1. Introduction

The past two decades have witnessed significant growth in the number of Chinese companies publishing corporate social responsibility (CSR) reports. According to Yin et al. (2019, 2022), only four CSR reports were published in 2004, while 1,751 in 2013 and 2,648 in 2022. Moreover, the recently updated listing requirements (in April 2024) by Chinese stock exchanges indicate that CSR reporting in China is in transition from voluntary to mandatory. This change could have a profound global impact, as China pursues more sustainable economic development, aligns with wider stakeholder groups beyond domestic ones, and contributes to the United Nations’ sustainable development goals (SDGs) (Shen et al., 2020). The Chinese context features centralised control derived from its one-party leadership system, which significantly impacts political and social policies and allows for rapid implementation of economic reforms and development strategies. This system has contributed to China’s remarkable economic growth over the past few decades. Meanwhile, the regulatory environment in China is characterised by strong government intervention in markets and industries, thus steering the country through modernisation and globalisation while maintaining sociopolitical stability (Feng, 2013; T. Li et al., 2023). This unique sociopolitical context has significantly influenced the development of CSR reporting in China. The government’s overriding role in economic, political, and social activities often sets the tone for CSR, where companies are expected to align their responsibilities with national policies and development strategies (such as poverty alleviation and environmental protection) (T. Li et al., 2023; T. Li & Belal, 2018).

The development of CSR reporting in China has triggered academic research in this area. There is a body of literature exploring CSR reporting in China, which is linked to the country’s unique sociopolitical context, regulatory environment, and globalisation (see, for example, Marquis et al., 2015, 2017; Marquis & Qian, 2014; Parsa et al., 2021; Qian & Chen, 2021; Situ et al., 2021; X. Zhao et al., 2022). Studies show that Chinese companies increasingly implement CSR reporting to gain (political) legitimacy and ensure regulatory compliance. CSR reporting in China largely reflects alignment with the government’s political ideology (T. Li et al., 2023) rather than corporate responsibility, thus leading to a distinct aspect of Chinese corporate governance (Tang et al., 2020).

Despite the burgeoning practice and research, a notable synthesis gap (that is, according to Booth et al. (2021), the lack of consolidation of existing studies, findings, or theories into a coherent understanding, often due to a dearth of reviews summarising and synthesising relevant extant literature) exists in the influential factors of CSR reporting in China. The rapid development of CSR (along with recent trending concepts including sustainability, environmental, social and governance (ESG), and the SDGs) within China’s complex economic conditions requires a more nuanced understanding of influential factors of CSR reporting. The extant literature indicates various factors that influence the nature, extent, and process of CSR reporting in China, ranging from regulatory environments to political pressures, market incentives, stakeholder demands, social expectations, and corporate characteristics. However, there is a dearth of literature review studies that synthesise existing knowledge, identify (in)consistencies, and reveal areas lacking empirical evidence. Such review studies are essential to provide directions for future research, policymaking, and reporting practices. In this context, this paper aims to address the synthesis gap by investigating the research question (RQ), as follows:

What are the influential factors of CSR reporting in China and how do these factors influence the reporting practice?

The systematic review approach is used because it reduces researcher bias in relation to the inclusion and exclusion of studies and provides a transparent literature search process (Booth et al., 2021; Kunisch et al., 2023).

The present review maps the landscape of existing research on influential factors of CSR reporting in China and catalogues the factors into three categories: corporate characteristics, general contextual factors, and internal contextual factors (Adams, 2002). By synthesising existing research and identifying convergence and divergence, this review contributes to the research field by enhancing the understanding of contextual specificities in China and thus informing the theoretical and practical development of CSR reporting using insights from the Chinese context. It systematically addresses the synthesis gap by offering a comprehensive picture of factors influencing CSR reporting, highlighting the dearth of (qualitative) studies exploring general and internal contextual factors, and identifying the limited understanding of the interrelation and interaction between the three categories of factors. Based on the synthesised evidence, this review offers recommendations for future research areas that could further enhance the understanding and practice of CSR reporting in China and beyond. It provides a research agenda for scholars to explore how changing regulatory environments and trends in CSR and sustainable development further shape reporting practices, thus filling research gaps in regional disparities and methodological weaknesses in previous studies.

The remainder of this paper is structured as follows. Section 2 introduces SLR as the method of this research and explains how it has been conducted. Section 3 presents and analyses the SLR results. Section 4 discusses the systematic review findings and addresses the RQ. Section 5 recommends new areas for future research based on gaps identified in the existing body of literature on CSR reporting in China. Section 6 concludes this paper and discusses research limitations.

2. Research Method: Systematic Literature Review

A systematic literature review (SLR) refers to a research method for identifying, critically appraising, and synthesising all relevant empirical studies on a specific topic, through explicit and systematic strategies that minimise bias, to generate reliable findings and inform decision-making (Booth et al., 2021; Kunisch et al., 2023). It is widely used by researchers and academics in scientific literature reviews as it can provide an overview of the current state of knowledge in a specific topic area, with minimal potential bias (Booth et al., 2021; Farisyi et al., 2022). For an SLR to be impactful, the focus topic area should feature both “synthesis gaps” and “research gaps” (Booth et al., 2021, p. 74). As mentioned earlier, empirical evidence of factors influencing CSR reporting in China remains inconclusive in the extant literature (i.e., a research gap). Meanwhile, to our best knowledge, there is a lack of literature review studies on the topic (i.e., a synthesis gap). Noronha et al. (2013) and Guan and Noronha (2013) reviewed CSR reporting in China and called for more empirical research in this area. Given that both the reviews were published more than 10 years ago, their review findings may need updates. A recent review study by Shen et al. (2023) focused on the practice and research on ESG in China and called for future research on the impact of the unique Chinese context on ESG. So far, no study focuses on systematically reviewing the influential factors of CSR reporting in China.

This paper aims to address the gaps through an SLR, based on the approaches introduced by Booth et al. (2021), Kunisch et al. (2023), and Hiebl (2021). The SLR includes the following stages, which are further explained in the subsequent subsections:

-

Design: setting scope, RQ, and inclusion criteria for studies

-

Literature selection: identification, screening, and disclosure (see Figure 1 later)

-

Data collection, extraction, analysis, and synthesis

2.1 Design

The scope of the current review is limited to extant empirical studies on influential factors of CSR reporting in China in the past two decades. The research period (i.e., from 2004 to 2023) covers the development of CSR reporting practice in China so far. Informed by the RQ, the following inclusion criteria (IC) were applied in the literature selection process:

-

IC1: original research papers written in English and published in peer-reviewed academic journals from 2004 to 2023

-

IC2: empirical studies using quantitative, qualitative, or mixed research design

-

IC3: empirical studies investigating the influential factors of CSR reporting in China

In terms of IC1, only research written in English was included because it is a common academic language worldwide. Only original research papers published in peer-reviewed academic journals were selected as this could ensure the quality of included studies (Booth et al., 2021). Therefore, books, book chapters, conference proceedings, doctoral theses, and dissertations were excluded from this review. For IC2, the current review focused on empirical studies using a quantitative, qualitative, or mixed research design. In other words, literature review papers were excluded. IC3 assessed the relevance of studies to the RQ. Notably, in this review, the term “CSR reporting” refers to corporate reporting on economic, environmental, and social impacts. It is the terminology commonly used by the Chinese corporate reporting community (G. Yin et al., 2022). In practice, the terms “CSR reporting,” “sustainability reporting”, and more recently “ESG reporting” are sometimes used interchangeably. The use of different terms to refer to CSR reporting was considered during the literature searching process. The three ICs were applied in the process of literature selection explained in the next subsection.

2.2 Literature Selection

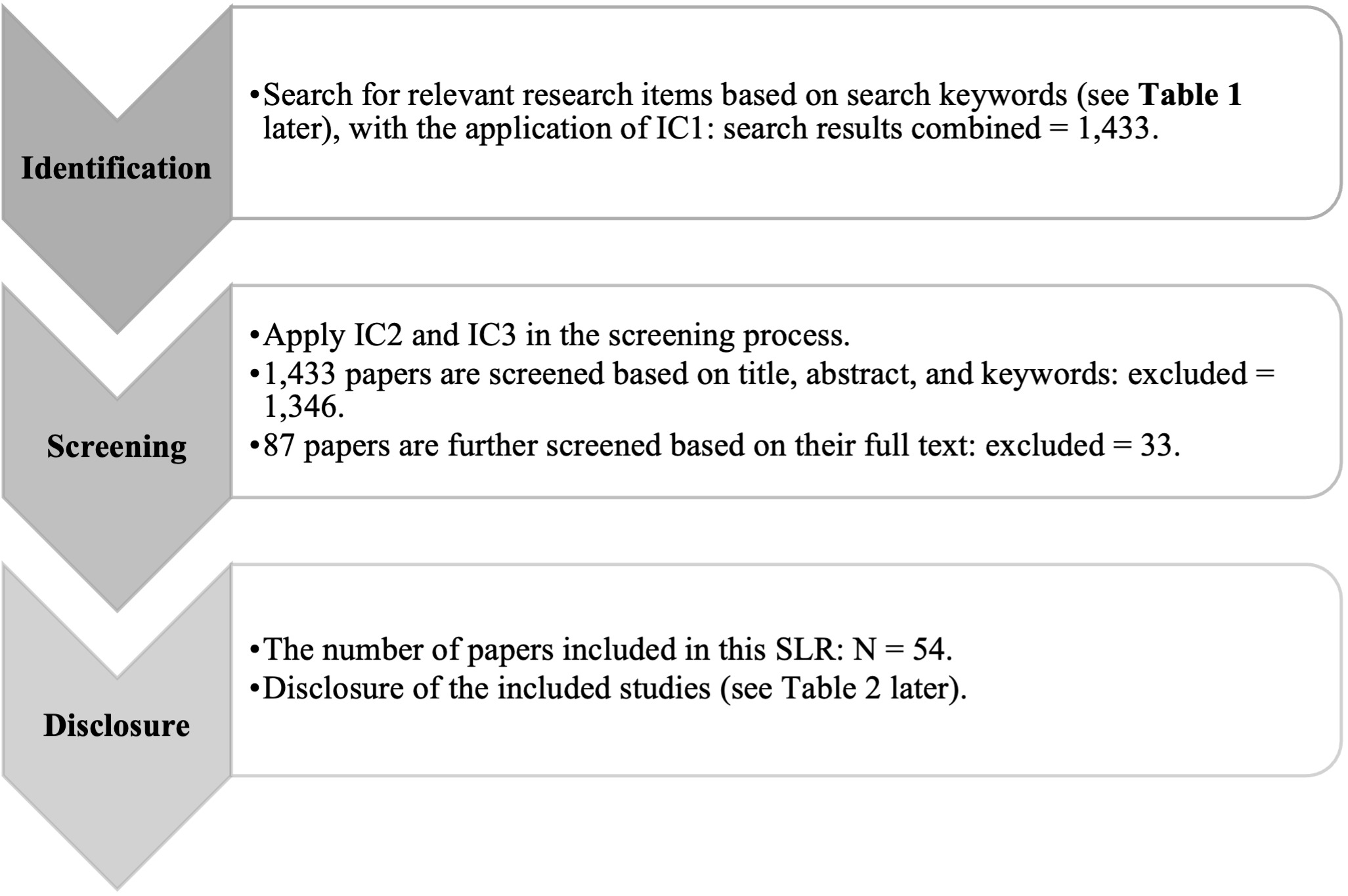

The literature search was conducted on Elsevier (SCOPUS), an online database including large repositories of academic studies (with more than 23,500 peer-reviewed journals) (Farisyi et al., 2022). Drawing on Hiebl (2021), Figure 1 shows the process of literature selection, which includes three steps: identification, screening, and disclosure. The identification step involved searching for research papers that were potentially relevant to the RQ on SCOPUS through predefined keywords.

Keywords for the literature search were defined based on the review topic area, namely, the influential factors of CSR reporting. Drawing on a seminal work by Adams (2002), the influential factors of CSR reporting can be classified into three categories: corporate characteristics, general contextual factors, and internal contextual factors. Under each category, a list of factors is believed to be influential in determining the nature, extent, process, and quality of CSR reporting (Adams, 2002). In case there were factors missed by Adams (2002), we also referred to other relevant literature review papers including Ali et al. (2017), Arkoh et al. (2024), Farisyi et al. (2022), Fifka (2013), and Hahn and Kühnen (2013). The influential factors identified were summarised and used as search keywords (Table 1) after being amended to be tailored to the research context of this review.

Through this structured search, we tried to exhaust the already known influential factors of CSR reporting and capture potentially relevant research items. It allowed for comprehensive coverage of the extant literature on influential factors of CSR reporting based on pre-existing beliefs (Hiebl, 2021). Four more general terms (“factor*” OR “motivation*” OR “driver*” OR “determinant*”) were used as search keywords to identify any other potentially relevant research items free from pre-existing beliefs. Such openness in the identification step was important, as it ensured that an unbiased and representative SLR sample could be generated, and the key findings of the current review could be generalised about the influential factors of CSR reporting in China (Hiebl, 2021). The search keywords defining CSR reporting include “CSR report*” OR “CSR disclos*” OR “environmental report*” OR “ethical report*” OR “responsibility report*” OR “responsible report*” OR “social report*” OR “sustainability report*” OR “sustainable report*” OR “ESG report*” OR “environmental, social, and governance report*”, acknowledging the differences in the terms used to refer to CSR reporting as much as possible.

The identification step, with the application of IC1, resulted in 1,433 potentially relevant research papers. They were prepared for screening and analysis of their content fit for addressing the RQ (Booth et al., 2021; Hiebl, 2021). According to IC2 and IC3, the papers were explored and selected based on titles, abstracts, and keywords; 1,361 papers were excluded. Then, all the papers not eliminated in the previous selection were explored and selected through full-text reading while adhering to IC2 and IC3. Also, not fully accessible research papers were excluded from the current review. After applying all inclusion and exclusion criteria, the final SLR sample (N = 54) was generated. The included studies are categorised and listed in Table 2 (later in Section 3, Results). The disclosure of the full list of included studies ensures the transparency of the basis for this SLR’s results and findings (Hiebl, 2021).

2.3 Data Collection, Extraction, Analysis, and Synthesis

The data were collected, extracted, and summarised manually through a thorough reading of all included studies. For each included study, data extracted included authors, paper title, year of publication, journal name, abstract, keywords, research methods, empirical data, CSR reporting factors, findings on the influence of factors on CSR reporting, practical implications, and future research recommendations. The next sections present the results of data analysis and synthesis and discuss key findings of the current review.

3. Results

3.1 Year of Publication

As for the year of publication of the SLR sample (54 included studies in total), Figure 2 illustrates the number of studies published over five-year intervals from 2004 to 2023. During the initial five-year period (2004–2008), no studies were published, indicating a lack of research on the influential factors of CSR reporting in China during these years. The next interval (2009–2013) shows a modest beginning, with five studies published. This suggests a nascent interest in the topic, possibly driven by new CSR guidelines and a growing awareness of CSR in China.

A surge is observed in the third interval (2014–2018), with 19 studies published. This surge reflects a growing interest in the topic, along with the continuous increase in the number of Chinese companies involved in CSR reporting (G. Yin et al., 2022). The number of studies published continuously increases, peaking at 30 in the most recent interval (2019–2023). Thus, the development of CSR reporting practice in China has been supported by a stable and growing body of research. Overall, the clear upward trend in the number of studies published indicates an increasing escalation in scholarly attention and academic investigation of the influential factors of CSR reporting in China.

3.2 Journal Title

Figure 3 presents a bar chart categorising the 54 studies by the journal where they were published. It reveals diverse publications, with Sustainability; Journal of Cleaner Production; and Sustainability Accounting, Management and Policy Journal representing the most popular journals (hosting nine, four, and four studies respectively). This suggests that these journals are key venues for disseminating research on CSR reporting in China. The distribution of studies across journals highlights some concentration of research in a few key journals while indicating a broad scope, with many journals contributing only one or two studies. The presence of numerous journals with a low number of studies might indicate research gaps or areas that have not yet gained significant attention. Furthermore, while Figure 3 indicates a core group of accounting journals, there are studies published in other business and management journals and journals in other research areas. This result indicates a need for more outlets to accommodate the growing body of research in CSR reporting.

3.3 Research Methodological Design

Research methodological designs are generally referred to as quantitative, qualitative, or mixed methods. In a quantitative or qualitative research design, one method (i.e., mono-method) or multiple methods can be adopted to address the research problem (Saunders et al., 2023). A mixed-method research design combines quantitative and qualitative approaches (Saunders et al., 2023). Figure 3 shows how the 54 included studies are categorised based on their research methodological designs.

The mono-method quantitative category comprises most of the included studies, with 44 studies making up 81% of the total (54 included studies). These studies rely solely on quantitative methods, indicating a preference for numerical data and statistical analysis in this field. However, no studies are categorised as multi-method quantitative. Two studies (4%) combine qualitative and quantitative approaches to provide a comprehensive analysis by integrating numerical data with contextual understanding. In terms of qualitative research design, eight studies (15%) employ qualitative research methods. These studies rely on textual data such as interviews, documents, and archives to provide a detailed understanding of CSR reporting practices in China. Specifically, seven studies (13%) follow a mono-method qualitative design, and one study (2%) uses multiple qualitative methods.

The pie chart in Figure 4 shows the predominance of mono-method quantitative studies, thus a focus on measurable outcomes and trends in investigating the influential factors of CSR reporting in China. Meanwhile, the representation of qualitative studies indicates an acknowledgement of the complex nature of CSR reporting, which cannot be captured by quantitative data alone. The presence of mixed-method studies, though very few, reflects some attempts to triangulate data for a more comprehensive understanding of the influential factors of CSR reporting. The absence of multi-method quantitative studies suggests a potential gap in the extant literature that future research can seek to address. The chart also suggests opportunities for future research to adopt multi-/mixed method designs to further enrich the nuanced understanding of CSR reporting dynamics in China.

3.4 Influential Factors Identified

Table 2 shows the specific influential factors, by category, identified from the 54 included studies. The identification of the influential factors initially followed a deductive approach, referring to the influential factors indicated in Adams (2002) and other relevant literature review papers – thus consistent with the approach followed to generate keywords for the literature search (explained in Section 2.2 and listed in Table 1). While reviewing each included study, the influential factors and relevant empirical findings were extracted. Each included study was read and reread by the two authors separately to ensure that all influential factors, with or without pre-existing beliefs, were identified and accurately recorded. Then, the influential factors identified were classified into three categories based on Adams (2002). For each influential factor, Table 2 shows the studies investigating it. Typically, an included study investigates more than one influential factor. Therefore, one included study can appear several times in different rows of the table. The next section discusses the identified influential factors and relevant empirical findings in detail.

4. Findings Discussion

4.1 Corporate Characteristics

4.1.1 Company Size

Company size is commonly considered an important corporate characteristic that influences CSR reporting practice in China. Studies investigating the relationship between company size and CSR reporting find that the larger the company size, the higher the likelihood of initiating CSR reporting (Anyigbah et al., 2023; Jan et al., 2021; Liang et al., 2022; Patten et al., 2015; Sun et al., 2022). Given their scale of business operation, larger companies are faced with more pressure from wider stakeholder groups. In response to the stakeholder pressure, larger companies tend to adopt CSR reporting to enhance information transparency (Liang et al., 2022; Sun et al., 2022). Patten et al. (2015) find that the extent of CSR reporting is positively related to the company size. That is, larger companies are more likely to disclose more CSR information. Specifically, Anyigbah et al. (2023) suggest that company size is positively related to economic and environmental reporting but insignificant to social reporting.

Notably, different definitions of company size can lead to different research results. For example, Sun et al. (2022) define company size as asset size and find that it has a negative but non-significant influence on the degree of integration of CSR disclosures. Jan et al. (2021) find that asset size is an important factor influencing the positive correlation between CSR reporting and corporate performance. If company size is measured by the total number of employees, it is positively correlated with animal welfare information disclosures (Sun et al., 2021).

4.1.2 Industry/Sector

Some previous studies on Chinese CSR reporting have focused on the manufacturing industry (Anyigbah et al., 2023; Chu et al., 2013; Dong et al., 2014). Chu et al. (2013) argue that companies in high carbon-emitting industries tend to disclose more greenhouse gas (GHG) information as they aim to enhance legitimacy. Dong et al. (2014) suggest that the Chinese Central Government exerts pressure on companies in the mining industry in terms of CSR reporting practices. Thus, the adoption of CSR reporting by Chinese mining companies is regarded as a response to governmental policies. Similarly, Anyigbah et al. (2023) highlight the fact that issues such as environmental pollution, harmful working conditions, and occupational injuries/diseases in mining and labour-intensive manufacturing industries have attracted increasing attention from various stakeholders and the general public. The Chinese government requires companies operating in these industries to adopt more sustainable practices and report their performance accordingly (Anyigbah et al., 2023).

Chu et al. (2013) note that within high carbon-emitting industries, state-owned enterprises (SOEs) tend to report less GHG information than their private counterparts. One possible reason is due to their hybrid nature, which means that these SOEs do not genuinely control their assets and thus are unable to make major decisions by themselves. Consequently, they tend to keep silent about investments in GHG/energy-reduction projects. Also, as SOEs are predominately controlled by the government, other stakeholders’ information demands are less frequently heard. The SOEs are less willing to disclose GHG information as they tend to ignore the information demand of minor stakeholders.

4.1.3 Company Age

Some previous studies define company age as the company life cycle (Anyigbah et al., 2023; Cherian et al., 2020; Jan et al., 2021; X. Zhao et al., 2022). Jan et al. (2021) find that the company life cycle has a positive moderating effect on the relationship between CSR reporting and the financial performance of Chinese-listed companies. CSR activities contribute to better financial performance, and better financial performance helps the companies stay in business. Moreover, Cherian et al. (2020) and Anyigbah et al. (2023) suggest a positive correlation between company age and CSR reporting. With maturity, companies are increasingly concerned about corporate reputation, thus are more likely to increase the level of CSR reporting.

Other studies define company age as the period of listing. Zheng et al. (2014) find that Chinese companies listed between 2008 and 2010 are more likely to disclose CSR information, due to the significant change in relevant stock exchange requirements in 2008. Conversely, Zhao et al. (2022) argue that company age is inversely associated with the likelihood of adopting CSR reporting, as companies with a longer history are less willing to issue CSR reports. A plausible explanation is that it is more difficult for those long-established companies to undergo radical changes in corporate reporting.

4.1.4 Financial/Economic Performance

A number of previous studies have investigated the relationship between CSR reporting and financial/economic performance. Previous empirical results commonly show that CSR reporting is positively related to corporate financial performance (Chang et al., 2022; Jan et al., 2021; Lu et al., 2015; Noronha et al., 2018; Sial et al., 2018). Companies showing better financial performance are more likely to adopt CSR reporting (Sial et al., 2018). In turn, CSR reporting, as a legitimate tool, tends to enhance corporate reputation and thus contribute to better corporate financial performance (Lu et al., 2015). Furthermore, the quality of CSR reporting positively influences corporate financial performance (Lu et al., 2015). Notably, there are studies showing different results. Wang et al. (2017) argue that corporate financial performance does not directly influence CSR reporting quality but significantly moderates the interactive effects of mandatory supervision and company size on CSR reporting quality. Chang et al. (2022) attempt to determine the relationship between CSR reporting and financial performance but find that the results won’t be conclusive without further exploration.

4.1.5 Debt Ratio

The findings on the relationship between debt ratio and CSR reporting remain inconclusive. Gallego-Álvarez and Pucheta-Martínez (2020) find that Chinese companies with a higher level of leverage tend to report less CSR information. Wang et al. (2021) explain that highly leveraged companies focus more on short-term financial goals than on long-term CSR goals. Conversely, Shaheen et al. (2023) find that financial leverage is significantly positively correlated with the level of CSR reporting. Cherian et al. (2020) argue that Chinese companies with a high leverage level tend to improve their CSR reporting due to an intention to meet the information demands of creditors and other stakeholders. With a sample of Chinese companies listed on the New York Stock Exchange, Ricardo and Florencio (2020) find that the relationship between CSR reporting and debt ratio is not significant. Moreover, some studies find that the quality of CSR reporting is negatively correlated with the cost of capital (Anyigbah et al., 2023; Cherian et al., 2020; Y. Li & Foo, 2015; Zheng et al., 2014). Companies with higher CSR reporting quality have significantly lower costs of capital, indicating that the cost of capital is an important channel for the market to price the quality of CSR reporting (Y. Li & Foo, 2015).

4.1.6 Political Ties

In China, political ties tend to significantly influence the nature, extent, and quality of CSR reporting (Chu et al., 2013; Dong et al., 2014; Gao, 2011; Liang et al., 2022; Shaheen et al., 2023; Zheng et al., 2014), given the Chinese government’s considerable control over key industries, particularly through SOEs. The Chinese government uses symbolic power to deepen political ideology into corporate practices and encourage companies to publish CSR reports in line with government guidance, thus accumulating symbolic capital and enhancing social status (Situ et al., 2021). The SOEs, and even non-SOEs, use CSR reports to signal compliance with state priorities, avoid possible regulatory scrutiny, and secure government endorsement (Dai et al., 2018).

Specifically, Gao (2011) finds that Chinese companies with strong political ties demonstrate higher enthusiasm when facing social issues, which may stem from their political sensitivity. Situ et al. (2021) further confirm that Chinese companies with strong political ties are more likely to produce robust CSR reports consistent with state strategies to maintain political legitimacy and secure state resources. When comparing the behaviours of SOEs with non-SOEs in politically authoritarian regimes, Wang et al. (2016) find that non-SOEs often limit their investments in CSR activities and disclosures, whereas SOEs perform better in implementing CSR activities and producing high-quality reports following government guidance. Also, Zheng et al. (2014) suggest a positive association between central government-controlled companies and CSR reporting. Wang et al. (2018) further show that Chinese companies with strong political ties tend to produce high-quality CSR reports. Overall, political ties positively influence CSR reporting in China as companies seek to meet government expectations, gain political legitimacy, and benefit from critical resources provided by the state. Their influence on the behaviour of SOEs tends to be stronger than that on non-SOEs.

4.2 General Contextual Factors

4.2.1 Regulatory Environment

The past two decades have witnessed the development of various CSR-related guidelines, which signalled the Chinese government’s expectations for companies to engage in CSR activities and reporting (Kim & Koo, 2022; Marquis & Qian, 2014; Shen et al., 2020, 2023). For example, in 2006, the China Business Council for Sustainable Development provided companies with CSR standards and best practices for reference (Marquis & Qian, 2014). The Shenzhen Stock Exchange issued a CSR guide in 2006, and the Shanghai Stock Exchange issued guidelines on environmental information disclosure in 2008, both encouraging listed companies to follow social responsibility systems, engage in CSR activities, and publish CSR reports (Marquis & Qian, 2014).

Specifically for central SOEs, the State-owned Assets Supervision and Administration Commission of the State Council issued recommendations on fulfilling social responsibility in 2008 and required all such SOEs to publish CSR reports within three years (He, 2021). In 2010, the Accountancy Department of the Ministry of Finance issued application guidelines for enterprise internal control, a section of which specified that CSR should include aspects such as environmental protection, resource-saving, product quality, safety production, and employee rights protection (Marquis & Qian, 2014).

So far, CSR reporting has remained largely voluntary in China, with no prescribed format or content. However, this is expected to change due to increasing demand from various stakeholders for relevant, transparent, and credible information disclosures (Shen et al., 2023). The Hong Kong Stock Exchange first introduced an ESG Reporting Guide in 2012 and mandated the disclosure requirements in 2020 (Shen et al., 2020). The Shanghai and Shenzhen stock exchanges required listed companies to publish a CSR/ESG report from 2022 (KPMG, 2022). More recently, in April 2024, the Shanghai and Shenzhen stock exchanges published sustainability reporting guidelines, which partially required mandatory disclosures. These recently updated regulations and requirements could significantly shape the landscape of CSR reporting, reflecting China’s commitment to sustainable development and corporate accountability and efforts to engage in international markets by adopting globally recognised practices (Parsa et al., 2021).

4.2.2 Political Context

As a typical government-led country, China features significant political influences in the development of CSR reporting practice (Kim & Koo, 2022; T. Li et al., 2023; W. Li et al., 2023; Situ et al., 2021). The Chinese government has played a facilitating role in CSR reporting through explicit CSR regulations and guidelines as part of its social harmony policy since 2006 (N. Zhao & Patten, 2016). The CSR guidelines are viewed as signals sent by a powerful actor that defines appropriate activities for companies (Marquis & Qian, 2014). Therefore, the content of CSR reports needs to comply with the Chinese government’s expectations and political beliefs (Situ et al., 2021). For example, as environmental protection has recently become a political priority, Chinese companies are increasingly expected to consider their environmental impact while pursuing profit maximisation (X. Wu & Hąbek, 2021). Disclosing information complying with the environmental protection policy can help companies effectively gain legitimacy and resources (Marquis & Qian, 2014; Situ et al., 2021). Dai et al. (2018) find that Chinese companies with high-quality CSR reports are regarded as having greater legitimacy, which leads to better financial performance with higher levels of government endorsement.

Large, particularly state-owned, Chinese companies use CSR reporting to gain political legitimacy from central and local governments (Marquis & Qian, 2014; Parsa et al., 2021; Qian & Chen, 2021; Situ et al., 2021). In turn, by signalling responses to changing expectations and conformity to global norms, CSR reporting helps the Chinese government (or the state) maintain its responsiveness and social legitimacy domestically while becoming a legitimate member of the global business community (Parsa et al., 2021). Notably, as the government authority is regarded as the ultimate stakeholder of CSR reports, Chinese reporting companies’ ability to engage wider stakeholder groups and develop their own CSR culture tends to be limited, which may restrict the further development of the reporting practice and corporate accountability (Qian & Chen, 2021).

CSR reporting in China has been developing significantly under the influence of governmental regulations and listing requirements. Since 2008, CSR guidelines introduced by the Chinese central government and stock exchanges have motivated the adoption of CSR reporting (Dong & Xu, 2016; Marquis & Qian, 2014). Wang et al. (2017) suggest that the disclosure requirements significantly enhance the quality of CSR reporting. Furthermore, He et al. (2020) find that mandatory CSR reporting has an insurance effect where Chinese companies regulate their behaviour by reducing violation costs in the stock market and increasing environmental protection expenditure. Also, Chinese companies required to issue CSR reports have gradually decreased their overall pollution levels, which indicates that non-prescriptive regulations can stimulate business innovations that improve process efficiency (Gramlich & Huang, 2023).

4.2.3 Stakeholder Expectations, Media Concerns, and Public Pressure

Expectations from various stakeholder groups are considered to influence the development of CSR reporting in China. Social organisations and intermediaries mediate CSR reporting to meet societal expectations, ensure responsiveness to international stakeholders, and help Chinese companies secure political legitimacy (Parsa et al., 2021). The media in China, as an intermediary, influences CSR reporting by shaping public awareness, endorsing reporting practices, and contributing to companies’ legitimacy (Dai et al., 2018; S. Wu et al., 2021). Media reports, either in newspapers or online, can form a positive mediation path in CSR reporting (S. Wu et al., 2021). Furthermore, Dai et al. (2018) find that Chinese companies that publish high-quality CSR reports receive greater endorsement from the media, which can contribute to enhanced perceived legitimacy both domestically and globally.

Chinese citizens tend to agree that good companies should engage in socially responsible activities (S. Xu & Yang, 2010). Li and Foo (2015) suggest that customers in China prefer environmentally and socially responsible products. Also, international customers have become salient stakeholders who influence the CSR reporting of Chinese mining and mineral companies (Dong et al., 2014). Expectations from wider stakeholder groups, such as customers, local communities, and the general public, can drive Chinese companies to engage in CSR activities and maintain transparency through regular CSR reporting (Dong et al., 2014).

The pressures from some stakeholder groups can be relatively weak, particularly when compared with the pressures from government authority, investors, and reporting regulations. For example, Chinese mining and minerals companies are almost indifferent to local communities’ interests and demands (Dong et al., 2014). Employees’ demands are largely ignored in Chinese CSR reports (Dong et al., 2014; Liu & Anbumozhi, 2009). Furthermore, Zhang and Chen (2020) argue that the increasing pressure from the media and other stakeholder groups is insufficient when it comes to enhancing the quality of Chinese CSR reporting.

4.3 Internal Contextual Factors

4.3.1 Attitudes: Corporate Culture and Views on Reporting Bad News

Some included studies explore the role of corporate culture in shaping CSR practices among Chinese companies, which may further influence how CSR is communicated. Based on a content analysis of CSR disclosures (using six criteria: presence, prominence, extent, title of CSR section, types and number of CSR issues, and level of institutionalisation of CSR practices) of 204 leading companies in Greater China, Zhao (2020) finds that mainland Chinese companies put much more effort into philanthropic activities, poverty alleviation, and disaster relief, largely driven by government values and guidelines. Hong Kong companies emphasise volunteering and partnerships in CSR implementation and community sustainable development, while Taiwanese companies focus on arts and culture, employee engagement, and environmental products, reflecting a humanist spirit. This study enriches the CSR reporting literature and provides insights into the differences between three contexts with convergent-and-divergent cultural backgrounds (M. Zhao, 2020). Based on a mixed method of in-depth interviews and a survey study of 225 Chinese companies, Yin (2017) finds that implicit ethical corporate culture, represented by an ethics institutionalisation scale measuring the level of social and ethical responsibilities embedded in the corporate culture, values, and policies, plays a key role in predicting different aspects of CSR. The author also highlights the intertwining of CSR with corporate traditions and values within Chinese companies (J. Yin, 2017).

Based on the empirical data collected through a questionnaire survey and measured by a multiple-item five-point Likert scale, Yu and Choi (2016) find that a CSR-oriented organisational culture, defined as an organisational consensus concerning shared CSR-related assumptions, values, and beliefs, plays a fully mediating role in the relationship between stakeholder pressure and Chinese companies’ adoption of CSR practices, suggesting the establishment of such a culture within organisations to gain a competitive advantage. Notably, research on how corporate culture influences Chinese CSR reporting practices is still lacking. Western CSR concepts often do not adapt well to Chinese business practices without considering the culture and traditional wisdom (such as Confucianism and Taoism) (L. Wang & Juslin, 2009). Further research is needed to enrich our understanding of the relationship between CSR reporting and corporate culture in China.

Chinese companies’ attitudes towards bad news (or negative information) can significantly influence the nature, extent, and quality of CSR reporting. In practice, this is often through disclosure strategies aiming to manage stakeholder perceptions, balance information transparency, and maintain a positive corporate image. Some included studies indicate Chinese companies’ reluctance to (fully) disclose their negative impacts, mainly due to concerns about reactions from the public and government (Chu et al., 2013; Huang & Wang, 2022; Lin, 2020, 2021). Chu et al. (2013) find that Chinese companies’ GHG reporting generally focuses on neutral and positive news, with SOEs reporting even less GHG information. Lin (2020) suggests that where negative information is disclosed, Chinese companies tend to disclose the bare minimum through a structured approach that aims to mitigate the bad news and reassure report readers. The choice of discursive strategy and the frequency of its use can reflect the company’s attitude when handling bad news. The level of Chinese CSR reporting has long been criticised for being relatively low and far from meeting different stakeholders’ information demands (X. Wu & Hąbek, 2021).

4.3.2 Process: Ownership Structure

Several included studies investigate the relationship between Chinese CSR reporting and corporate ownership structure. Considering the Chinese government’s role in encouraging CSR reporting among SOEs, Xu and Zeng (2016) suggest that state ownership is positively associated with CSR and its various components, such as ESG scores. Conversely, Patten et al. (2015) find a negative relationship between the extent of CSR reporting and the state ownership status. Xu et al. (2012) suggest varying degrees of government influence on CSR practices across different SOEs, as the relationship between state shares and CSR reporting is mixed. Moreover, Chinese SOEs tend to form a distinctive CSR reporting pattern as part of their legitimisation strategies to gain central government resources (Marquis et al., 2017). Patten et al. (2015) further suggest that although SOEs tend to disclose certain types of information, the differences between SOEs and non-SOEs are not that significant.

Apart from state ownership, some included studies explore the influence of other types of ownership structures on Chinese CSR reporting. For example, foreign ownership may be an influential factor in CSR reporting in China, as Hu et al. (2018) find that foreign investors contribute to a higher likelihood of CSR reporting adoption, though this influence is weaker in SOEs compared with private companies. Yu and Zheng (2020) find that implementing mandatory CSR reporting in China influences the investment behaviour of foreign institutional investors. These findings can be linked to Chinese companies’ recent efforts to address pressures from globalisation (Marquis et al., 2017) and join international markets by conforming to global common practices (T. Li et al., 2023; Parsa et al., 2021). Furthermore, Ma (2023) suggests that family ownership is positively related to CSR disclosures. More generally, Noronha et al. (2018) find that Chinese companies with lower concentrated ownership levels tend to have higher levels of CSR reporting.

The existing findings on the relationship between corporate ownership structure and Chinese CSR reporting remain mixed and inconclusive. Particularly, there is a lack of research investigating the influence of ownership structures other than state ownership, such as institutional ownership, on CSR reporting. Notably, there has been a growing body of literature investigating how institutional ownership influences CSR-related practices. For example, Buchanan et al. (2018) explore the interaction between CSR, influential institutional ownership, and firm value around the 2008 financial crisis and argue that influential institutional ownership mitigates the negative impact of CSR on firm value during the crisis. Ren et al. (2023) suggest that institutional ownership significantly reduces Chinese listed companies’ GHG emissions, with foreign and pressure-resistant institutional investors exerting the most substantial influence. Using fixed-effects regression models and a two-stage least squares approach, Ashton et al. (2024) find that mutual fund ownership significantly increases Chinese listed companies’ corporate environmental spending, especially for SOEs and companies operating in provinces with stronger legal environments. Furthermore, green-oriented mutual funds amplify this effect by influencing companies to prioritise sustainability (Ashton et al., 2024). Future research can build upon these studies and explore how various ownership structures influence CSR reporting in the Chinese context.

4.3.3 Process: Corporate Governance Procedures

The influence of corporate governance procedures/mechanisms on CSR reporting has been extensively investigated in the Chinese context. Specifically, the procedures/mechanisms include board size, board independence, board gender diversity, CEO-chairman duality, and the existence of a CSR board committee. Larger board sizes and more independent directors play an important role in increasing stakeholder accountability and corporate transparency (Sun et al., 2021). Some included studies find a positive correlation between board size and the level of CSR reporting (Anyigbah et al., 2023; Sun et al., 2021, 2022; C. Wang et al., 2021). Sun et al. (2021) further indicate that more directors on the board leads to a higher level of CSR report integration.

Several included studies suggest that board independence has a positive impact on CSR reporting, as independent directors are more likely to support the transparency of environmental and social disclosures (Anyigbah et al., 2023; Cherian et al., 2020; Gallego-Álvarez & Puchaveta-Martínez, 2020; Lu et al., 2015; Sun et al., 2021). Cherian et al. (2020) further suggest that companies with a higher proportion of independent directors show better performance in CSR reporting. On the contrary, Wang et al. (2021) suggest an insignificant relationship between independent directors and CSR reporting because in Chinese companies, independent directors usually have limited power to influence the decision-making process of CSR reporting.

Previous studies generally show the significant positive influence of board gender diversity on CSR reporting. Chinese companies with politically connected female directors and executives are more likely to publish CSR reports (Shaheen et al., 2021). Having more female directors means having effective supervisors who deliver better communal and ethical values through their social roles, which leads to better CSR reporting as well as financial performance (Guping et al., 2020). Moreover, female succession from male CEOs also has a positive impact on CSR reporting, as female CEO successors are more likely to improve their companies’ CSR reporting levels considering their traits, values, and preferences for green issues (Shaheen et al., 2023).

CEO-chairman duality has been criticised for negatively influencing CSR reporting, which leads to fewer information disclosures, neglected stakeholder demands, and decreased corporate transparency (Gallego-Álvarez & Pucheta-Martínez, 2020; Ma, 2023; Sun et al., 2021). One possible reason for the negative influence is that the dual status often represents more agency problems and less corporate transparency (Anyigbah et al., 2023; Cherian et al., 2020; Gallego-Álvarez & Pucheta-Martínez, 2020). For example, Sun et al. (2021) find that the level of animal welfare disclosure decreases when the CEO has a dual role, which tends to undermine the independence of the board and the transparency of the disclosure. Notably, in China, CSR strategies depend heavily on CEOs’ personal characteristics. Zhao et al. (2022) find that CEOs’ age, education experience, international experience, and political ideology are positively correlated with the likelihood of their companies publishing CSR reports.

The existence of a CSR committee promotes the adoption of CSR reporting (Adnan et al., 2018; Anyigbah et al., 2023). A CSR committee indicates that the companies are concerned about their social and environmental impacts and are committed to CSR reporting (Adnan et al., 2018). Furthermore, a CSR committee plays an essential role in helping review the companies’ CSR-related issues, policies, and reporting approaches (Anyigbah et al., 2023; Gallego-Álvarez & Pucheta-Martínez, 2020). However, Sun et al. (2022) argue that listed companies rarely set up a CSR-related committee. Where there is such a committee, the board of directors tend not to improve the level of CSR reporting (Sun et al., 2022).

4.4 Summary of Review Findings

The present SLR reveals a multifaceted landscape of Chinese CSR reporting shaped by influential factors identified and categorised into corporate characteristics, general contextual factors, or internal contextual factors. Regarding corporate characteristics, corporate size is a key factor, with larger companies reporting more extensively due to increased visibility and stakeholder pressure. Industry type, company age, financial health, and political ties also play significant roles. Larger, established companies in environmentally sensitive sectors tend to be more transparent. Financially healthy companies can better support resource-intensive CSR initiatives. In China, political ties are particularly influential, especially when it comes to SOEs, which are at the forefront of implementing government-driven economic and social policies.

The political context is a defining feature of CSR reporting in China, as the government, through policies and guidelines, encourages such reporting and embedding its ideology into business CSR practices. The Chinese government’s overriding role in shaping CSR-related practices leads to a homogeneous approach to reporting aimed at gaining political legitimacy. Other general contextual factors such as media and societal expectations also push for transparency in CSR reporting. Moreover, despite limited empirical evidence, internal contextual factors such as ownership structure, corporate governance procedures, corporate culture, and views on reporting negative information are noted. SOEs generally perform better in the adoption and quality of CSR reporting. Foreign investment is likely to drive the adoption of CSR reporting as Chinese companies endeavour to follow up with global common practices. Furthermore, more robust corporate governance procedures contribute to better CSR transparency. Notably, Chinese companies generally avoid disclosing bad news to maintain a positive corporate image and thus manage stakeholder perceptions.

We further compared the above synthesised empirical findings from the Chinese context with those in the Western context by referring to previous relevant literature review papers (Ali et al., 2017; Andrew & Baker, 2020; Arkoh et al., 2024; Fifka, 2013; Hahn & Kühnen, 2013) and highlighted the uniqueness of Chinese CSR reporting and its influential factors. CSR reporting in China is largely shaped by the influence of the prominent and powerful central government as well as traditional values and culture. The Chinese government embeds its socio-political ideology into the CSR guidelines and regulations followed by companies to ensure CSR-related practices are aligned with national strategies and political priorities. As a result, Chinese companies, both SOEs and non-SOEs, publish CSR reports primarily to gain political legitimacy and demonstrate compliance, as they regard the government authority as the ultimate stakeholder of such reports (Qian & Chen, 2021). In contrast, CSR reporting in the Western context is mostly influenced by market dynamics and stakeholder expectations, which emphasises organisational transparency, stakeholder accountability, and individualistic values (Ali et al., 2017; Arkoh et al., 2024; Fifka, 2013). Despite clear differences, there is also a trend towards convergence in CSR/sustainability reporting from a global perspective (Andrew & Baker, 2020; Hahn & Kühnen, 2013). With their international presence expanding, Chinese companies increasingly adopt internationally recognised CSR frameworks and standards, reflecting the effort to align their reporting with global norms. Similarly, Western companies operate under pressure from changing stakeholder expectations and increasingly stricter regulations, which continuously shape their CSR reporting. Either in the Chinese or Western context, the common recognition is the essential role of CSR in fostering long-term value creation, societal well-being, and sustainable development.

5. Research Agenda: New Areas of Enquiry

The present SLR further identifies several research gaps in the extant literature on the influential factors of CSR reporting in China. First, a number of influential factors remain underexplored. While this review identifies various factors influencing Chinese CSR reporting practices, some factors, particularly those in the categories of internal contextual factors, have relatively limited empirical evidence. Furthermore, referring back to Adams (2002), factors such as cultural context and ethical relativism, economic context, time, stakeholder involvement, accountant involvement, views on (CSR) reporting, and corporate culture remain unexplored in the extant literature. Further investigations into these factors could provide a more nuanced understanding of the complexities of Chinese CSR reporting practices. Also, the extant literature predominantly focuses on large, public, or state-owned Chinese companies. There is a lack of studies on small and medium-sized companies, which may behave differently in CSR reporting due to distinct corporate characteristics, challenges and opportunities, and stakeholder expectations. Expanding the sample to include these companies could provide a more comprehensive view of CSR reporting in China.

From a methodological perspective, this SLR shows that the majority of included studies use quantitative methods, with fewer qualitative or mixed-method studies. This methodological gap may lead to a lack of deeper investigations into complex issues in CSR reporting in China, such as the cultural nuances influencing the reporting practice or the decision-making processes within organisations. The existing body of empirical research will benefit from more qualitative and mixed-method studies that could enhance methodological diversity and research robustness. Moreover, there is a lack of longitudinal research tracking changes in Chinese CSR reporting practices, particularly given recent regulatory updates. Longitudinal studies could shed light on the development of CSR reporting over time and the long-term influence of specific influential factors. Also, more comparative studies are needed to explore different CSR reporting practices between Chinese companies and their peers across different countries or regions. Such studies could further uncover unique political, cultural, and social influential factors of CSR reporting in various national/regional contexts.

Though not specifically addressed in this SLR, the extant literature on CSR reporting in China lacks theoretical development, particularly regarding the combination of commonly invoked CSR theories (such as legitimacy theory, stakeholder theory, and institutional theory) and localised cultural/political theories that might be more applicable to China. Integrating contextualised theoretical perspectives into general CSR theories could enrich the analysis and understanding of CSR reporting in China. Furthermore, theoretical frameworks from other relevant disciplines could be invoked to address the multifaceted nature of CSR reporting and provide novel insights into the complex interplay among various influential factors. China’s unique approach to CSR reporting provides opportunities to develop new theories that are different from existing CSR theories (often originating from Western contexts) and can effectively explain CSR reporting practices and influences within emerging or transitional economies.

We call for future empirical and theoretical studies to address the research gaps identified above and thus enrich the existing body of knowledge in the field of CSR reporting in China. Specifically, a number of new areas are suggested for future research, which include the following:

-

Explore the changing regulatory environment of CSR reporting in China. Particularly given the recent regulatory shift from voluntary to mandatory reporting, it is necessary to examine how this change influences reporting quality and corporate behaviour across different industries/sectors and company sizes, thus evaluating the effectiveness of regulations. Attention also needs to be paid to CSR reporting in small and medium-sized Chinese companies and the barriers they face within the changing regulatory environment.

-

Identify cultural and ethical influential factors (e.g., traditional Chinese values) and determine how these factors influence Chinese CSR reporting practices. Future research can further explore how these factors and the changing regulatory environment intersect to shape CSR reporting, ideally through longitudinal studies.

-

Investigate how international sustainability reporting standards and frameworks shape Chinese CSR reporting practices, given that Chinese companies are increasingly held to international standards with globalisation. Future studies can also compare international and local reporting standards and discover local adaptations, best practices, and areas for improvement.

-

Explore how different stakeholder groups intersect and influence CSR reporting, particularly the power dynamics between the groups and how they shape CSR priorities and strategies. Furthermore, as an emerging area attracting enormous interest, the role of technological tools (e.g., big data and artificial intelligence) in enhancing stakeholder engagement and improving the accuracy, relevance, and timeliness of CSR reporting could be explored.

-

Determine how specific internal context factors, such as vision, mission and values, internal control (or, more specifically, accounting) systems and the role of accountants, influence the decision-making process of CSR reporting.

-

Determine how corporate characteristics, general contextual factors, and internal contextual factors impact each other in the decision-making process of CSR reporting at organisational level. For example, the political and cultural context in China shapes individual values, characteristics, and behaviours, which can impact the aggregated attitudes towards CSR reporting within organisations. Exploring the intertwinement of the three types of influential factors could generate a nuanced understanding of how CSR reporting is institutionalised from both macro- and micro-level perspectives.

-

Compare CSR reporting in China and other emerging or developed economies to both provide global insights and validate unique contextualised aspects in light of different regulatory, economic, and cultural contextual factors.

The investigation of the above areas would benefit from more qualitative studies that capture detailed opinions, experiences, and perceptions of CSR reporting practices in China. Mixed-method studies are also encouraged to develop and validate new theoretical perspectives, enhance research robustness, and provide a comprehensive view of CSR reporting in China. Moreover, it will be beneficial if the above areas can be investigated through one or more theoretical lenses. Although the present SLR specifically focuses on the Chinese context, we encourage scholars to research the above areas suggested or other relevant issues within different national/regional contexts to contribute to the burgeoning CSR reporting field.

6. Concluding Remarks

This SLR has comprehensively examined the multifaceted influences shaping CSR reporting in China by synthesising previous empirical evidence and analysing the influential factors categorised as corporate characteristics, general contextual factors, or internal contextual factors. The review findings highlight the essential role of the Chinese government and relevant regulations in driving the adoption of CSR reporting in China. Due to the significant political influences, CSR reporting largely serves as a tool to gain political legitimacy. Other general contextual factors, such as cultural context, ethical relativism, and economic context, remain underexplored in the extant literature. Considering corporate characteristics, large Chinese companies, typically SOEs, engage more in CSR reporting as they are motivated by greater visibility (especially by the Chinese government), larger environmental and social footprint, and higher stakeholder pressure. Also, Chinese companies with better financial performance are more likely to implement CSR activities and reporting. Environmentally sensitive or polluting industries and mature, well-established companies show better performance in CSR reporting.

The previous empirical evidence tends to be limited when it comes to internal contextual factors. This review captures ownership structure, corporate governance procedures, and attitudes towards bad news. However, referring back to Adams (2002), a number of internal contextual factors remain underexplored in the extant literature on CSR reporting in China. This SLR contributes to the literature by identifying research gaps in the existing body of knowledge and recommending new areas for future research to enhance the understanding of CSR reporting in China and beyond. Particularly, it emphasises the need for qualitative and mixed-method research, comparative and longitudinal studies, and theory development to enrich the discourse and provide deeper insights into the complex dynamics of the CSR reporting field.

This SLR, while comprehensive in its scope and analysis, is not without limitations. The sample of the review was limited to empirical research papers published in English and peer-reviewed journals, thus potentially excluding relevant conference proceedings, book chapters, industry reports, and research published in Chinese or other languages. The language and publication biases might restrict the perspective diversity of the included studies. Also, the review period from 2004 to 2023 means that more recent developments emerging post 2023 might not be fully captured. Moreover, as the included studies largely employ quantitative research methods, the review findings tend to lack nuanced qualitative insights into the complexities of Chinese CSR reporting practices. This methodological bias might influence the completeness of the review findings.

Last but not least, regarding Adams’ (2002, p. 246) framework, we found ambiguity in “time” (not sure what it refers to as a general contextual factor) and “decision horizon (long-term or short-term)” (not sure why it is a corporate characteristic rather than an internal contextual factor as it seems relevant to internal decision-making processes or leadership practices). Also, in “internal context”, the factor “views on recent increase in reporting, reporting bad news, reporting in the future, regulation and verification” includes several elements that it would be more sensible and beneficial to consider separately and define clearly. Furthermore, given that CSR reporting is an evolving and expanding field, the factors and interrelationships depicted by Adams (2002) may have been dated, which requires updating to reflect recent changes. Future research can empirically validate, refine and update the framework. Overall, addressing this study’s limitations in future research could provide a more inclusive understanding of CSR reporting in China and its influential factors.