This literature review forms part of my PhD thesis. I am grateful to my supervisor, Páll Ríkhardsson, and the thesis committee members, Carsten Rohde and Niels Sandalgaard, for their valuable guidance. I also thank the two anonymous reviewers and the editor for their insightful comments and the participants of the seminars and conferences where earlier versions of this review have been presented. I am especially grateful to Jytte G. Larsen and Cristiana Parisi for their invaluable support and advice.

1. Introduction

Budgeting is a crucial management accounting tool (Hansen, 2011; Hansen et al., 2003). Despite its widespread use, it has been criticised (Hopwood, 1986, 2009). Scholars and practitioners have highlighted its inefficiencies, such as its time-consuming nature, misalignment with strategy, and inability to adapt to dynamic environments (Covaleski et al., 2003; Hofstede, 1969). Practitioners have echoed these concerns, with some advocating for alternatives like activity-based budgeting or even abandoning budgeting entirely, as seen in movements such as Beyond Budgeting (Bogsnes, 2008; Hope & Fraser, 2003).

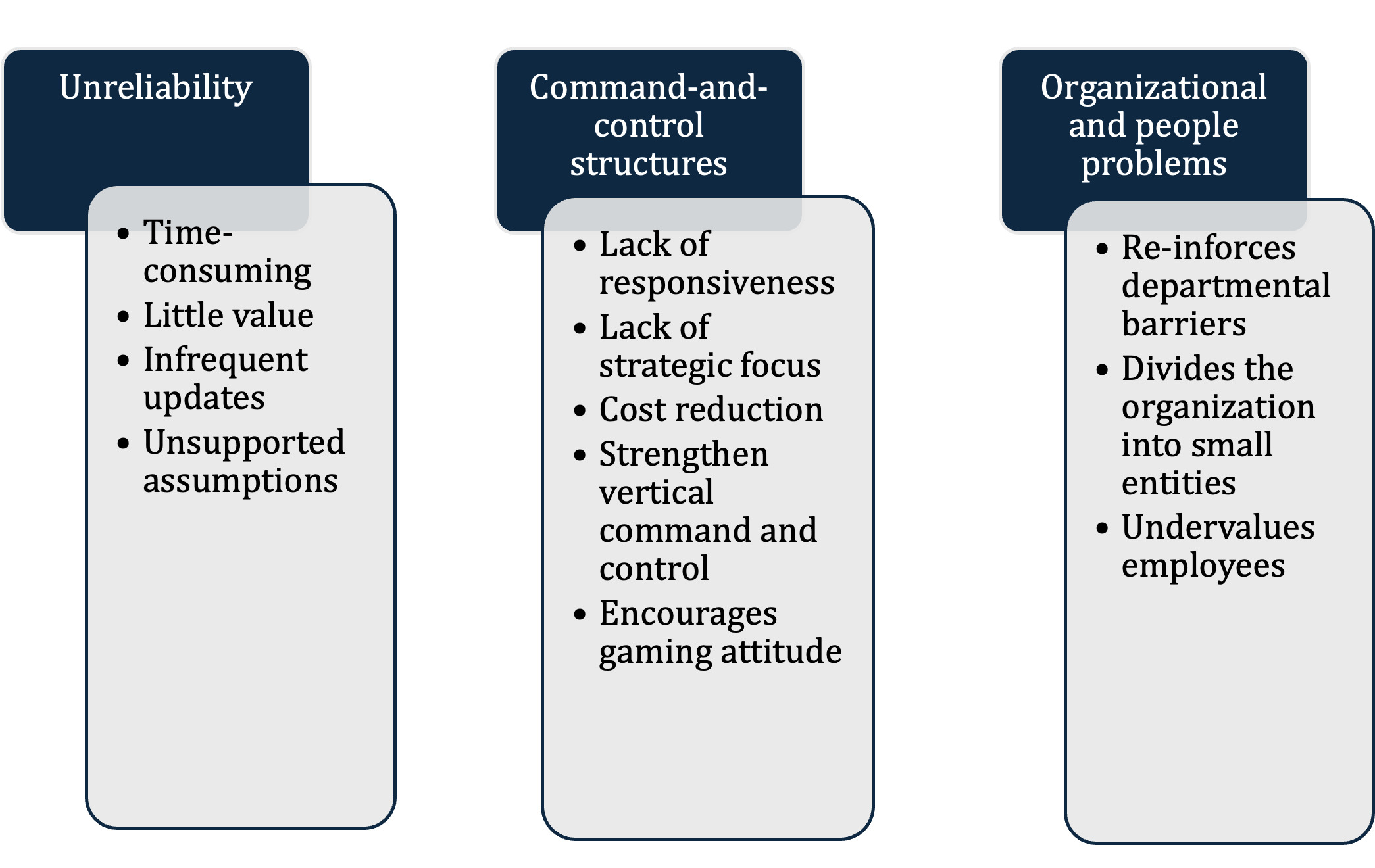

There is a long-standing tradition in management accounting research that involves engaging directly with practitioners (Chapman & Kern, 2012). Hansen et al. (2003) expressed concerns about the disconnect between practitioners’ needs for developing budgeting practices and scholarly literature focusing on traditional issues like participative budgeting. Drawing on a practitioner-led report by Neely et al. (2001), Hansen et al. (2003) identified 12 budgeting weaknesses most frequently cited by practitioners, highlighting long-standing practitioners’ concerns about the relevance and effectiveness of traditional budgeting practices. Hansen et al. (2003) categorised them as: unreliability, command-and-control structures, and organisational and people problems. Figure 1 presents these 12 most cited weaknesses.

The unreliability weakness claim is that budgets are outdated by the time they are used and rely on unsupported assumptions and guesswork made months before the accounting year begins. Organisations then struggle to adapt to environmental changes, making the considerable time invested in the budgeting process ineffective.

Command-and-control structure weakness (involving the imposition of a vertical command-and-control structure), emphasises how centralised decision-making can stifle initiative and change. This emphasis is reflected in budgeting practices prioritising cost control over strategic alignment (Hansen et al., 2003; Neely et al., 2001).

Organisational and people problems underscore budgeting issues hindering empowered employees, fostering perceptions of budgets as control tools, undervaluing their contributions, and reinforcing departmental barriers instead of promoting collaboration. Hansen et al. (2003) argue that these weaknesses call for innovative research and solutions.

However, these concerns are not new. Around the same time as Hansen et al. (2003) made their call, Covaleski et al. (2003) and Luft and Shields (2003) observed that budgeting research remains focused on traditional issues. Selto and Widener (2004) identified a growing gap between academic and professional publications, noting that academic research reflects traditional research topics that might not reflect the practitioners’ concerns. This gap between accounting research and practitioners’ concerns has been acknowledged by many (Mitchell, 2002; L. D. Parker et al., 2011; Rajgopal, 2021; Tucker & Parker, 2014; Tucker & Schaltegger, 2016). All come to the same conclusion: accounting is an applied field, and it only exists because there is a real-world practice of accounting. However, challenges persist, especially regarding the efficacy of budgeting in uncertain times (Ekholm & Wallin, 2000, 2011; Hansen et al., 2003).

This paper revisits these debates by conducting a systematic literature review of budgeting research published since 2003. It aims to answer the question: To what extent has budgeting research reflected practitioners’ concerns? In doing so, it updates and extends the reviews by Covaleski et al. (2003) and Luft and Shields (2003).

This review contributes to both theory and practice in several ways. Firstly, it synthesises the budgeting literature since the work of Luft and Shields (2003), highlighting its importance as a research subject. Secondly, it identifies research themes and highlights gaps where academic research diverges from practitioners’ concerns. Thirdly, it evaluates how these studies engage with the budgeting weaknesses. Lastly, it provides a roadmap for future studies, emphasising the importance of addressing budgeting’s role in dynamic and uncertain environments. This review aims to foster more relevant and impactful management accounting research by bridging the gap between academic research and practitioners’ concerns.

The remainder of this paper is organised as follows. Section 2 presents the methodology used in the literature review. Section 3 presents a review of empirical research on budgeting. Section 4 outlines reflections and future research opportunities. Finally, Section 5 closes the paper with some brief concluding remarks.

2. Methodology

This study employs a systematic literature review approach following Tranfield et al. (2003), which is designed to enhance transparency, replicability, and rigour in synthesising existing knowledge. Systematic reviews are distinct from but related to structured literature reviews (Massaro et al., 2016). Structured reviews also emphasise a clear protocol and replicable selection criteria, allowing for more interpretive synthesis. Systematic reviews, in contrast, apply stricter standards for comprehensiveness and bias minimisation. The study aims to map the empirical budgeting literature comprehensively and critically assess its response to practitioners’ concerns; therefore, the systematic review method is most appropriate. Nonetheless, the structured review tradition informs the organisational and analytical framing used here.

As in other literature reviews (Farrell & Sweeney, 2021), journal ranking lists are used to choose the journals on which to focus. The focus is on high-calibre accounting journals, which rank as 4*, 4, and 3 on the Chartered Association of Business Schools’ 2021 Academic Journal Guide (The ABS Rankings). This process yielded a list of 19 journals – see Appendix A.

The search was limited to 2003–2023 for several reasons. Firstly, the review intends to map recent budgeting studies. Luft and Shields (2003) have already mapped studies on management accounting up to 2002. An updated synthesis of budgeting research is relevant at this point. However, considering the critiques budgeting has undergone in recent years, it is relevant to analyse if budgeting research has evolved since Luft and Shields’s (2003) work. Secondly, the literature review takes its starting point from Hansen et al. (2003) and analyses whether recent studies on budgeting in private organisations have addressed the issues raised there. Thirdly, the organisational environment has changed, leading to restructuring and outsourcing, and these external changes have caused more uncertainty (Otley, 2016; Otley & Soin, 2014). Technological advancements have altered business practices through modern computer technology and the internet (Otley, 2016). Lastly, there have been changes in the responsibilities of financial and accounting professionals (Baldvinsdottir et al., 2009). It is irrelevant to include older studies referring to a business environment that does not correspond to today’s.

Using the journals database, articles were searched using the keyword “budget*” in the title, abstract, and keywords. The search was restricted to “budget*” to ensure that the literature review focuses on studies explicitly analysing budget and budgeting. Other terms, such as “performance measurement” and “target-setting”, would have been less appropriate to the aim of the study. The use of the asterisk with the keyword allowed for search on variations of “budget”, such as “budgets” and “budgeting”. After a first search, about 130 articles were found in all 19 journals. The articles were screened to exclude those unrelated to the subjects of this study, such as studies on capital budgeting, budgeting in the not-for-profit organisation, and budgeting in public entities (hospitals, governmental, publicly owned companies, schools, universities). Since the review focuses on how budgeting research reflects practitioners’ concerns, only articles providing empirical evidence were included. Therefore, purely conceptual or theoretical articles and empirical studies conducted in public or not-for-profit settings were excluded. These contexts were considered beyond the scope of the review, as budgeting practices and roles in such organisations differ from budgeting in private entities. Applying the procedure here, and after reading the articles, 59 articles remained in the final sample. (A list of these articles is available in Appendix B.) As in any review paper, it cannot be ruled out that articles potentially relevant to the topic were missed using the approach described. This limitation may arise because of the keyword search, which may exclude studies using alternative terminology. While efforts were made to ensure a comprehensive search, the inherent challenges of capturing all relevant work remain a limitation of the review process.

Each article was read thoroughly in three rounds to analyse the literature. After a first reading, the article was summarised. In the second round, it was read with two questions in mind: What is the main theme regarding budgeting in this study? and How does this theme relate to the budgeting weaknesses? Figure 1 presents the classification of the budgeting weaknesses developed by Neely et al. (2001) and Hansen et al. (2003), which served as the basis for mapping each study. The third round was intended to ensure the data quality and that the themes associated with the study were accurate.

3. Results and Discussion

3.1 Synthesis of Budgeting Research

Table 1 below summarises the articles in the sample published in high-calibre accounting journals from 2003 to 2023. The table shows that the highest number of studies were identified in Accounting, Organizations and Society (16), followed by Management Accounting Research (nine). The focus of these journals on management accounting can explain these results. The table also illustrates the distribution of the publications within the period. While more studies were published in 2008, 2010, 2011, and 2015, there are no significant differences with the other years. The author did not find any explanation of why specific years were more prolific for articles on budgeting than others.

Appendix B presents bibliographical information on the 59 articles included in this review. It includes the journal abbreviation, authors’ names and publication year, the methodological approach (survey, experiments, database/archival data, and case study/interview), the sample size, the country where the study took place, and the research theme as defined by the authors of the articles. Most articles in the review (45) used a quantitative methodology. In contrast, 11 articles followed a qualitative research approach, and three studies (Aranda et al., 2014; Becker et al., 2016; T. Davila & Wouters, 2005) used a quantitative and qualitative methodology. The quantitative studies used experiments (20), surveys (22), and database/archival data (three), while the qualitative studies used case studies/interviews. Eight experimental studies are about budgetary slack, six are about participative budgeting, and three are about budget negotiations. A notable trend in the US is experimental studies conducted among students. More than half of these studies focus on budgetary slack or participative budgeting. Meanwhile, survey studies conducted among managers in Europe (nine) have sample sizes ranging from 1,250 managers (Huang & Chen, 2009) to 57 managers (Hansen & van der Stede, 2004). Six case studies were conducted on single companies and nine on company groups. Eight were conducted within European companies, and five studies were conducted outside Europe. Most of the studies were conducted in Western industrialised countries, with 25 conducted in North America, 21 in Europe, four in Australia and New Zealand, and four in other world regions. Only five studies were conducted in more than one country.

3.2 Themes in Budgeting Research

The studies were mapped and analysed to determine whether recent budgeting studies addressed practitioners’ concerns. Table 2 presents an overview of the research themes and their distribution over time. Based on the keywords used by the original authors, 26 themes were identified. As in Luft and Shields (2003), participative budgeting was the most frequently researched theme with 13 studies, followed by budgetary slack (9 studies) and Beyond Budgeting (six studies). Other themes, such as budgetary control, budget negotiations, and budget reports appeared less frequently, with three studies each. Additional themes were also identified, although these were more isolated and appeared less frequently in the sample.

This review includes all relevant empirical studies on budgeting, organised into three primary themes: participative budgeting, budgetary slack, and Beyond Budgeting. A fourth category includes studies that address other budgeting topics, such as budget reporting and control. By structuring the analysis around the four categories, the review ensures a comprehensive and balanced account of recent empirical research while identifying the primary theoretical and practical developments. While each study is assigned to a single theme based on its primary focus as indicated by the original authors, it is acknowledged that conceptual overlaps exist. For instance, participative budgeting and budgetary slack are often intertwined: slack may arise from participative processes in which subordinates influence budget targets.

This thematic structure enables analytical clarity and conceptual flexibility, accommodating the diversity of approaches within the budgeting literature while highlighting the dominant lines of inquiry that have emerged in response to practitioners’ concerns.

3.3 Key Themes and Budgeting Weaknesses

3.3.1 Participative Budgeting

Participative budgeting occurs when subordinates are involved in the budgeting process and may influence the budget process (Brink et al., 2017). As shown in Appendix B, studies on participative budgeting were published across seven journals, predominantly in English-speaking contexts (notably the US and Australia). Most used either survey methods (six) or student experiments (six). Four sub-themes within participative budgeting were uncovered: (i) superior–subordinate relationships and information flow; (ii) participative budgeting and performance; (iii) cultural aspects of participative budgeting; and (iv) participative budgeting and budgetary slack.

Superior–Subordinate Relationships and Information Flow

Initially, research on participative budgeting focused on the superior–subordinate relation and information flow (Shields & Shields, 1998), a line of inquiry that continues to shape the literature.

Parker and Kyj (2006) developed a model exploring vertical information sharing in budgeting. They found a direct link between participation and information sharing, with organisational commitment as a mediator influenced by role ambiguity. Parker and Kyj’s study found a positive correlation between information sharing and individual performance, highlighting the inverse relation between budget participation, role ambiguity, and individual performance.

Expanding on this, Kyj and Parker (2008) explored the causes of budget participation’s significance in the workplace. They examined why superiors encourage subordinates to participate in the budget process and found that supportive leadership styles foster this participation. Furthermore, when budget goals affect performance evaluations, leaders emphasise organisational justice by promoting involvement. Thus, budget participation mediates the relationship between evaluative budget use and work-outcomes justice.

Abdel-Rahim and Stevens (2018) contributed to this literature by studying the impact of information systems on managers’ honesty in the budget report. Their experiment among students showed that an information system’s precision increases honesty in managerial reporting. However, this positive precision effect is weaker when the information system’s accuracy is low. They concluded that the accuracy of information systems is a form of information asymmetry that should be controlled and examined further. Their study helps explain the mixed results of prior studies.

Douthit and Majerczyk (2019) investigated the effect of the perceived role legitimacy of superiors by subordinates. The experiment showed that when subordinates perceive superiors as legitimate, budgetary slack is lower than when subordinates perceive superiors as illegitimate. While this study took place in a participative budgeting context, it contributed more to the superior’s role legitimacy literature than to the budgeting literature.

Participative Budgeting and Performance

A significant body of research has examined how participative budgeting influences managerial performance, often through mediating variables such as knowledge, feedback, fairness, and organisational context. Agbejule and Saarikoski (2006) investigated how budget participation, cost management knowledge, and managerial performance are interconnected. Their survey showed that managers’ cost management knowledge influences the impact of budget participation on their perception of managerial performance. They concluded that increasing managers’ cost management knowledge could enhance their performance in the budgeting process.

Later, Chong and Johnson (2007) examined the impact of participative budgeting on job performance, finding that task exceptions and task analysability are significant antecedents. Their survey suggests that participative budgeting facilitates the exchange of job-relevant information among subordinates, enabling them to develop strategies to achieve their goals. Furthermore, the study supported the idea that participative budgeting aids in setting challenging yet achievable goals and enhancing job performance.

Studies on whether managers should have a voice in budget allocation have presented conflicting results. Byrne and Damon (2008) explored how giving managers a voice in budget allocation settings improves their performance. They demonstrated that the circumstances in which the voice and the explanation improve performance depend on the impression that budget allocation is unfair. According to this study, setting a budget and explaining its rationale might be a better approach.

Nouri and Kyj (2008) studied how performance feedback influences budgetary participation. The study examined the impact of job performance on perceptions of budgetary participation and factors like role ambiguity. The experimental findings indicated that performance feedback influences individuals’ perceptions of budgetary participation, job satisfaction, role ambiguity, motivation, and access to job-relevant information. The results highlighted the correlation between self-reported individual characteristics, performance data, and organisational variables like participative-budgeting performance data.

Additionally, the behavioural underpinnings of budget reporting have been investigated. Blay et al. (2019) focused on the reasons behind the preferences for honesty and used AIM (affect intensity measure) a psychometric measure. Their experiment showed that subordinates feel a negative effect when diverging from a social norm of honesty. This preference for honesty also reduces slack. This study may have a practical contribution, as firms prefer employees with strong preferences for honesty. Those who do not place much importance on honesty may try to game the system. AIM is less susceptible to gaming and, thus, more useful.

Likewise, Cannon and Thornock (2019) investigated the similarity between one’s decision environment and that of a referent peer regarding budgetary reporting. The study suggested that identifying with a group with similar characteristics affects one’s behaviour, as people view themselves as part of a group with similar characteristics. This suggested that managers facing similar environmental conditions feel more comfortable adjusting their behaviour to adhere to the social norms of peers withing the same environment. Furthermore, this study showed that when managers are unaware of their peer’s behaviour, they predict their peer’s report under similar circumstances.

Cultural Aspects of Participative Budgeting

Wong-On-Wing et al. (2010) tested a motivation-based model of participation in budgeting, differentiating between intrinsic, autonomous, and controlled extrinsic motivations. Their survey findings indicated a positive link between intrinsic and autonomous extrinsic motivations and budgeting participation, correlating with performance. Conversely, controlled extrinsic motivation showed a negative association with performance. The study highlights the need to discern different motivation types in participative budgeting research, suggesting that the mechanisms benefiting from budgeting participation may be more complex than previously thought.

Participative Budgeting and Budgetary Slack

Some studies have explicitly examined how participation interacts with slack creation. Lau and Eggleton (2003) investigated whether information asymmetry and budget emphasis moderate the relationship between budgetary participation and subordinates’ propensity to create slack. They proposed that subordinates who find budgetary participation useful are unlikely to jeopardise their participation privileges by creating slack, since detecting such activities could result in withdrawing these privileges.

Bryer’s (2014) study offered an anthropological multiple-case analysis of cooperatives in Argentina. It challenged conventional economic assumptions about accounting systems, employing a critical anthropological approach influenced by Marx’s “social praxis” and Latour’s “mode of existence.” Through case studies, it examined how varying levels of agency and participation in budgeting among actors lead to expanding ontological plurality, addressing tensions and structural conflicts.

Five of the 13 studies on participative budgeting connect to the most cited budgeting weaknesses. Table 3 maps these articles to the relevant weaknesses. This research addresses the practitioner’s concerns, particularly the use of unsupported assumptions, the lack of responsiveness, the strengthening of command and control, and the encouragement of gaming behaviour. However, most studies rely on experimental designs and focus on individual-level outcomes, offering limited insight into how participative budgeting affects broader organisational dynamics, such as whether it helps overcome departmental barriers or makes budgeting less time-consuming. This suggests that, while participative budgeting research has made relevant contributions, important gaps remain in its practical applicability.

3.3.2 Budgetary Slack

Budgetary slack is “the amount by which a subordinate understates his productive capability when given a chance to select a work standard against which his performance will be evaluated.” (Young, 2010, p. 831). Budgetary slack is a consequence of participative budgeting, which assumes subordinates truthfully communicate their private information in the budgeting process, which is useful for the central management of the organisation. This is the second-largest theme in this review, with nine studies, most of which (seven) are experiments conducted in the US. One exception is Davila and Wouters (2005), a case study involving four organisations. Two sub-themes were identified: (i) information asymmetry, and (ii) implication of individuals in budgetary slack.

Information Asymmetry

Two studies examined the information asymmetry problem in transactions where superiors and subordinates lack common information. Ideally, all parties in budgeting should act honestly and prioritise the organisation’s welfare. Rankin et al. (2008) explored how honesty and superior authority affect budget proposals by presenting budget requests factually and varying whether subordinates or superiors determined budgets. Findings showed that less slack occurred when subordinates set budgets with factual inputs, while no significant slack difference occurred when superiors made the final decision. The study implies that decentralising budgeting positively influences outcomes in organisations. Douthit and Stevens (2015) examined the impact of honesty on budget proposals, focusing on superiors’ rejection of authority. The first experiment revealed that honesty reduced budgetary slack when the subordinate was unaware of the superior’s pay. In the second experiment, honesty still influenced slack when the superior set the subordinate’s salary. Honesty did not affect strategic participative budgeting, which emphasised its significance only when subordinates lacked information about superiors’ pay.

The Implication of Individuals in Budgetary Slack

Several studies have investigated how personal responsibility, ethical judgment, and social context shape slack-related decisions. Davis et al. (2006) studied management accountants’ susceptibility to creating budgetary slack in violation of corporate policy. The study evaluated links between pressure effects, perceived responsibility, decision justifications, and underlying ethical dimensions. The results revealed that almost half of the participants violated explicit policy and created budgetary slack under obedience pressure. Those who added slack felt less responsible for their budget than those who refused to add slack. Most participants claimed that creating budgetary slack was unfair, unjust, and contrary to their duties.

Hartmann and Maas (2010) investigated business unit controllers’ inclination to create budgetary slack. They explored whether controllers involved in business units’ decisions are more susceptible to social pressure to create slack than controllers who are not. The results indicated that three factors, involvement in management, pressure from business unit managers, and personality, determine controllers’ engagement in creating slack.

Hobson et al. (2011) examined participants’ moral judgments about budgetary slack at the end of a budgeting experiment. Traditionally, these judgments were seen as fixed, regardless of financial incentives or social context. However, prior studies indicated that framing effects influence these moral judgments. This study supports the framing perspective in participative budgeting, suggesting that financial incentives shape the moral context while personal values affect individual responses.

Church et al. (2012) conducted two experiments on how shared interest in budgetary slack impacts budget report honesty. The study explored the advantages of sharing budgetary slack and how firms can reduce the negative effects on honesty. The first experiment revealed that managers report less honestly when misreporting benefits are shared with others. The second experiment assessed whether managers’ honesty is influenced by the preference of those who benefit from slack. The results indicated that managers report more honestly when aware of an employee’s preference for honesty.

Later, Church et al. (2019) studied the relation between slack and honesty. This experimental study investigated how managers’ budget reporting is influenced by (i) the measurement basis used in budget preparation, and (ii) managers’ slack benefits in budget execution. The results showed that the financial measurement basis increases misreporting by strengthening the desire to pursue self-interest. However, the absence of direct slack benefits increases misreporting by attenuating individuals’ moral concerns.

Altenburger (2020) then studied the impact of managers’ moods on their budget reporting. Based on a laboratory experiment, the study demonstrated that managers in a positive mood report their budget more honestly than managers in a negative mood. A neutral mood state does not increase honesty sufficiently to balance out the effect of the negative mood state.

Among the nine studies on budgetary slack, five demonstrated a connection to budgeting weaknesses. Table 4 maps these studies against the relevant weaknesses. This research responds to practitioners’ concerns about gaming behaviour and making employees undervalued. However, few studies directly addressed broader structural issues, such as the reinforcement of departmental barriers or the unsupported assumptions, suggesting that empirical slack research has focused more on behavioural mechanisms than systemic reform.

3.2.3 Beyond Budgeting

Beyond Budgeting, introduced by Hope and Fraser (1997), proposes replacing traditional budgeting with more adaptive, decentralised management models. Since both Beyond Budgeting and the budgeting weaknesses emerge from practice, it seems relevant to investigate whether studies of a practice-based budgeting approach align with practitioners’ concerns. In this literature review, six articles focused on Beyond Budgeting. Four studies occurred in Scandinavia, one in a German-speaking country and one in North America. Two streams of interest among these studies can be identified: (i) the abandonment of budgeting, and (ii) the impact of Beyond Budgeting on organisations.

Abandonment of Budgeting

Libby and Lindsay (2010) surveyed budgeting practices to assess their relevance and found that 80% of respondents use budgeting as a control tool, and 94% of those did not intend to abandon it. Most respondents viewed budgeting as value-added. This study analysed four main budgeting weaknesses, and the findings show that North American respondents do not share these concerns.

Later, Ekholm and Wallin (2011) examined how uncertainty and strategy affect the usefulness of fixed and flexible budgeting, distinguishing between the two. They found a significant negative association between environmental uncertainty and the usefulness of traditional annual budgets, while no significant association was found with flexible budgets.

Becker (2014) explored the abandonment of budgeting through multiple case studies in German-speaking countries. It focused on abandoning traditional budgeting in favour of Beyond Budgeting. The study analysed how the abandonment process has occurred and how sustainable it is.

Impact of Beyond Budgeting on Organisations

Østergren and Stensaker (2011) examined Beyond Budgeting in practice through a case study. The findings indicate that Beyond Budgeting alters the relationship between corporate and division managers to create new dependency lines. Implementing Beyond Budgeting leads to three main elements: (i) targets become more strategic and based on higher ambitions; (ii) there is greater focus on the big picture; and (iii) rules of action are perceived as an increased focus on possibilities and flexibility. After implementation, the role of the controller becomes more influential.

Henttu-Aho and Järvinen (2013) explored how institutionalised practices, such as budgeting, change over time, and examined the implications of such changes for the budgeting function. The results show that the traditional budgeting roles, such as planning, control, and target-setting, find a different place in those organisations that have changed their budgeting processes. The study also supports the finding of Østergren and Stensaker (2011) that organisations transition gradually to Beyond Budgeting, as it is a long process.

Bourmistrov and Kaarbøe (2013) studied the changes in management control systems that result from implementing Beyond Budgeting. Their case study suggests that many organisational issues stem from budgeting. The study illustrates how redesigned MCSs move decision-makers from their comfort zone to stretch zones, affecting their information needs. Implementing Beyond Budgeting fosters more entrepreneurial managerial work, urging managers to use new information to enhance their interaction with internal and external environments.

Three of the six studies on Beyond Budgeting demonstrate a connection to budgeting weaknesses. Table 5 maps these studies against the relevant weaknesses. Together, they show that Beyond Budgeting responds directly to concerns about budgeting being time-consuming, offering little value, lacking responsiveness, and having limited strategic focus. By shifting emphasis towards decentralised control and continuous adaptation, these studies also counter vertical command and control reinforcement. However, much of this evidence remains context-specific and drawn from early adopters, particularly in Scandinavia. Moreover, few studies assess whether Beyond Budgeting addresses other persistent weaknesses, such as reinforcing departmental barriers or undervaluing employees. While Beyond Budgeting research reflects several practitioners’ concerns, its broader relevance and impact remain limited in scope and generalisability.

3.3.4 The Other Research Themes

Thirty studies in this review fall outside the three dominant themes but offer insights into specific aspects of budgeting practice. These are grouped into smaller sub-themes based on their primary focus: (i) budgetary control, (ii) budgetary negotiations, (iii) budget reporting, (iv) budget process, (v) budgeting role, (vi) target setting, and (vii) other sub-themes.

Budgetary Control

Armstrong (2011) linked workplace bullying to budgeting behaviours, stating that budgetary controls can enable managerial bullying. He claimed that budget constraints create a toxic environment, allowing managers to manipulate financial metrics for psychological control, fostering fear and compliance. Budget targets exemplify this manipulation, undermining employee morale and organisational health.

Bedford et al. (2022) investigated the relationship between budgeting and employee stress during the COVID-19 pandemic. They found that financial pressures increase role conflict and uncertainty, negatively affecting employee morale and productivity. This highlights the negative human impact of budgeting, including increased employee stress, especially during periods of crisis.

Deore et al. (2023) investigated the impact of management controls on honesty in managerial reporting. The study argued that robust control systems, which include comprehensive performance evaluations and accountability mechanisms, can enhance the integrity of financial disclosures by reducing opportunities for dishonest reporting. This research demonstrated how budgeting can incentivise dishonesty and examined how management controls influence this.

Budgetary Negotiations

Fisher et al. (2006) investigated budget negotiations across periods, highlighting how past budget results influence current negotiation strategies. Experiments with students showed that superiors and subordinates react predictably to previous negotiation outcomes. The paper recommends improving negotiation by setting clear objectives, building trust, and using iterative techniques to adapt to circumstances.

Arnold and Gillenkirch (2015) studied how negotiated budgets impact organisational planning and performance evaluation. They showed that involving managers in budgeting boosts commitment and accountability, leading to improved performance. Results indicate that negotiated budgets promote better communication and goal alignment, facilitating effective resource allocation and evaluation. The findings underscore the significance of participative budgeting for organisational effectiveness.

Arnold (2015) studied the effects of superiors’ exogenous constraints on budget negotiations. The study suggests that such constraints, like policies, market conditions, or financial limits, lead to rigid negotiation strategies, impacting flexibility and outcomes. It concludes by highlighting the importance of recognising external factors in budgeting to improve negotiation outcomes and communication between managers and teams.

Budget Reporting

Brown et al. (2014) examined the impact of rankings on honesty. The results show that when managers know their reports will be ranked, they tend to report dishonestly to improve their position. They highlight that competitive ranking pressure can undermine honesty, suggesting organisations should consider the implications of these systems for reporting integrity. The findings emphasise the need for balanced performance evaluations, encouraging honesty and accountability.

Nikias et al. (2010) investigated how aggregation levels and budget information timing impact budgeting and decision-making. They found that aggregation influences decisions, with disaggregated data providing better insights. Timely budget information also improves decision-making. The study concludes that organisations should consider these factors in budgeting to enhance performance and resource management.

Kuang et al. (2023) investigated how subordinates’ budget reporting in hierarchical organisations affects their perceived social distance from their direct manager. Their two experiments reveal that reduced social distance initially increases subordinates’ honesty but decreases as the manager’s stake in the residual claim drops. Additionally, subordinates’ concern for the manager’s economic well-being and the manager’s perception of their reporting behaviour influence these outcomes.

Budget Process

Kramer and Hartmann (2014) examined how budgeting approaches impact budgetary slack and managerial performance. They applied social exchange theory to explore how top-down (TD) and bottom-up (BU) budgeting affect manager-organisational relationships. The study reveals that TD creates economic pressure, while BU promotes collaboration and trust, improving performance. Thus, the choice of budgeting orientation influences social and economic exchanges, affecting budgetary outcomes and managerial behaviour.

Sharma and Frost (2020) explored the role of social capital in shaping organisations’ budgeting processes. Social capital arises when people collaborate and achieve more than they could individually. The authors found that higher levels of social capital promote improved communication and collaboration, resulting in more effective budgeting practices and enhanced organisational performance.

Budgeting Role

Frow et al. (2010) examined the concept of continuous budgeting to balance the need for flexibility in budget management with maintaining control over financial resources. The authors argue that traditional annual budgeting processes often lack responsiveness to changing organisational environments, resulting in inefficiencies and misalignment with strategic goals. Continuous budgeting facilitates adjustments and real-time feedback, allowing organisations to adapt to fluctuations and uncertainties while adhering to control mechanisms.

Hansen and van der Stede (2004) argue that budgeting is more than a financial aspect; it is also about communication, motivation, and control. Their analysis reveals how these elements shape managerial behaviour and decision-making. Budgeting aligns organisational goals with individual performance, promotes departmental coordination, and fosters accountability. The authors emphasise understanding budgeting’s various functions to boost effectiveness and address the weakness of rigidity. Their findings indicate that a comprehensive view of budgeting enhances organisational performance and adaptability.

Target Setting

Aranda et al. (2014) examined how relative target setting (RTS) affects organisational and budgetary practices and performance outcomes. The study analysed data from various branches of a large travel retailer, revealing that managers consider the performance of similar units when establishing their targets, which leads to a phenomenon known as ‘ratcheting’. This occurs when past performance influences future targets, often placing increased pressure on managers to meet higher expectations. The findings suggest that while RTS can motivate improved performance, it may also lead to unintended consequences, such as budgetary slack and reduced honesty in reporting.

Fukushima and Yamada (2023) examined the connection between budget target setting and managers’ propensity for unethical behaviour. The study finds that when budget targets are perceived as excessively challenging, managers may resort to unethical practices to meet them, driven by the pressure to achieve performance metrics tied to compensation and job security. The authors stress that organisations must balance target difficulty with ethical considerations to prevent the emergence of unethical behaviours.

Other Subthemes

Huang and Chen (2009) examined how leadership in budgeting impacts managerial attitudes and dynamics in Taiwanese corporations. They highlighted behaviours like supportiveness and communication that foster a positive budgeting environment, improving attitudes and reducing strategic manipulations. The study emphasises the importance of effective budgetary leadership in promoting a collaborative culture and enhancing organisational performance.

Arnold and Artz (2018) analysed the use of single versus separate budgets for planning and performance evaluation. They argued that a single budget simplifies processes but may lead to conflicts and reduced motivation, while separate budgets improve accountability and reduce slack. The study emphasises the need for organisations to balance flexibility, control, and performance outcomes in their budgeting strategies.

Grabner and Moers (2021) explored factors influencing budget reallocations and their impact on performance. They identified key determinants such as organisational structure, strategic priorities, and external factors. Their findings suggest that reallocations align resources with strategic goals but can disrupt established processes. The study emphasises understanding the motivations behind reallocations and their effects on managerial decisions, contributing to budgeting literature by highlighting the need for flexible budgeting practices to adapt to change.

Using a configurational approach, Sponem and Lambert (2016) examined how budget characteristics affect managers’ roles and satisfaction. They found that different budget configurations lead to varying satisfaction levels, suggesting that a one-size-fits-all approach is ineffective. The authors advocate for customised budgeting practices tailored to organisational contexts and managerial needs, emphasising the importance of nuanced budget characteristics in enhancing budgeting literature.

Chong and Mahama (2014) examined how different budgeting approaches affect team performance. They distinguished between interactive budgeting, which enhances communication and collaboration, and diagnostic budgeting, which focuses on performance measurement. The study shows that interactive budgeting boosts team cohesion and effectiveness, while diagnostic budgeting, though important for accountability, lacks engagement. The authors recommend prioritising interactive budgeting for improved team dynamics and effectiveness, highlighting its role in promoting teamwork and achieving organisational goals.

Douglas et al. (2007) explored how ethical positions and national culture affect budgetary systems by examining the perspectives of Egyptian managers in US and local firms. Significant differences are found, with US managers holding more relativistic views than their Egyptian counterparts, who are more idealistic. These differing orientations influence budgeting practices and decision-making. The findings indicate that cultural context and ethical frameworks significantly shape managerial behaviour in budgeting, contributing to the broader discourse on national culture’s impact on accounting practices.

Marginson and Ogden (2005) investigated how budgetary targets help managers navigate uncertainty and ambiguity in their roles. The authors argued that clear budget targets provide a framework that enhances decision-making and accountability, enabling managers to cope with the uncertainties of their environments. The study concludes that managers with specific targets are more likely to engage in proactive budgeting behaviours, resulting in improved performance and alignment with organisational goals. This research highlights the importance of structured budgeting processes in fostering effective management practices and alleviating the adverse effects of ambiguity.

Becker et al. (2016) examined how organisations adjust budgeting practices during economic downturns. They argued that crises prompt reevaluating traditional methods, leading to the adoption of flexible techniques like rolling forecasts and scenario planning. These approaches help organisations manage risks and allocate resources more effectively. The study highlights the importance of communication and collaboration, which enhance decision-making and resilience. The authors advocate for innovative budgeting strategies to improve crisis navigation and performance.

Hartmann and Maas (2011) explored how uncertainty affects controllers’ roles and budgeting in organisations. They stated that increased uncertainty transforms controllers’ roles from strict budget control to flexible management. In such environments, controllers facilitate insights and communication rather than just enforcing budgets. The study highlights that budgets should be used as control tools for strategic planning in uncertain times. Their findings recommend that organisations adopt dynamic budgeting methods to manage uncertainty better and enhance performance.

Jordan and Messner (2020) explored how forecast accuracy indicators improve organisational planning. They argued that these indicators help managers assess forecast reliability and make informed decisions. The case study shows that using these measures fosters accountability and continuous improvement. The study concludes that integrating forecast accuracy into planning enhances goal alignment and overall performance.

Arnold et al. (2008) compared two corporate budgeting approaches: the Groves mechanism and profit sharing. They analyse how these affect participants’ behaviour and outcomes using experimental methods, particularly with pre-play communication. The Groves mechanism, which aligns individual incentives with collective outcomes, leads to more efficient budget allocations than profit sharing. However, regardless of the mechanism, pre-play communication significantly impacts strategies and cooperation. The findings indicate that the Groves mechanism promotes honesty and efficiency, but communication dynamics critically shape budgeting outcomes.

Dunk (2007) examined the interplay between budgetary pressures for innovation, information systems (IS) quality, and departmental performance. The study posits that high budget pressure makes IS quality vital for decision-making and resource allocation. It finds that quality IS information can reduce the negative impacts of budget pressure on performance. In contrast, poor-quality information worsens challenges from budget constraints, resulting in lower performance outcomes. The study emphasises the need to invest in quality information systems to aid innovation and improve departmental results under financial limits.

Kobelsky et al. (2008) examine factors influencing IT budget allocation, identifying determinants like organisational size, strategic priorities, and the perceived importance of IT. Firms with a clear IT strategy allocate higher budgets, leading to improved efficiency and competitive advantage. Effective IT budgeting enhances decision-making and resource management. The authors stress the importance of aligning IT budgets with business strategy to maximise technological investment benefits.

Davila and Foster (2005) studied how startup growth relates to management control systems (MCS). They noted that as startups grow, complexity increases, requiring formal MCS for effective operations. Their findings emphasise that early MCS adoption enhances performance by providing structure and improving decision-making. Startups implementing MCS early are better equipped to handle challenges and achieve sustainable performance. The authors conclude that grasping MCS adoption dynamics is vital for startup success, especially transitioning to structured management practices.

Fauré and Rouleau (2011) analysed accountants’ and middle managers’ roles in budgeting processes. The study shows that these professionals facilitate stakeholder communication, ensuring budget decisions meet strategic goals. The authors emphasised that effective budgeting relies on accountants’ and managers’ strategic competence as they navigate complex dynamics and aid overall performance. The research highlights the need to foster these competencies to enhance budgeting and align with organisational objectives and goals.

Aranda et al. (2019) analysed how subjective bonuses impact target setting in budget-based incentive contracts. These bonuses boost motivation and performance by providing flexibility in assessing contributions. The study reveals that organisations using subjective bonuses align individual efforts with organisational goals, fostering collaboration. However, the authors warn that the success of subjective bonuses hinges on clear communication of performance expectations and evaluation criteria. The research highlights the importance of balancing objective and subjective measures in budgeting to enhance employee performance and engagement.

Among these 30 studies, nine are connected to at least one of the most cited budgeting weaknesses. Table 6 maps these studies accordingly. This diverse body of research addresses a wide range of practitioners’ concerns, particularly the encouragement of gaming behaviour, unsupported assumptions and guesswork. Several studies also contribute to employees being undervalued, and constraining budgeting responsiveness. However, this work is fragmented and often limited to narrow organisational contexts or behavioural insights. While these studies enrich the literature, their scattered focus and lack of integration into the examination of broader budgeting reforms suggest that practitioners’ concerns remain only partially addressed outside the dominant themes.

4. Reflections and Research Opportunities

This section identifies gaps and research opportunities across the budgeting literature reviewed. By reflecting on how empirical studies address or fail to address practitioners’ concerns, several avenues for advancing budgeting research emerge. These opportunities span theoretical development, methodological improvement, and closer alignment with practitioners’ concerns. Addressing them is essential to strengthening the field’s relevance and enhancing its impact on management accounting practice.

4.1 Addressing Budgeting Weaknesses through Research

The budgeting literature reflects practitioners’ concerns about budgeting. Studies on participative budgeting tell us that sharing information between superiors and subordinates positively impacts individual performance and helps mediate their relationship. In addition, when subordinates prepare the budget, the welfare of the superiors is higher, and the slack is lower. Lau and Eggleton (2003) reported that subordinates who find participative budgeting useful are unlikely to jeopardise their participation by engaging in slack or sharing false information.

Research on budgetary slack contributes to illuminating the conditions under which budgeting encourages gaming behaviour. Studies by Davis et al. (2006), Hobson et al. (2011), and Church et al. (2012, 2019) demonstrated that pressure to meet targets, moral framing, and incentive structures strongly influence the likelihood of slack creation. Hartmann and Maas (2010) further showed how internal pressure from business unit managers can lead controllers to engage in slack, especially in role conflict or low moral resistance.

Beyond Budgeting research offers an alternative model for handling the weaknesses of budgeting. Østergren and Stensaker (2011) and Bourmistrov and Kaarbøe (2013) provide case-based insights into how abandoning or reframing traditional budgeting can improve responsiveness, strategic alignment, and decentralised decision-making, countering vertical command-and-control reinforcement. However, these studies also revealed that the transition to Beyond Budgeting is far from straightforward. Henttu-Aho and Järvinen (2013) found that legacy systems, institutional expectations, and path dependence constrain transformation, suggesting that while Beyond Budgeting may mitigate several weaknesses, its implementation remains selective and gradual.

Despite this, gaps remain in how the budgeting weaknesses are explored and addressed. Future research can help close this gap by focusing on three major areas: unreliability, command-and-control structures, and organisational and people-related issues.

Firstly, regarding budget unreliability, such as outdated assumptions, time consumption, and limited adaptability (Hansen et al., 2003; Neely et al., 2001), future studies could examine how different budgeting methods, including rolling budgets and activity-based budgeting, influence the timeliness and relevance of budgetary information (Hansen, 2011). Case studies exploring the role of information technology, business analytics, and dynamic forecasting tools in enhancing budget responsiveness would also be valuable (Rikhardsson & Yigitbasioglu, 2018).

Secondly, the weaknesses of vertical command-and-control structures suggest that traditional budgeting can stifle initiative and responsiveness (Hansen et al., 2003). Research on participative budgeting (e.g., V. K. Chong & Johnson, 2007; Wong-On-Wing et al., 2010) indicates potential for mitigating these concerns. However, more work is needed to understand how participative processes, hybrid models, or Beyond Budgeting principles reshape decision-making authority and strategic agility within organisations (Østergren & Stensaker, 2011).

Thirdly, organisational and people problems, such as reinforcing departmental barriers and encouraging gaming behaviour, remain underexplored. Future research could investigate how budgeting systems interact with power dynamics, intra-organisational competition, and internal incentives, shaping behaviours that undermine coordination and shared accountability.

Addressing these practitioners’ concerns through empirical investigation can strengthen budgeting research’s theoretical robustness and practical relevance.

4.2 Expanding beyond Traditional Themes

Much of the empirical budgeting literature continues to focus on traditional themes, particularly participative budgeting and budgetary slack. While these areas remain important, future research should broaden its focus to address the evolving organisational environment. Regarding participative budgeting, further studies are needed to examine how participation mechanisms influence actual budget outcomes, especially information sharing, employee empowerment, and strategic alignment (e.g., V. K. Chong & Johnson, 2007; R. J. Parker & Kyj, 2006). Similarly, research on budgetary slack could examine how slack is formed, utilised, and mitigated within evolving organisational contexts. As firms undergo digital transformation, embrace more agile structures, and face increasing uncertainty, the functions and risks of budgetary slack may change, warranting renewed attention to its role in enabling adaptability, innovation, or opportunism.

Beyond Budgeting research offers an alternative perspective but remains underdeveloped. Studies such as Østergren and Stensaker (2011) and Bourmistrov and Kaarbøe (2013), illustrated Beyond Budgeting’s potential. However, conceptual clarity is still lacking. Future research should clarify the meaning of Beyond Budgeting, explore its adaptation across cultural contexts, and assess its impact on organisational performance and employee behaviour.

The narrow focus on participative budgeting and budgetary slack leaves practitioners’ concerns underexplored. For instance, time-consuming, infrequent updates, and lack of strategic focus are among the most frequently cited weaknesses; however, they are only addressed peripherally in empirical studies. Frow et al. (2010), Becker et al. (2016), and Bedford et al. (2022) provided exceptions by examining how organisations modify budgeting practices during periods of crisis or change. These studies suggest that flexible budgeting tools, such as rolling budgets, scenario planning, and continuous budgeting, can alleviate the rigidity and delay associated with traditional annual cycles. However, this focus has received limited attention in empirical research. Broadening the scope of research beyond traditional themes will strengthen the theoretical foundations of budgeting studies and provide more nuanced, practice-oriented insights for scholars and practitioners.

4.3 Methodological Improvements in Budgeting Research

A notable characteristic of the budgeting literature is the heavy reliance on experimental designs, particularly those using student samples (e.g., Davis et al., 2006; Hobson et al., 2011). While such studies provide valuable behavioural insights, they limit the generalizability of findings to real-world organisational settings. Greater methodological variety is essential to advance the field. Case studies such as Davila and Wouters (2005), Østergren and Stensaker (2011), and Bourmistrov and Kaarbøe (2013) offer richer perspectives on budgeting as an evolving social and organisational process.

Geographic diversity also represents an important methodological opportunity. Most empirical budgeting research has been conducted in North America and Western Europe, with few studies examining budgeting practices in other regions (e.g., Bourmistrov & Kaarbøe, 2013; Bryer, 2014). Investigating how cultural, institutional, and economic differences shape budgeting behaviour and effectiveness would enhance the global relevance of budgeting theories.

Additionally, future studies could apply longitudinal designs to capture how budgeting practices evolve, especially in response to environmental uncertainty, technological change, or organisational restructuring. Methodological innovation, including mixed-methods approaches, can enrich the theoretical development of budgeting research and better connect it with practitioners’ concerns.

4.4 Strengthening the Link Between Practice and Academia

A persistent theme across budgeting research is the need to bridge the gap between academic studies and practitioners’ concerns (Chapman & Kern, 2012; Hansen et al., 2003; Tucker & Parker, 2014). While many studies acknowledge practitioners’ concerns, few directly align research questions with organisations’ practical challenges.

Future research should prioritise designing studies that explicitly engage with issues identified in practitioner literature, such as budgeting’s responsiveness to change, strategic alignment, and organisational empowerment (Neely et al., 2001; Selto & Widener, 2004). This requires more than adjusting research questions; it involves rethinking the role of budgeting in organisations.

Moreover, developing frameworks integrating budgeting practices, such as activity-based budgeting or rolling budgets, would make academic research more actionable for practitioners. Strengthening the dialogue between academia and practice can enhance the impact, relevance, and contribution to management accounting as an applied field.

Future research should address both conceptual gaps and practical challenges in budgeting. By deepening our understanding of budgeting processes, roles, and outcomes, and engaging more closely with practitioners’ concerns, scholars can enhance the relevance and impact of budgeting research. Bridging the gap between theory and practice remains essential for advancing management accounting as an applied discipline.

5. Conclusions

Two decades have passed since Luft and Shield’s (2003) and Covaleski et al.'s (2003) literature reviews. Both reported that academic research has focused on traditional issues, such as participative budgeting. Hansen et al. (2003) observed the lack of practice-led research literature, a gap this literature review aims to revisit by evaluating whether management accounting research since 2003 has addressed the budgeting weaknesses.

This literature review aims to firstly synthesise the budgeting literature since the work of Luft and Shields (2003), highlighting its importance as a research subject. Secondly, to identify research themes and highlight gaps where academic research diverges from practitioners’ concerns. Thirdly, to evaluate how these studies engage with the budgeting weaknesses. Lastly, to provide a roadmap for future studies, emphasising the importance of addressing the role of budgeting in dynamic and uncertain environments. A systematic review of 59 empirical studies has revealed three main themes: participative budgeting, budgetary slack, and Beyond Budgeting. These themes provide a structure for assessing academic engagement with budgeting criticisms.

The studies were analysed against the budgeting weaknesses using Figure 1 as a framework. Participative budgeting and budgetary slack are conceptually linked, but research provides limited evidence to address these gaps. In contrast, Beyond Budgeting aligns with budgeting weaknesses, as it addresses practitioners’ concerns, showcasing it as a potential solution.

The studies reviewed do not encompass all potential research avenues in budgeting. Research into the budgeting process could clarify claims about its time-consuming nature and infrequent renewal. Studies of budgeting functions could clarify claims regarding the imposition of vertical command-and-control structures. Finally, studies on the operationalisation of budgeting could clarify organisational and people budgeting issues.

A research agenda is insufficient to bridge the gap. While some studies have addressed the disconnect between research and practice, suggesting solutions or justifying its existence. Recent advancements, such as activity-based budgeting and Beyond Budgeting, have emerged from practice. To remain relevant, the field must shift its mindset. Researchers should prioritise studies that foreground practitioners’ concerns, adopt flexible methodologies, and embrace the complexity of organisational budgeting. Survey-based research and longitudinal case studies offer promising avenues for reconnecting budgeting research with its practical roots.

This review contributes by mapping budgeting research since 2003 and analysing the research against budgeting weaknesses. While gaps remain, the review shows that budgeting weaknesses have often been mentioned in the literature and that the Beyond Budgeting literature does engage with the practitioners’ concerns. This review encourages a renewed dialogue between academia and practice by mapping where progress has been made and where further inquiry is needed. Advancing budgeting research in this direction can enhance its relevance, contribution, and impact in dynamic organisational environments.