Analysis

The co-occurrence analysis indicated the most significant themes in the research field through the occurrence of key terms. One of the most prevalent keywords in the field is “price earnings ratio” which is closely linked with keywords like “stock valuation”, “stock returns”, “asset pricing”, and also connects with other cluster keywords like “valuation”, “equity valuation”, and “valuation multiples”, highlighting the wide usage of the P/E ratio in financial metrics, including valuation comparison, and investment decision making. These findings align with the practitioners as price multiples are one of the common approaches used by investment analysts for valuation. Another important keyword is “valuation” which is interconnected with equity valuation, IPO, fundamental analysis, private equity, valuation multiples, investment and the P/E ratio, again highlighting the role of valuation in IPO pricing, private equity and other financial decisions.

5.2.2 Bibliographic Coupling of Articles

A bibliographic coupling analysis illustrates connections and relationships between academic publications based on shared references. Thematic clusters highlighted several insights on the application of valuation multiples and also highlighted key studies on finding the appropriate peer for comparable company analysis. The cluster network visualisation map also highlighted industry-specific, firm-specific, and country-specific studies. Furthermore, we can draw insights from the authors’ co-citation analysis. First, there seems to be a high level of cooperation between authors, as they recognise each other’s contributions to the field. Second, the most impactful authors are from the Western part of the globe. This indicates that the field of relative valuation is largely influenced by the West.

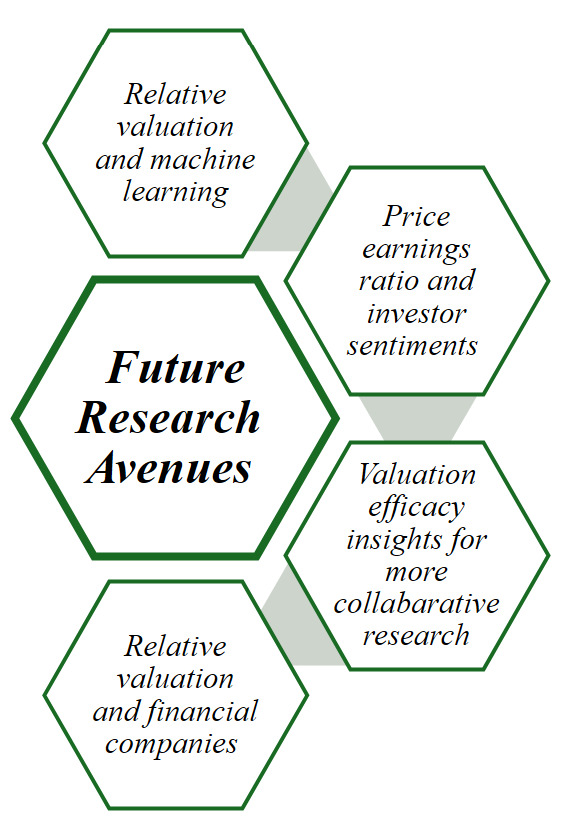

5.3 The Way Forward for Research in Valuation Multiples

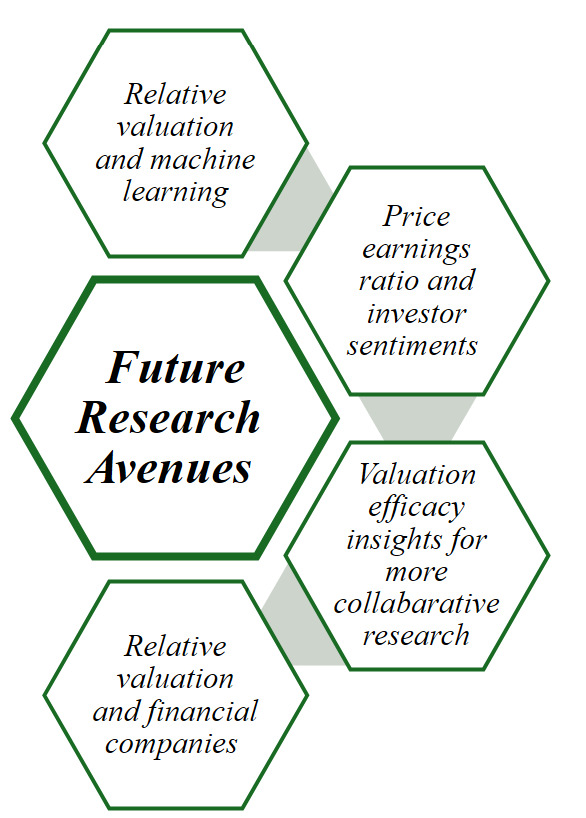

This section discusses potential study pathways that might improve understanding of the research field. This article offers future research directions after reviewing current literature and identifying knowledge gaps (presented in Figure 9).

5.3.1 Relative Valuation and Machine Learning

One of the issues in the relative valuation approach is how to find a similar asset to compare the value, as no two assets are the same. While there is some groundbreaking research regarding the problem, Bhojraj and Lee (2002) use the OLS regression approach. A recent study by Geertsema and Lu (2023) uses the Gradient Boosting machine technique for peer group firm selection. Researchers can explore more machine learning tools that may outperform the traditional models for valuation accuracy.

5.3.2 Price Earnings Ratio and Investor Sentiment

Investor sentiment and the P/E ratio are interconnected elements in the stock market. Only a couple of studies have explored the relationship between these two – Rahman and Shamsuddin (2019) and Mian and Sankaraguruswamy (2012). Hence, there is a knowledge gap in the field that could explain the behavioural explanations of price multiples.

5.3.3 Valuation Efficacy Insights from More Collaborative Research

There is a great representation of North America in the field, which underlines the need for greater collaboration across European, emerging and other developing economies. This will make the field more diverse and can promote valuation through different regulatory insights and market efficiency.

5.3.4 Relative Valuation and Financial Companies

The effectiveness of stock market multiples for equity valuation of nonfinancial enterprises has been a topic of much discussion among finance and accounting researchers (e.g., Alford, 1992; Bhojraj, Lee, & Oler, 2003; Bhojraj & Lee, 2002; Lie & Lie, 2002; Liu et al., 2002; Yee, 2004). However, only a few studies have discussed valuation multiples and financial companies’ stock valuation (Forte et al., 2020; Nissim, 2013).

6. Conclusion

This study attempts to present a comprehensive understanding of the theoretical advancements in the field of valuation multiples, offering insight into their wide application in assessing financial performance, exploring broader market dynamics, stock performance, corporate transactions, and other financial and strategic decision-making. The literature was analysed on both quantitative (performance analysis) and qualitative (thematic) views. The key clusters created with the VOSviewer software map the wide literature on valuation multiples that provide critical insights and offer several theoretical and practical implications presented in Table 5. The study lays the groundwork for future research by mapping the existing literature and finding gaps which will help academicians and practitioners to understand valuation multiples in an increasingly complex financial landscape. The study uses only the Scopus database for corpus creation and thus, in future, research could be conducted using Web of Science or combining the outcome from both Scopus and Web of Science. Our dataset may underrepresent European accounting scholarship, as prominent UK and continental scholars often publish in interpretivist outlets (e.g., Accounting, Organizations and Society) that fall outside the capital markets-focused valuation multiples literature examined here. To sum up, this review highlights the evolution, development and multidimensional significance of valuation multiples.